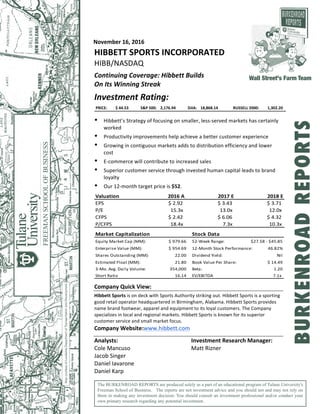

1. November 16, 2016

HIBBETT

SPORTS

INCORPORATED

HIBB/NASDAQ

Continuing

Coverage:

Hibbett

Builds

On

Its

Winning

Streak

Investment

Rating:

PRICE: $ 44.53 S&P 500: 2,176.94 DJIA: 18,868.14 RUSSELL 2000: 1,302.20

• Hibbett’s

Strategy

of

focusing

on

smaller,

less-‐served

markets

has

certainly

worked

• Productivity

improvements

help

achieve

a

better

customer

experience

• Growing

in

contiguous

markets

adds

to

distribution

efficiency

and

lower

cost

• E-‐commerce

will

contribute

to

increased

sales

• Superior

customer

service

through

invested

human

capital

leads

to

brand

loyalty

• Our

12-‐month

target

price

is

$52.

Valuation

2016

A

2017

E 2018

E

EPS $

2.92 $

3.43 $

3.71

P/E 15.3x

13.0x

12.0x

CFPS $

2.42 $

6.06 $

4.32

P/CFPS 18.4x

7.3x

10.3x

Market

Capitalization Stock

Data

Equity

Market

Cap

(MM): $

979.66 52-‐Week

Range:

$27.58

-‐

$45.85

Enterprise

Value

(MM): $

954.69 12-‐Month

Stock

Performance: 46.82%

Shares

Outstanding

(MM): 22.00 Dividend

Yield: Nil

Estimated

Float

(MM): 21.80 Book

Value

Per

Share: $

14.49

3-‐Mo.

Avg.

Daily

Volume: 354,000 Beta: 1.20

Short

Ratio 16.14 EV/EBITDA 7.1x

Company

Quick

View:

Hibbett

Sports

is

on

deck

with

Sports

Authority

striking

out.

Hibbett

Sports

is

a

sporting

good

retail

operator

headquartered

in

Birmingham,

Alabama.

Hibbett

Sports

provides

name

brand

footwear,

apparel

and

equipment

to

its

loyal

customers.

The

Company

specializes

in

local

and

regional

markets.

Hibbett

Sports

is

known

for

its

superior

customer

service

and

small

market

focus.

Company

Website:www.hibbett.com

Analysts:

Investment

Research

Manager:

Cole

Mancuso

Matt

Rizner

Jacob

Singer

Daniel

Iavarone

Daniel

Karp

The BURKENROAD REPORTS are produced solely as a part of an educational program of Tulane University's

Freeman School of Business. The reports are not investment advice and you should not and may not rely on

them in making any investment decision. You should consult an investment professional and/or conduct your

own primary research regarding any potential investment.

Wall Street's Farm Team

BURKENROADREPORTS

2. Hibbett

Sports

Incorporated

(HIBB)

BURKENROAD

REPORTS

(www.burkenroad.org)

November

16,

2016

2

Figure

1:

Five-‐year

Stock

Price

Performance

Source:

Yahoo

Finance

INVESTMENT

SUMMARY

Our

team

gives

Hibbett

Sports

an

investment

rating

of

Market

Perform

by

assigning

a

12

month

target

stock

price

of

$52.

We

predict

that

the

November23rd

price

of

$41.50

will

increase

by

25.3%

to

reach

our

target

stock

price.

We

forecasted

revenue

by

using

a

quantity

and

price

method

focusing

on

revenue

per

square

foot

and

total

store

square

footage.

For

this

forecast,

we

factored

in

the

seasonality

of

the

sporting

goods

industry

by

using

historical

data

to

predict

revenue

per

square

foot

by

quarter.

Hibbett

Sports

is

a

sporting

goods

retailer

headquartered

in

Birmingham,

Alabama.

Hibbett

Sports

focuses

on

the

small

to

mid-‐sized

markets

located

in

the

Mid-‐Atlantic,

Midwest

and

Southern

regions

of

the

U.S.

The

Company

offers

high

quality

and

regionally

specific

apparel,

footwear,

and

equipment

in

order

to

appeal

to

its

customers

in

different

markets.

Hibbett’s

ability

to

respond

quickly

to

major

sporting

events

allows

the

Company

to

appeal

to

thelocal

interests

of

its

customers.

Hibbett

employs

3,300

full

time

and

5,600

part-‐time

employees

that

are

dedicated

to

establishing

strong

relationships.

The

Company

operates

1,044

retail

stores

throughout

33

states.

Hibbett

takes

advantage

of

efficiencies

in

logistics,

marketing,

and

regional

management

by

opening

new

stores

that

are

within

a

two-‐hour

driving

distance

from

an

existing

store.

Hibbett

Sports

focuses

on

developing

significant

relationships

within

local

communities

and

customers

in

order

to

build

brand

loyalty.

3. Hibbett

Sports

Incorporated

(HIBB)

BURKENROAD

REPORTS

(www.burkenroad.org)

November

16,

2016

3

Table

1:

Historical

Burkenroad

Ratings

and

Prices

Report

Date

Stock

Price

Rating

12

Month

Target

Price

10/30/15

$34.16

Market

Outperform

$42.00

11/22/13

$62.72

Market

Perform

$63.00

11/06/12

$53.95

Market

Perform

$56.00

11/29/11

$44.05

Market

Perform

$48.00

11/26/10

$34.61

Market

Perform

$37.36

12/08/09

$19.85

Market

Perform

$22.10

04/11/08

$16.00

Market

Outperform

$20.36

INVESTMENT

THESIS

Our

team

assessed

Hibbett

Sports

with

a

Market

Perform

rating.

We

attribute

this

rating

to

a

12-‐month

target

price

of

$52.

The

Company’s

future

growth

can

be

attributed

to

its

expanding

store

operations,

satisfying

customer

experience,

and

investments

in

human

capital.

Considering

these

factors,

Hibbett

appears

to

possess

significant

upside

potential.

