12 March Daily market report

•

0 likes•301 views

The QE index in Qatar declined 1.4% led by losses in the Consumer Goods & Services and Banks & Financial Services indices. Qatar International Islamic Bank and Qatar General Insurance & Reinsurance Co. fell 4.9% each. Volume traded rose slightly while trading activity was higher than the 30-day average. Regional indices also declined except for Saudi Arabia. News from Qatar included projects market momentum, Barwa Real Estate reporting increased profits, Muntajat signing a shipping contract, and corporate events from banks and insurers.

Recommended

More Related Content

What's hot

What's hot (20)

Viewers also liked

Similar to 12 March Daily market report

Similar to 12 March Daily market report (20)

More from QNB Group

More from QNB Group (20)

Recently uploaded

Recently uploaded (20)

12 March Daily market report

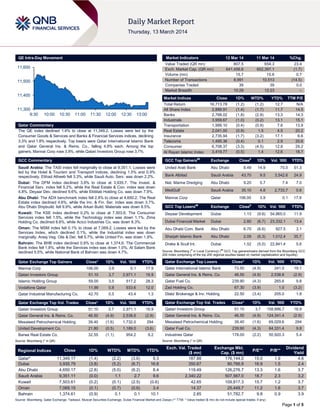

- 1. Page 1 of 5 QE Intra-Day Movement Qatar Commentary The QE index declined 1.4% to close at 11,349.2. Losses were led by the Consumer Goods & Services and Banks & Financial Services indices, declining 3.3% and 1.8% respectively. Top losers were Qatar International Islamic Bank and Qatar General Ins. & Reins. Co., falling 4.9% each. Among the top gainers, Mannai Corp rose 3.9%, while Qatari Investors Group rose 3.7%. GCC Commentary Saudi Arabia: The TASI index fell marginally to close at 9,351.1. Losses were led by the Hotel & Tourism and Transport indices, declining 1.5% and 0.9% respectively. Etihad Atheeb fell 3.3%, while Saudi Auto. Serv. was down 2.2%. Dubai: The DFM index declined 3.8% to close at 3,935.7. The Invest. & Financial Serv. index fell 5.2%, while the Real Estate & Con. index was down 4.8%. Deyaar Dev. declined 9.6%, while Ekttitab Holding Co. was down 7.9%. Abu Dhabi: The ADX benchmark index fell 2.8% to close at 4,650.2. The Real Estate index declined 4.6%, while the Inv. & Fin. Ser. index was down 3.7%. Abu Dhabi Shipbuild. fell 9.9%, while Arkan Build. Materials was down 8.5%. Kuwait: The KSE index declined 0.2% to close at 7,503.6. The Consumer Services index fell 1.5%, while the Technology index was down 1.1%. Zima Holding Co. declined 8.8%, while Acico Industries Co. was down 8.3%. Oman: The MSM index fell 0.1% to close at 7,069.2. Losses were led by the Services Index, which declined 0.1%, while the Industrial index was down marginally. Areej Veg. Oils & Der. fell 5.7%, while United Fin. was down 1.9%. Bahrain: The BHB index declined 0.9% to close at 1,374.6. The Commercial Bank index fell 1.8%, while the Services index was down 1.0%. Al Salam Bank declined 5.5%, while National Bank of Bahrain was down 4.7%. Qatar Exchange Top Gainers Close* 1D% Vol. ‘000 YTD% Mannai Corp 106.00 3.9 0.1 17.9 Qatari Investors Group 51.10 3.7 2,971.1 16.9 Islamic Holding Group 59.00 3.5 517.2 28.3 Vodafone Qatar 11.99 0.8 933.6 12.0 Qatar Industrial Manufacturing Co. 42.70 0.5 43.4 1.3 Qatar Exchange Top Vol. Trades Close* 1D% Vol. ‘000 YTD% Qatari Investors Group 51.10 3.7 2,971.1 16.9 Qatar General Ins. & Reins. Co. 46.50 (4.9) 2,538.6 (2.9) Mesaieed Petrochemical