Cash conversion cycle, cash budget

•Download as DOCX, PDF•

2 likes•585 views

The document discusses the cash conversion cycle (CCC), which describes the flow of cash through a company as it purchases inventory, sells products to customers, and collects payment. The CCC has three components: inventory conversion period, average collection period, and payables deferral period. It also discusses calculating a target CCC and actual CCC, as well as cash budgeting and cash management techniques to efficiently use cash and maintain appropriate target cash balances.

Recommended

More Related Content

What's hot

What's hot (19)

Viewers also liked

Viewers also liked (20)

Similar to Cash conversion cycle, cash budget

Similar to Cash conversion cycle, cash budget (20)

More from Arshad Islam

More from Arshad Islam (20)

Recently uploaded

Recently uploaded (20)

Cash conversion cycle, cash budget

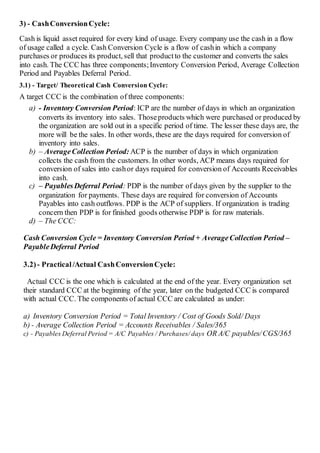

- 1. 3) - CashConversionCycle: Cash is liquid asset required for every kind of usage. Every company use the cash in a flow of usage called a cycle. Cash Conversion Cycle is a flow of cashin which a company purchases or produces its product, sell that productto the customer and converts the sales into cash. The CCC has three components;Inventory Conversion Period, Average Collection Period and Payables Deferral Period. 3.1) - Target/ Theoretical Cash Conversion Cycle: A target CCC is the combination of three components: a) - Inventory Conversion Period: ICP are the number of days in which an organization converts its inventory into sales. Thoseproducts which were purchased or produced by the organization are sold out in a specific period of time. The lesser these days are, the more will be the sales. In other words, these are the days required for conversion of inventory into sales. b) – AverageCollection Period: ACP is the number of days in which organization collects the cash from the customers. In other words, ACP means days required for conversion of sales into cashor days required for conversion of Accounts Receivables into cash. c) – PayablesDeferral Period: PDP is the number of days given by the supplier to the organization for payments. These days are required for conversion of Accounts Payables into cash outflows. PDP is the ACP of suppliers. If organization is trading concern then PDP is for finished goods otherwise PDP is for raw materials. d) – The CCC: Cash Conversion Cycle = Inventory Conversion Period + AverageCollection Period – PayableDeferral Period 3.2)- Practical/Actual CashConversionCycle: Actual CCC is the one which is calculated at the end of the year. Every organization set their standard CCC at the beginning of the year, later on the budgeted CCC is compared with actual CCC. The components of actual CCC are calculated as under: a) Inventory Conversion Period = Total Inventory / Cost of Goods Sold/ Days b) - Average Collection Period = Accounts Receivables / Sales/365 c) - Payables Deferral Period = A/C Payables / Purchases/ days OR A/C payables/CGS/365

- 2. 4) - CashBudget: Cash is most commonly used asset in every organization. There must be a properschedule for the usage of cash and acquisition of cash. Cash budget is a tool to measure the usage of cash on monthly and weekly basis. Monthly budget: Descriptions June July August Septembe r Novembe r Decembe r GrossSales *** *** *** *** *** *** Receiptsfrom Sales: 1-5 months *** *** *** *** *** *** 6-12 months *** *** *** ** *** *** Otherreceipts ** *** *** *** *** *** Total Cash received Payments: Expenses: *** *** *** *** *** *** Purchases: *** *** *** *** *** *** Total Cash paid Netcash inhand 5) - CashManagementand TargetCashbalances: Cash is required for daily operations and contingencies. There should be properway to manage the cash in an efficient way. Since cash is liquid asset and it is used in each area of life there should be a proper toolof managing the cash. For are some areas of cash management. I) - Reasonsforholding cash: There are different reasons for cash holding. All these reasons are categorized in three heads: - TransactivePurpose: When cash is held for daily operations, such as purchases, sales, advertisement and productions etc. This Transactive purposeis called transaction balances. Sometimes cash is kept for covering the difference of cashinflow and outflow. In order to keep a balance for precautions is called precautionary balances. - BankingPurpose: Bank needs cashas bank charges and minimum account balances. Cash is required for maintaining minimum balances and making charges for banks. - SpeculativePurpose: A special amount of balance is also required for investment opportunities. Sometimes a productive use of cash arises in the market but business faces shortage of cash, due to which business losses the opportunity. If organization keep a special amount of balance then it can avail such opportunities.

- 3. II) - CashManagementTechniques: For efficient use of cash there are different techniques. Some of them are discussed as under: - Synchronizing CashFlows: Synchronizing is the process ofdesigning the stream of cash flows in such a way to keep a special balance of cash. If cash flows are equal then company may not be able to keep balance. A budget is designed to organize the gap of inflow and outflow. - Speeding up the cheque-clearing process: An unclear cheque is nothing more than a paper. If the process ofcheque clearance is designed then the organization can covert there cash into accounts with speed. The bank accounts are fast updates and the payment is made. - ManagingFloats: Float is the difference of pass bookand cash book. Sometimes the cash bookis overstated. The company makes payment on the basis of cash bookbut pass bookis appeared with different balance. In order to cover such a float, company keeps a balance to equalize the gaps. - Speeding Collections: The most important task of the business is to recover the cash. Company grows on sales but it runs on cash. The collection of cash must be properly managed to run the company. It can be improved by direct credit system or lock box systems. In both of these systems cash is sent to bank directly rather than sending it to the company. - Cash Accounts: Maintenance of cash account is very important to have a good command over the cash management. Cash account is prepared on daily basis for finding the net balances on cash. If company knows how much cash is needed then it will be able to arrange that. Cash account lets the company know how much cash is available. - Petty Control: Daily expenses also waste a handsome amount of cash. A petty budget is prepared to control over the cash. If a petty budget is prepared then the extra amount is used in a better alternative of usage otherwise the cash is always misused.