Hibbett’s

Strategy

of

focusing

on

smaller,

less-‐served

markets

has

certainly

worked

Hibbett’s

strategy

involves

targeting

isolated

markets

with

less

competition.

As

such,

the

Company

is

currently

undergoing

a

clustered

expansion

program.

Under

this

program,

Hibbett

aims

to

open

new

stores

within

two

hours

driving

distance

of

existing

stores

(see

Figure

2).

By

targeting

smaller

communities,

avoiding

congested

urban

regions,

and

expanding

in

a

clustered

method,

Hibbett

achieves

greater

marketing

success,

larger

economies

of

scale,

and

decreasing

costs

per

store.

Furthermore,

suburban

and

rural

markets

result

in

lower

corporate,

logistical,

and

operational

expenses.

Hibbett

also

combats

low

customer

frequency

by

locating

stores

near

strip

centers

and

super

stores

like

Walmart.

Figure

2:

Hibbett

Store

Map

by

State

Source:

Hibbett’s

Roadshow

Presentation

4. Hibbett

Sports

Incorporated

(HIBB)

BURKENROAD

REPORTS

(www.burkenroad.org)

November

16,

2016

4

Productivity

Improvements

help

achieve

a

better

customer

experience

Hibbett’s

management

capitalizes

on

its

customer

base

by

choosing

different

products

lines

for

different

communities.

The

Company

offers

regional

team

and

college

inspired

apparel

and

sports

gear.

Additionally,

the

sports

gear

offered

is

based

on

the

weather

conditions

and

fields

in

the

area.

With

products

correlated

to

community

needs

and

wants,

Hibbett’s

customers

find

a

highly

satisfying

customer

experience.

After

management

creates

a

product

line,

it

maintains

relevant

product

offerings

through

high-‐tech

information

systems.

These

systems

help

record

customer

data

and

decipher

trends

in

the

market

so

Hibbett

is

always

selling

exactly

what

the

customer

wants.

Growing

in

contiguous

markets

adds

to

distribution

efficiency

and

lower

cost

All

of

Hibbett’s

merchandise

is

shipped

and

received

from

a

single

wholesale

and

logistics

facility

in

Alabaster,

Alabama.

This

centralized

distribution

facility

allows

Hibbett

to

maintain

low

operating

costs,

as

well

as

to

use

third-‐party

logistic

providers

to

help

it

gain

efficiencies

by

25%

at

their

outlying

stores.

The

Company’s

logistic

and

wholesale

facility

is

designed

with

automation

and

to

ensure

efficiency

and

lower

costs.

E-‐commerce

will

contribute

towards

increased

sales

Hibbett’s

primary

revenue

source

will

continue

to

be

from

brick

and

mortar

stores;

however,

a

growing

and

more

developed

website

should

lead

to

significant

revenue

generation.

E-‐

commerce

is

an

integral

section

of

Hibbett’s

omni-‐channel

initiative

with

a

strategy

of

engaging

the

consumer

in

multiple

platforms.

Growth

in

Hibbett’s

e-‐commerce

sales,

which

currently

represents

only

5%

of

Company

sales,

could

potentially

lead

to

more

accurate

information

systems.

Ultimately,

the

increase

in

technology

and

implementation

of

the

omni-‐channel

initiative

will

create

a

more

individualized

customer

experience

which

will,

in

turn,

lead

to

higher

customer

satisfaction.

Superior

customer

service

through

invested

human

capital

leads

to

brand

loyalty

The

final

piece

in

Hibbett’s

strategy

is

carrying

out

exceptional

customer

service.

Sales

associates

are

trained

and

specialized

in

sporting

goods

products.

As

a

result,

employees

are

able

to

effectively

manage

customers’

needs

and

provide

assistance

throughout

their

visit.

This

further

enhances

the

customer

experience

and

builds

strong

brand

loyalty

to

Hibbett.

5. Hibbett

Sports

Incorporated

(HIBB)

BURKENROAD

REPORTS

(www.burkenroad.org)

November

16,

2016

5

VALUATION

Hibbett’s

Stock

price

is

$44.53

as

of

November

16,

2016.

We

calculated

a

12-‐month

target

price

of

$51

for

Hibbett

using

the

discounted

cash

flow

(DCF)

and

relative

multiple

methods

(See

figure

3).

Figure

3:

Hibbett’s

Current

Stock

Price

and

12-‐Month

Target

Price

Source:

Burkenroad

Valuation

Discounted

Cash

Flow

A

large

component

of

Hibbett’s

performance

is

based

on

the

amount

of

square

footage

their

stores

cover.

As

such,

we

forecasted

revenue

using

a

quantity

and

price

method

based

on

revenue

per

square

foot.

In

projecting

total

square

footage,

we

estimated

a

growth

rate

in

stores

using

both

historical

figures

and

management

projections.

Other

notable

figures

we

used

to

discount

free

cash

flows

to

the

firm

are

the

risk

free

rate,

market

risk

premium,

and

Hibbett’s

beta,

all

of

which

we

found

on

Bloomberg.

In

order

to

calculate

the

weighted

average

cost

of

capital

(WACC),

we

used

the

capital

asset

pricing

model,

as

the

Company

has

no

debt.

We

then

assumed

a

liquidity

premium

to

further

discount

the

cash

flows.

Finally,

we

assumed

a

terminal

growth

rate

of

3%.

Discounting

the

next

ten

years’

free

cash

flows

and

terminal

value

to

present

value,

we

calculated

Hibbett

having

a

target

price

of

$51.

$20.00

$25.00

$30.00

$35.00

$40.00

$45.00

$50.00

$55.00

$60.00

DCF

P/E

15X

P/BV

3.16X

12-‐Month

Target

Price:

$52.00

Current

Price:

$44.53

6. Hibbett

Sports

Incorporated

(HIBB)

BURKENROAD

REPORTS

(www.burkenroad.org)

November

16,

2016

6

Relative

Multiple

Methods

In

our

analysis,

we

also

used

two

relative

multiples:

price

to

equity

(P/E)

and

price

to

book

value

(P/BV).

When

looking

at

Hibbett’s

peers

to

calculate

multiple

values,

we

used

historical

figures

from

Dick’s,

Cabela’s,

Footlocker,

and

Genesco.