Holding 39.40 (1.6) 1,732.0 294 United Development Co. 21.80 (0.5) 1,189.0 (3.6) Barwa Real Estate Co. 32.55 (1.1) 954.2 9.2 Source: Bloomberg (* in QR) Market Indicators 12 Mar 14 11 Mar 14 %Chg. Value Traded (QR mn) 807.5 654.3 23.4 Exch. Market Cap. (QR mn) 641,456.6 652,397.1 (1.7) Volume (mn) 15.7 15.6 0.7 Number of Transactions 8,991 10,513 (14.5) Companies Traded 39 39 0.0 Market Breadth 10:29 12:23 – Market Indices Close 1D% WTD% YTD% TTM P/E Total Return 16,713.78 (1.2) (1.2) 12.7 N/A All Share Index 2,889.91 (1.4) (1.7) 11.7 14.5 Banks 2,768.02 (1.8) (2.9) 13.3 14.3 Industrials 3,959.67 (1.0) (0.2) 13.1 15.1 Transportation 1,999.10 (0.4) (0.9) 7.6 13.9 Real Estate 2,041.00 (0.9) 1.5 4.5 20.2 Insurance 2,735.94 (1.7) (3.2) 17.1 6.6 Telecoms 1,495.36 (0.4) 0.1 2.9 20.6 Consumer 6,708.37 (3.3) (4.5) 12.8 29.2 Al Rayan Islamic Index 3,419.77 (0.5) 1.4 12.6 18.7 GCC Top Gainers## Exchange Close# 1D% Vol. ‘000 YTD% United Arab Bank Abu Dhabi 8.49 14.9 75.0 51.3 Bank Albilad Saudi Arabia 43.70 9.5 3,542.6 24.9 Nat. Marine Dredging Abu Dhabi 9.20 5.7 7.4 7.0 MedGulf Saudi Arabia 35.10 4.8 2,733.7 0.6 Mannai Corp Qatar 106.00 3.9 0.1 17.9 GCC Top Losers## Exchange Close# 1D% Vol. ‘000 YTD% Deyaar Development Dubai 1.13 (9.6) 54,865.0 11.9 Dubai Financial Market Dubai 2.80 (6.7) 23,332.1 13.4 Abu Dhabi Com. Bank Abu Dhabi 6.70 (6.6) 927.5 3.1 Sharjah Islamic Bank Abu Dhabi 2.09 (6.3) 1,012.4 35.7 Drake & Scull Int. Dubai 1.52 (5.0) 22,841.4 5.6 Source: Bloomberg ( # in Local Currency) ( ## GCC Top gainers/losers derived from the Bloomberg GCC 200 Index comprising of the top 200 regional equities based on market capitalization and liquidity) Qatar Exchange Top Losers Close* 1D% Vol. ‘000 YTD% Qatar International Islamic Bank 73.50 (4.9) 241.0 19.1 Qatar General Ins. & Reins. Co. 46.50 (4.9) 2,538.6 (2.9) Qatar Fuel Co. 239.90 (4.3) 265.6 9.8 Zad Holding Co. 67.30 (3.9) 1.0 (3.2) Dlala' Brokerage & Inv. Holding 22.50 (3.4) 205.0 1.8 Qatar Exchange Top Val. Trades Close* 1D% Val. ‘000 YTD% Qatari Investors Group 51.10 3.7 158,886.7 16.9 Qatar General Ins. & Reins. Co. 46.50 (4.9) 124,341.4 (2.9) Mesaieed Petrochemical Holding 39.40 (1.6) 69,029.6 294 Qatar Fuel Co. 239.90 (4.3) 64,331.4 9.8 Industries Qatar 178.00 (2.2) 50,920.3 5.4 Source: Bloomberg (* in QR) Regional Indices Close 1D% WTD% MTD% YTD% Exch. Val. Traded ($ mn) Exchange Mkt. Cap. ($ mn) P/E** P/B** Dividend Yield Qatar* 11,349.17 (1.4) (2.2) (3.6) 9.3 187.88 176,144.0 15.0 1.9 4.6 Dubai 3,935.79 (3.8) (5.2) (6.7) 16.8 350.67 80,766.9 16.9 1.5 2.4 Abu Dhabi 4,650.17 (2.8) (5.0) (6.2) 8.4 119.49 126,276.7 13.3 1.6 3.7 Saudi Arabia 9,351.11 (0.0) 1.1 2.7 9.6 2,340.22 507,567.0 18.7 2.3 3.2 Kuwait 7,503.61 (0.2) (0.1) (2.5) (0.6) 42.65 109,817.3 15.7 1.2 3.7 Oman 7,069.15 (0.1) (0.7) (0.6) 3.4 14.37 25,449.7 11.2 1.6 3.7 Bahrain 1,374.61 (0.9) 0.1 0.1 10.1 2.85 51,782.7 9.8 0.9 3.9 Source: Bloomberg, Qatar Exchange, Tadawul, Muscat Securities Exchange, Dubai Financial Market and Zawya (** TTM; * Value traded ($ mn) do not include special trades, if any) 11,300 11,400 11,500 11,600 9:30 10:00 10:30 11:00 11:30 12:00 12:30 13:00