We

found

an

industry

average

P/E

ratio

of

15x

and

when

applied

to

Hibbett,

we

calculated

a

target

price

of

$54.

We

found

an

industry

average

P/BV

of

3.16

and

when

applied

to

Hibbett,

we

calculated

a

target

price

of

$51.

After

analyzing

all

three

calculated

prices,

we

decided

on

a

12-‐month

target

price

of

$51.

INDUSTRY

ANALYSIS

Hibbett

Sports,

Inc.

operates

in

the

sporting

goods

store

industry.

The

sporting

goods

industry

is

highly

fragmented

with

no

single

company

controlling

more

than

17%

of

the

total

market

share.

In

recent

years

the

industry

has

experienced

more

competition

from

e-‐commerce,

specialty

stores,

and

mass

merchandisers.

The

introduction

of

these

new

competitors

has

led

to

a

more

fragmented

market

as

well

as

a

price-‐based

competition

environment.

According

to

the

American

College

of

Sports

Medicine,

alternative

exercise

methods,

such

as

yoga

and

pilates,

are

expected

to

drive

industry

revenue

growth

in

the

coming

years.

This

is

due

to

the

growing

health

consciousness

of

middle

aged

and

elderly

Americans.

These

individuals

are

expected

to

participate

in

low

intensity

exercises

such

as

swimming,

yoga,

and

bowling

which

will

stimulate

sales

of

both

apparel

and

sports

equipment

for

these

exercises.

Additionally,

team

sport

participation

is

expected

to

rise

by

1%

in

the

next

five

years.

Current

state

of

the

industry

and

changing

cultural

trends

have

presented

a

number

of

challenges

for

Hibbett’s

management.

Hibbett

primarily

focuses

on

selling

quality,

brand

name

merchandise

such

as

Nike,

Adidas,

and

Oakley.

The

growing

presence

of

online

retailers,

such

as

Amazon,

and

mass

merchandisers,

such

as

Walmart

and

Target,

have

forced

Hibbett

to

lower

its

prices

to

remain

competitive.

Additionally,

Hibbett

has

been

slow

to

respond

to

the

increasing

importance

of

e-‐commerce,

as

online

sales

represent

just

5%

of

total

revenue.

This

is

in

stark

contrast

with

competitors

such

as

Dick’s

Sporting

Goods

and

Academy

Sports.

Individuals,

specifically

those

aged

7-‐17,

are

choosing

to

participate

in

more

leisure

activities

than

sporting

activities

in

recent

years.

Individuals

aged

7-‐17

participated

in

slightly

fewer

team

sports.

This

can

be

attributed

to

a

number

of

factors

but

one

of

the

primary

reasons

is

the

growing

video

gaming

industry.

As

these

games

become

more

advanced

and

interactive,

individuals

are

choosing

to

spend

their

time

playing

these

games

as

opposed

to

participating

in

exercises

or

team

sports

(IBIS

World).

7. Hibbett

Sports

Incorporated

(HIBB)

BURKENROAD

REPORTS

(www.burkenroad.org)

November

16,

2016

7

Industry

State

The

sporting

goods

industry

is

currently

consolidating

and

experiencing

low

revenue

volatility,

low

revenue

growth,

and

high

competition.

These

factors

are

indicative

of

an

industry

in

the

mature

lifecycle

stage.

The

high

number

of

consolidations

has

allowed

some

retailers

to

bypass

sporting

wholesalers

and

reduce

overall

costs.

Additionally,

as

more

competition

has

entered

the

industry,

retailers

have

started

to

pursue

exclusive

deals

with

both

wholesalers

and

manufactures

in

order

to

limit

availability

of

products

and

drive

their

brands.

Sporting

goods

stores

have

begun

to

focus

on

apparel

and

footwear

in

recent

years,

as

these

high

margin

products

have

grown

in

popularity.

Apparel

sales

have

been

spurred

by

the

increased

sports

participation

among

women

as

well

as

sport-‐specific

apparel

such

as

tennis

shorts

and

golf

shirts.

Developing

Health

Consciousness

According

to

IBIS

World,

individuals

are

expected

to

participate

in

more

exercise

and

team

sports

in

the

coming

years

due

to

the

increased

health

consciousness

of

the

population.

Individuals

aged

18-‐44

have

been

growing

more

health

conscious

in

recent

years

as

they

engage

in

physical

activities

such

as

camping

and

fishing.

This

group

presents

two

opportunities

to

the

sporting

goods

industry.

The

primary

opportunity

is

this

groups’

increasing

demand

for

sports

apparel

and

footwear.

According

to

IBIS

World,

this

group

is

expected

to

comprise

42.5%

of

industry

revenue

in

2016.

Additionally,

many

individuals

in

this

age

group

have

children.

As

more

schools

no

longer

require

fitness

classes,

these

parents

are

emphasizing

physical

activities

for

both

themselves

and

their

children.

These

activities

often

include

fishing

and

camping

which

suggests

that

the

parents

will

become

more

active

as

their

children

get

older

(IBIS

World).

One

major

concern

is

that

17%

of

children

and

adolescents

are

obese.

This

is

a

historically

high

number

and

it

provides

a

counterbalance

towards

the

overall

growing

health

consciousness

environment.

Key

Success

Factors

Due

to

the

fragmented

nature

of

the

sporting

goods

industry,

companies

must

be

efficient

with

their

resources

and

maximize

revenue

opportunities

through

marketing,

product

selection,

and

market

control.

Hibbett

attempts

to

maximize

its

revenue

by

offering

products

that

are

regionally

favored,

such

as

Atlanta

Braves

and

Crimson

Tide

apparel

in

Georgia

and

Alabama.

Another

key

success

factor

is

location

in

key

markets.

High

foot

and

vehicle

traffic

correlates

with

increased

revenue.

Hibbett,

with

its

emphasis

on

small

and

medium

sized

markets,

is

limited

in

its

ability

to

generate

high

traffic.

Other

key

success

factors

are

disposable

personal

income

(DPI),

consumer

confidence,

and

gross

domestic

product

(GDP).

As

disposable

income

rises,

individuals

can

purchase

more

luxury

items

such

as

sports

apparel,

footwear

and

sports

equipment.

This

is

particularly

important

to

Hibbett

as

its

products

are

generally

more

expensive

than

those

products

offered

by

mass

merchandisers.

Additionally,

as

gross

domestic

product

grows,

consumer

confidence

grows

and

this

makes

it

more

likely

that

individuals

will

spend

money

on

more

expensive,

higher

quality

items.

8. Hibbett

Sports

Incorporated

(HIBB)

BURKENROAD

REPORTS

(www.burkenroad.org)

November

16,

2016

8

Growing

E-‐Commerce

A

major

development

in

general

retailing

is

the

tremendous

growth

e-‐commerce

has

played

in

sales.

In

fact,

sporting

goods

retailers

have

developed

their

own

websites

to

connect

with

customers

at

home.

The

emergence

of

online

sales

has

not

only

increased

competition

between

sporting

goods

stores,

but

online

sales

has

allowed

general

retailers

and

athletic

brands

to

enter

the

market.

Online

distributors

and

merchandisers,

like

Nike,

are

able

to

sell

directly

to

customers.

This

access

to

customers

allows

online

distributors

and

merchandisers

to

cut

out

retail

stores

such

as

Hibbett

Sports.

In

fact,

Nike’s

annual

online

sales,

totaling

over

$1

billion,

now

amount

to

more

than

Hibbett’s

total

sales.

To

fight

this

growing

trend,

sporting

goods

retailers

are

relying

on

the

consumer's’

desire

to

test

equipment

or

ask

a

specialist

for

assistance.

Availability

of

Substitutes

Sporting

goods

are

not

difficult

to

purchase.

Consumers

can

look

to

alternatives

such

as

department

stores,

big-‐box

retailers,

and

online

distributors.

Online

distributors

pose

a

significant

threat

as

popularity

grows

and

prices

drop.

Currently,

Hibbett

has

only

about

5%

of

its

sales

online.

Hibbett’s

major

draw

is

the

knowledge

employees

can

provide

on

specific

sports

equipment,

coupled

with

the

understanding

of

what

best

matches

the

needs

of

the

community

where

customers

are

located.

For

example,

sales

associates

will

know

which

cleats

perform

best

on

the

local

high

school's

field.

Bargaining

Power

of

Suppliers

In

order

to

maintain

high-‐quality

merchandise,

sporting

goods

stores

are

reliant

on

a

few

top

brands

to

supply

products.

The

sporting

goods

industry

is

primarily

brand

name

driven.

As

such,

over

70%

of

Hibbett’s

inventory

purchases

can

be

attributed

to

three

vendors.

This

heavy

reliance

on

a

few

vendors

gives

suppliers

significant

bargaining

power

over

sporting

goods

retailers.

This

dependence

on

few

vendors

requires

small

and

mid-‐sized

sporting

goods

stores

to

maintain

strong

and

stable

relationships

with

these

vendors.

Bargaining

Power

of

Buyers

As

a

sporting

goods

store

that

sells

directly

to

the

end

user,

Hibbett

has

no

major

single

customer.

Consumers

are

able

to

gain

their

small

bargaining

power

through

their

ability

to

purchase

products

from

alternative

stores.

Hibbett

must

be

constantly

aware

of

competitors’

prices;

however,

due

to

the

Company’s

investment

in

employee

knowledge

in

training

and

product

knowledge,

consumers

are

less

price

sensitive

than

competitors.

9. Hibbett

Sports

Incorporated

(HIBB)

BURKENROAD

REPORTS

(www.burkenroad.org)

November

16,

2016

9

Threat

of

Entry

The

high

initial

costs

to

entering

the

sporting

goods

industry

make

up

a

large

portion

the

barriers

to

entry.

These

costs

include

the

building,

inventory

to

fill

a

retail

store,

and

cost

of

training

employees.

A

new

entrant

would

likely

need

to

spend

additional

capital

on

marketing

expenses

in

order

to

compete

against

the

well-‐established

sporting

goods

stores.

Furthermore,

a

new

entrant

would

require

a

line

of

credit.

Retailers

use

lines

of

credit

to

purchase

inventories

and

cover

other

short-‐term

operating

expenses.

Additionally,

retail

is

a

relatively

unregulated

industry

with

very

few

competitive

advantages

other

than

capital.

For

these

reasons,

the

threat

of

entry

in

the

sporting

goods

industry

is

moderate.

Competitive

Rivalry

The

retail

sporting

goods

industry

is

increasingly

competitive.

This

has

directly

led

to

decreasing

prices

and

aggressive

marketing

campaigns.

Firms

compete

primarily

on

price

but

also

battle

over

service,

quality

and

range

of

products,

and

knowledge

of

the

communities.

A

consequence

of

this

stiff

competition

is

consolidation

and

a

sharp

rise

in

acquisitions.

Companies

are

focusing

on

decreasing

costs,

increasing

efficiency,

and

gaining

market

share.

ABOUT

HIBBETT

Hibbett

Sports

Inc.

is

a

sporting

goods

retail

operator

headquartered

in

Birmingham,

Alabama.

Hibbett

Sports

focuses

on

the

small

to

mid-‐sized

markets.

The

Company

also

targets

the

Mid-‐

Atlantic,

Midwest,

and

Southern

regions

of

the

U.S.

In

1945,

Hibbett

Sports

opened

a

single

location

in

Florence,

Alabama

that

sold

athletic,

marine

and

small

aircraft

equipment.

In

1960,

Hibbett

decided

to

focus

primarily

on

sporting

goods

merchandise.

Mickey

Newsome

was

soon

hired

as

Chief

Executive

Officer,

and

he

helped

expand

Hibbett

Sports

Inc.

from

12

stores

to

79

stores,

eventually

taking

the

Company

public

in

October

of

1996.

As

of

January

2016,

Hibbett

Sports

operated

1,044

retail

stores

in

33

states

of

the

U.S.

Hibbett

Sports

stores

account

for

98%

of

the

Company’s

locations,

while

the

other

2%

are

smaller-‐format

sports

athletic

shoe

stores

(see

figure

4).

10. Hibbett

Sports

Incorporated

(HIBB)

BURKENROAD

REPORTS

(www.burkenroad.org)

November

16,

2016

10

Figure

4:

Hibbett

Sports

Inc.

Store

Location

by

State

Products

Hibbett

provides

an

array

of

quality

name

brand

footwear,

apparel,

and

athletic

equipment

at

an

economical

price

point

with

a

full

service

environment.

The

Company

emphasizes

the

importance

of

providing

local

products.

For

fiscal

year

2016,

Hibbett

generated

49%

of

net

sales

from

footwear,

29%

from

apparel,

and

22%

from

equipment.

Competitive

Advantage

Hibbett’s

competitive

advantage

is

derived

from

six

key

factors:

Logistics-‐

All

of

Hibbett’s

merchandise

is

shipped

and

received

from

a

single

wholesale

and

logistics

facility

in

Alabaster,

Alabama.

This

centralized

distribution

facility

allows

Hibbett

to

maintain

low

operating

costs,

as

well

as

to

use

third-‐party

logistic

providers

to

help

it

gain

efficiencies

by

25%

at

their

outlying

stores.

The

Company’s

logistic

and

wholesale

facility

is

designed

with

automation

and

operational

efficiencies.

All

of

these

aspects

play

a

key

role

in

Hibbett

Sports

expansion

strategy.

Small

Market

Focus-‐

Hibbett

Sports

targets

small

communities

that

range

in

population

from

25,000

to

100,000

residents.

The

Company’s

strong

focus

on

regional

markets

has

resulted

in

reduced

corporate

expenses,

lower

logistic

costs,

and

increased

economies

of

scale

from

marketing

activities.

Store

Concepts-‐

Hibbett

Sports’

retail

format

is

approximately

5,000

square

feet

per

store,

with

locations

near

a

highly

populated

Walmart

store.

About

80%

of

all

Hibbett

Sports

stores

are

located

in

strip

centers

which

allow

greater

access

for

consumers.

11. Hibbett

Sports

Incorporated

(HIBB)

BURKENROAD

REPORTS

(www.burkenroad.org)

November

16,

2016

11

Merchandise-‐

Hibbett

provides

quality,

brand

name

merchandise

at

an

economical

price

that

is

lower

than

its

competitors.

Although

Hibbett

stocks

a

mostly

identical

general

inventory

within

its

locations,

the

Company

often

caters

to

local

and

regional

communities

through

inclusion

of

event

and

community

specific

offerings.

Customer

Service-‐

Hibbett

Sports

is

known

for

its

superior

customer

service

at

every

location.

Hibbett

Sports

provides

customers

in

different

communities

with

extensive

knowledge

on

mainstream

products,

as

well

as

the

regionally

targeted

products

that

the

Company

offers

to

different

communities.

Because

of

its

competitive

industry,

Hibbett

offers

a

personalized

customer

experience

that

affords

the

Company

a

competitive

advantage

over

its

peers.

This

aspect

of

the

Company

is

a

core

value

that

has

driven

success

day

in

and

day

out.

Information

Systems-‐

Over

the

past

few

years,

Hibbett

has

invested

in

information

systems

that

are

flexible

enough

to

meet

the

needs

of

each

store

location.

These

systems

assist

in

financial

control,

cost

management,

inventory

control,

merchandise

planning,

logistics,

replenishment,

and

product

allocation.

Corporate

Expansion

Strategy

Top

executives

at

Hibbett

Sports

are

implementing

two

main

strategies,

which

they

hope

can

help

expedite

growth.

The

first

strategy

primarily

focuses

on

opening

new

stores

within

120

miles

of

an

existing

Hibbett

location.

The

second

strategy

involves

investing

in

infrastructure

to

reach

customers

through

digital

commerce.

Recent

Developments

In

order

to

satisfy

the

strategies

for

corporate

expansion,

Hibbett

Sports

has

implemented

an

upgrade

to

its

point-‐of-‐sale

(POS)

system,

which

allows

the

Company

to

gain

inventory

visibility

across

all

stores

and

allow

store-‐to-‐store

transfers

to

complete

a

customer

sale.

This

new

POS

system

will

allow

Hibbett

Sports

employees

to

provide

a

better

customer

experience,

which

will

layer

onto

the

Company’s

current

superb

customer

service.

In

addition

to

the

upgrade

of

the

POS

system,

Hibbett

Sports

will

implement

a

new

Customer

Relationship

Management

(CRM)

capability

that

improves

its

ability

to

communicate

and

market

to

its

loyal

customers.

This

CRM

software

will

also

allow

the

Company

to

enable

a

store-‐to-‐home

capability,

which

allows

Hibbett’s

chain-‐wide

inventory

to

be

shipped

directly

to

a

customer’s

home.

The

addition

will

help

retain

the

Company’s

five

million

loyalty

members

who

are

enrolled

in

a

MVP

rewards

program.

The

goal

is

to

have

these

systems

provide

a

better

customer

experience,

which

in

turn

will

gain

more

loyalty

members

following

a

positive

experience.

Recent

2016

figures

show

that

Hibbett

Sports

added

56

stores

between

the

fourth

quarters

of

2015

and

2016.

This

increase

in

stores

has

caused

net

sales

to

increase

2.6%,

from

$239.3

million

to

$245.7

million

from

the

fourth

quarter

of

2015

to

the

fourth

quarter

of

2016.

12. Hibbett

Sports

Incorporated

(HIBB)

BURKENROAD

REPORTS

(www.burkenroad.org)

November

16,

2016

12

PEER

ANALYSIS

Hibbett

Sports,

Inc.

has

many

established

peers

active

in

the

sporting

goods

retail

industry.

Its

peers

include

Dick’s

Sporting

Goods

Inc.,

Big

5

Sporting

Goods

Corporation,

Cabela’s

Incorporated,

and

Academy

Sports

+

Outdoors.

It

is

important

to

note

that

a

former

peer,

The

privately-‐owned

Sports

Authority,

filed

for

bankruptcy

earlier

in

the

year

and

its

brand

was

acquired

by

Dick’s.

Table

2:

Hibbett’s

Peers

Company Hibbett

Dick’s

Big

5

Cabela’s

Symbol HIBB

DKS

BGFV CAB

Market

Cap 972M 7.04B

318M 3.53B

P/E 13.64 21.58 2.85 0.83

EPS 3.05 2.85 0.52 2.64

Beta

1.05 0.83 0.52 0.97

ROE

22.19% 18.25% 7.77% 10.39%

Operating

CF

58.80M 643.00M 16.40M 177.22M

Source:

Google

Finance

September

22,

2016

Dick’s

Sporting

Goods,

Inc.(DKS/NYSE)

Dick’s

Sporting

Goods,

Inc.,

is

one

of

the

largest

players

in

the

sporting

goods

market.

Dick’s

was

founded

in

1948

and

is

currently

headquartered

in

Coraopolis,

Pennsylvania.

It

has

a

market

capitalization

of

$6.94

billion

and

operates

in

all

50

states.

Dick’s

primary

operations

consist

of

sales

in

equipment,

apparel,

footwear,

and

other

sports

accessories.

Additionally,

it

has

subsidiaries

in

a

range

of

specialty

sports

stores.

Big

5

Sporting

Goods

Corporation

(BGFV/NASDAQ)

Big

5

Sporting

Goods

is

a

major

player

in

sporting

goods

retail

for

Western

America.

The

company

currently

operates

approximately

440

stores

in

over

ten

different

states.

Big

5

operates

as

a

retailer

for

big

merchandising

brands

as

well

as

selling

private

merchandise

under

its

various

trademarks.

The

company

also

sells

merchandise,

specialty

sports

equipment,

and

footwear

through

its

online

platform.

Compared

to

the

industry,

Big

5

stores

are

significantly

smaller

than

the

competition,

averaging

11,000

square

feet

per

store.

However,

Big

5

is

known

for

its

diverse

range

of

brands

throughout

its

stores.

Cabela’s

Incorporated

(NYSE:

CAB)

Cabela’s

Incorporated

is

a

specialty

outdoor

activities

retailer

made

up

of

three

business

segments.

Headquartered

in

Sidney,

Nebraska,

Cabela’s

operates

77

retail

stores

in

the

U.S.

and

Canada.

Its

two

primary

forms

of

revenue

generation

consist

of

the

retail

and

the

direct.

13. Hibbett

Sports

Incorporated

(HIBB)

BURKENROAD

REPORTS

(www.burkenroad.org)

November

16,

2016

13

The

retail

segment

consists

of

in-‐stores

sales

while

the

direct

segment

is

composed

of

e-‐

commerce

and

mail

catalogs.

Both

segments

sell

primarily

outdoor

apparel,

equipment,

footwear,

and

technology.

The

third

business

segment

performed

by

Cabela’s

is

Financial

Services.

This

segment

offers

credit

cards

and

other

financing

options.

Academy

Sports

+

Outdoors

(Private)

Academy

Sports

+

Outdoors

is

one

of

the

largest

private

retailers.

Academy

operates

approximately

200

stores

in

over

15

states

with

$4.6

billion

in

revenue

throughout

the

south

and

southwest.

Operations

primarily

consist

of

sports,

outdoor

activities,

and

lifestyle

products.

In

August

2011,

Academy

Sports

+

Outdoors

was

acquired

by

Kohlberg

Kravis

Roberts

&

Co

L.P.,

a

private

equity

firm.

Academy

emphasizes,

convenience,

quality,

and

service

throughout

the

customer

experience.

MANAGEMENT

PERFORMANCE

AND

BACKGROUND

Hibbett

Sports,

Inc.’s

top

level

management

has

significant

experience

and

knowledge

of

the

sporting

goods

industry

which

allows

for

continued

growth

of

the

Company.

Jeffry

O.

Rosenthal

Chief

Executive

Officer,

President

(58)

Jeffry

Rosenthal

is

currently

Hibbett’s

Chief

Executive

Officer

(CEO)

as

well

as

President

and

Chief

Operating

Officer

(COO).

He

was

promoted

from

Vice

President

of

Merchandising

to

the

duties

of

CEO

in

2010

and

has

retained

that

position

to

date.

Mr.

Rosenthal

has

served

as

President

and

and

COO

since

2009.

In

2014,

Mr.

Rosenthal

was

nominated

for

CEO

of

the

year

by

the

Alabama

Retail

Association.

He

was

awarded

the

Silver

award,

which

recognizes

the

CEO

that

reaches

annual

sales

of

more

than

$20

million.

Mr.

Rosenthal

previously

worked

for

a

sporting

goods

company

named

Champs

Sports,

where

he

held

the

position

of

Vice

President

of

Divisional

Merchandise

(DMM)

for

apparel

from

1981

to

1998.

Scott

J.

Bowman

Senior

Vice

President,

Chief

Financial

Officer,

Principal

Accounting

Officer

(49)

Scott

Bowman

has

been

Hibbett’s

Chief

Financial

Officer

and

Senior

Vice

President

since

July

2012.

Mr.

Bowman’s

expertise

comes

from

his

work

as

a

financial

leader

of

a

795

store

division

that

represented

$25

billion

in

annual

sales.

Prior

to

joining

Hibbett

Sports,

Mr.

Bowman

served

as

Home

Depot’s

Division

Chief

Financial

Officer

for

three

years.

Cathy

E.

Pryor

Senior

Vice

President

of

Operations

(53)

Cathy

Pryor

has

been

with

Hibbett

Sports

since

1988

where

she

served

as

a

District

Manager

and

Director

of

Store

Operations.

From

1995

to

2012,

Ms.

Pryor

was

the

Vice

President

of

Operations

and

eventually

earned

the

title

of

Senior

Vice

President

of

Operations.

14. Hibbett

Sports

Incorporated

(HIBB)

BURKENROAD

REPORTS

(www.burkenroad.org)

November

16,

2016

14

Jared

S.

Briskin

Senior

Vice

President

and

Chief

Merchant

(43)

Jared

Briskin

was

named

Senior

Vice

President

and

Chief

Merchant

at

Hibbett

Sports

in

2014.

Before

then,

he

served

as

the

Vice

President

of

Apparel

and

Equipment

at

Hibbett

Sports

from

2004

to

2010.

In

2010,

he

was

promoted

to

Vice

President

of

Footwear

and

Equipment.

He

retained

that

position

until

his

2014

promotion

to

Senior

Vice

President

and

Chief

Merchant.

Michael

J.

Newsome

Non

Executive

Chairman

of

the

Board

(75)

Michael

Newsome

is

currently

a

non-‐independent

Director

of

Hibbett’s

Board

and

has

been

a

member

since

1996.

In

1981,

Mr.

Newsome

was

the

President

of

Hibbett

Sports

and

in

1999

he

was

named

the

Chief

Executive

Officer.

In

2004,

he

was

named

as

the

Chairman

of

the

Board.

Mr.

Newsome

held

his

positions

until

2010.

In

2014,

Mr.

Newsome

resigned

from

his

executive

management

positions

to

serve

as

the

Chairman

of

the

Board.

In

2007

the

National

Sporting

Goods

Association

inducted

Mr.

Newsome

into

the

Sporting

Goods

Industry

Hall

of

Fame.

Mr.

Newsome

had

a

pivotal

role

in

the

transformation

of

Hibbett

Sports

from

a

small

privately

owned

retailer

to

the

successful

public

company

it

is

today.

Return

on

Invested

Capital

(ROIC)

Return

on

invested

capital

(ROIC)

measures

the

Company’s

ability

to

generate

cash

flows

relative

to

their

invested

capital.

This

measurement

allows

investors

to

view

how

well

a

company

uses

its

own

money

to

generate

returns.

Table

3

shows

the

five

year

ROIC

of

Hibbett

Sports

and

their

comparable

companies.

Hibbett

Sports

Inc.

has

a

higher

ROIC

for

every

year

as

compared

to

the

peer

average.

Table

3:

Return

on

Invested

Capital

Company Ticker 2015 2014 2013 2012 2011

Hibbett

Sports

Inc. HIBB 22.01% 23.33% 25.86% 32.46% 28.98%

Dick’s

Sporting

Goods

Inc. DKS 18.33% 19.57% 20.56% -‐-‐-‐-‐-‐-‐-‐-‐-‐-‐ 16.56%

Big

5

Sporting

Goods

Corporation BGFV 6.32% 6.38% 12.38% 7.41% 6.24%

Cabela’s

Incorporated CAB 3.29% 4.20% 5.75% 5.15% 4.70%

Peer

Average 9.31% 10.05% 12.90% 6.28% 9.17%

Source:

Thomson

One

September

22,

2016

15. Hibbett

Sports

Incorporated

(HIBB)

BURKENROAD

REPORTS

(www.burkenroad.org)

November

16,

2016

15

Management

Compensation

Hibbett

Sports’

Management

compensation

panel

has

an

extensive

procedure

when

setting

goals

and

guidelines

to

motivate

its

executive

officers

to

improve

performance

from

past

years.

This

panel

is

specifically

responsible

for

managing

the

guidelines

for

the

compensation

program

as

well

as

managing

equity

bonuses

for

executive

officers.

Factors

considered

include

performance-‐based

cash

bonuses,

performance

based

equity

awards,

and

base

salary.

The

panel

warrants

competitive

compensation

by

evaluating

a

group

of

equally

qualified

executives

from

22

peer

companies.

The

executive’s

compensation

correlates

with

the

progress

of

the

Company

as

well

as

making

sure

the

executives

are

always

doing

what

is

best

for

the

shareholders.

The

program

ensures

that

equity

awards

and

cash

bonuses

account

for

a

higher

portion

of

the

total

compensation

to

keep

these

executives

motivated

for

the

right

reasons.

Each

executive

position

payment

is

calculated

individually,

which

takes

into

account

factors

such

as

the

responsibility

of

the

executive

officer,

tenure,

performance,

and

the

amount

of

Company

stated

goals

achieved.

Overall

compensation

is

evaluated

by

Hibbett

Sports

performance

goal

and

earnings

before

interest

and

taxes

(EBIT),

which

is

found

in

Table

4.

The

Compensation

Panel’s

idea

of

“pay

for

performance”

allows

named

executive

officers

(NEOs)

to

receive

annual

cash

bonuses

based

on

the

Company’s

targeted

EBIT.

Table

4

shows

the

relationship

between

NEO’s

percentage

earning

of

performance

bonuses

and

the

Company’s

EBIT

goal

for

the

fiscal

years

of

2014,

2015

and

2016,

respectively.

Table

4:

Estimated

Bonuses

according

to

EBIT

Goal

Attained

%

of

Company

Performance

Goal

Attained

%

of

Executive’s

Performance

Bonus

Earned

Below

85.0% 0.0%

85.0% 62.5%

90.0% 75.0%

95.0% 87.5%

100.0% 100.0%

105.0% 112.5%

110.0% 125.0%

115.0% 137.5%

120.0%

or

above 150.0%

Source:

Hibbett

Sports

Proxy

Statement

Fiscal

Year

2016

16. Hibbett

Sports

Incorporated

(HIBB)

BURKENROAD

REPORTS

(www.burkenroad.org)

November

16,

2016

16

Table

5

shows

the

past

three

fiscal

years

of

how

percentage

payout

for

NEOs

is

affected

by

the

Company’s

EBIT:

Table

5:

Annual

EBIT

Goals

and

Achievements

EBIT

Goal EBIT

Achieved %

of

Goal

Achieved %

of

Payout

Fiscal

2016 $123.0

Million $110.1

Million 89.0% 72.5%

Fiscal

2015 $119.0

Million $118.1

Million 99.3% 97.5%

Fiscal

2014 $122.1

Million $113.9

Million 93.3% 82.5%

Source:

Hibbett

Sports

Proxy

Statement

Fiscal

Year

2016

SHAREHOLDER

ANALYSIS

As

of

September

21,

2016,

Hibbett

Sports

Inc.

had

21,987,475

shares

outstanding

with

a

free

float

of

21,748,644.

Additionally,

Hibbett

had

436

shareholders,

of

which

the

ten

largest

are

from

the

U.S.

(see

Table

6).

Fidelity

Management

&

Research

Company

remains

the

largest

stakeholder

owning

15.30%

of

shares

outstanding.

TimesSquareCapital

became

a

new

investor

this

calendar

year

and

now

owns

5.78%

of

shares

outstanding.

In

the

last

three

months,

Times

Square

Capital

has

increased

its

stake

in

the

Company

by

purchasing

429,850

common

shares

outstanding.

Hibbett’s

shares

are

primarily

controlled

by

the

top

ten

shareholders.

These

shareholders

own

69.85%

of

shares

outstanding

and

all

except

Arrowpoint

Asset

Management,

LLC

have

a

low

turnover

rate.

This

low

turnover

rate

keeps

Hibbett’s

stock

stable

and

active

with

a

three

month

average

daily

trading

volume

of

393,780

shares.

Table

6:

Hibbett’s

Largest

Shareholders

Holder

Name

%

O/S Shares

Held %

Change

(YTD)

Fidelity

Management

&

Research

Company 15.30 3,363,207 (6.23)

BlackRock

Institutional

Trust

Company,

N.A. 9.41 2,068,044 1.66

Arrowpoint

Asset

Management,

LLC

8.47 1,861,518 39.17

The

Vanguard

Group,

Inc. 8.23 1,808,753 (0.36)

Neuber

Berman,

LLC

6.92 1,521,530 (6.46)

TimesSquare

Capital

Management,

LLC

5.78 1,270,150 100

Epoch

Investment

Partners,

Inc. 4.75 1,045,343 6.22

ClearBridge

Investments,

LLC

3.90 858,284 (3.73)

GW&K

Investment

Management

3.71 815,472 (0.54)

Champlain

Investment

Partners,

LLC

3.38 743,005 (13.38)

Total

69.85 15,355,306

Source:

Thompson

One

September,

21

2016

17. Hibbett

Sports

Incorporated

(HIBB)

BURKENROAD

REPORTS

(www.burkenroad.org)

November

16,

2016

17

Stock

Repurchase

Program

Hibbett

has

not

historically

issued

dividends

and

does

not

plan

to

do

so

in

the

coming

years.

Instead,

the

Company

has

a

history

of

repurchasing

stocks.

In

November

2012,

the

Board

of

Directors

authorized

a

$250

million

Stock

Repurchase

Program.

In

November

2015,

this

authorization

was

replaced

by

a

new

Stock

Repurchase

Plan.

This

program

authorized

the

repurchase

of

$300

million

common

stocks

through

February

2,

2019.

During

the

13

weeks

ended

July

30,

2016,

Hibbett

repurchased

620,455

shares

of

common

stock

at

a

cost

of

$27.9

million.

As

of

July

30,

2016,

Hibbett

had

approximately

$271.2

million

remaining

under

the

Stock

Repurchase

Program.

RISK

ANALYSIS

AND

INVESTMENT

CAVEATS

Hibbett’s

future

success

is

challenged

by

multiple

risks.

These

risk affect

management

strategies

and

could

potentially

limit

growth.

Hibbett’s

risk

can

be

broken

into

two

main

groups:

Operational

Risk

and

Financial

and

Governmental

Risk.

Many

of

these

risks

can

be

attributed

to

the

retail

sporting

goods

industry;

however,

others

are

unique

to

Hibbett

because

of

its

size,

location,

and

strategic

position.

Operational

Risk

Economic

Hibbett’s

sales

primarily

come

from

customers’

discretionary

spending.

This

dependence

on

discretionary

spending

makes

Hibbett

susceptible

to

economic

factors

such

as

interest

rates,

inflation,

housing,

prices,

and

taxes.

Many

of

the

economic

risks

are

outside

of

Hibbett’s

control

and,

therefore,

cannot

be

completely

mitigated.

Any

major

disruption

in

the

U.S.

economy

or

financial

markets

would

likely

lead

to

decreased

sales

as

well

as

smaller

profit

margins.

Seasonality

Similar

to

other

retailers,

Hibbett

faces

seasonal

fluctuations

in

revenue.

Due

to

holiday

buying

patterns,

the

Company

consistently

records

its

highest

sales

in

the

first

and

fourth

quarters.

Specifically,

customers

increase

purchasing

directly

before

the

December

holidays.

First

quarter

sales

are

credited

to

New

Year’s

resolutions

to

get

in

shape

and,

thus,

purchase

workout

gear

and

equipment.

An

economic

decline

during

either

of

these

periods

would

likely

adversely

affect

the

Company’s

earnings

to

a

greater

extent

than

if

a

downturned

occurred

during

the

second

or

third

quarter

of

the

year.

Additionally,

merchandising

apparel

can

lead

to

an

increase

in

sales

if

a

regional

team

has

a

successful

sports

season.

Along

the

same

lines,

if

a

team

is

underperforming,

apparel

sales

can

be

significantly

lower

than

average.

Furthermore,

any

trends

or

new

products

can

cause

temporary

spikes

in

sales.

18. Hibbett

Sports

Incorporated

(HIBB)

BURKENROAD

REPORTS

(www.burkenroad.org)

November

16,

2016

18

Vendors

Hibbett

relies

on

a

select

number

of

key

vendors

to

supply

its

products.

This

selection

process

is

a

direct

result

of

customers

preferring

top

brands.

As

such,

Hibbett

is

dependent

on

maintaining

strong

relationships

with

its

major

vendors

and

manufacturers.

In

fact,

Hibbett’s

top

three

vendors

account

for

over

70%

of

products

purchased.

A

major

risk

would

be

any

conflict

in

these

relationships.

If

such

a

conflict

were

to

occur,

Hibbett

would

experience

operational

declines

as

they

search

for

new

vendors.

If

the

new

vendors

were

not

of

the

same

quality

as

the

existing

vendors,

these

operational

declines

could

persist

into

the

future.

Furthermore,

when

a

product

is

limited

by

supply

rather

than

demand,

a

vendor’s

allocation

of

products

among

retailers

plays

a

major

role

in

sales.

Continuing

a

strong

relationships

with

its

vendors

will

give

Hibbett

an

advantage

on

new

product

launches

and

will

help

Hibbett

keep

pace

with

market

trends.

Imported

Goods

Most

of

Hibbett’s

vendors

produce

and

import

a

large

majority

of

products

from

foreign

countries.

These

imported

goods

are

less

expensive

than

domestically

made

products

and

contribute

positively

to

Hibbett’s

profit

margins.

If

imported

goods

increase

in

price

or

become

unavailable,

the

Company’s

profit

margins

would

suffer

significantly.

Additionally,

the

domestic

products

used

to

supplement

the

foreign

products

may

be

of

a

lesser

quality

than

those

our

vendors