- 2. Page 2 of 5 Qatar Market Commentary The QE index declined 1.4% to close at 11,349.2. The Consumer Goods & Services and Banks & Financial Services indices led the losses. The index fell on the back of selling pressure from Qatari shareholders despite buying support from non-Qatari shareholders. Qatar International Islamic Bank and Qatar General Ins. & Reins. Co. were the top losers, falling 4.9% each. Among the top gainers, Mannai Corp rose 3.9%, while Qatari Investors Group rose 3.7%. Volume of shares traded on Wednesday rose by 0.7% to 15.7mn from 15.6mn on Tuesday. Further, as compared to the 30-day moving average of 13.2mn, volume for the day was 19.3% higher. Qatari Investors Group and Qatar General Ins. & Reins. Co. were the most active stocks, contributing 18.9% and 16.1% to the total volume respectively. Source: Qatar Exchange (* as a % of traded value) Global Economic Data Global Economic Data Date Market Source Indicator Period Actual Consensus Previous 03/12 US MBA MBA Mortgage Applications 7-March -2.10% – 9.40% 03/12 EU Eurostat Industrial Production SA MoM January -0.20% 0.50% -0.40% 03/12 EU Eurostat Industrial Production WDA YoY January 2.10% 1.90% 1.20% 03/12 France INSEE Non-Farm Payrolls QoQ 4Q2013 0.10% 0.10% 0.10% 03/12 Spain INE CPI EU Harmonised MoM February -0.10% -0.20% -1.80% 03/12 Spain INE CPI EU Harmonised YoY February 0.10% 0.00% 0.00% 03/12 Spain INE CPI Core MoM February 0.00% – -1.70% 03/12 Spain INE CPI Core YoY February 0.10% 0.10% 0.20% 03/12 Spain INE CPI MoM February 0.00% -0.10% -1.30% 03/12 Spain INE CPI YoY February 0.00% -0.10% -0.10% 03/12 Japan METI Tertiary Industry Index MoM January 0.90% 0.60% -0.50% 03/12 Japan Ministry of Finance BSI Large All Industry QoQ 1Q2014 12.7 – 8.3 03/12 Japan Ministry of Finance BSI Large Manufacturing QoQ 1Q2014 12.5 – 9.7 03/12 Japan ESRI Consumer Confidence Index February 38.3 40.0 40.5 Source: Bloomberg (s.a. = seasonally adjusted; n.s.a. = non-seasonally adjusted; w.d.a. = working day adjusted) News Qatar MEED: Qatar’s projects market sees upswing – Qatar‟s investments in various projects in the energy and infrastructure sectors have seen a remarkable boost over the last six months, with a host of new developments being announced and existing projects moving forward. MEED said under the new leadership of HH the Emir Sheikh Tamim bin Hamad al-Thani, momentum in Qatar‟s projects market has seen an upswing with a wide range of developmental projects announced. This includes $13bn in petrochemical schemes, intensification in upstream operations, extension of life of its mature oil fields, and infrastructure project opportunities worth $40bn such as roads, ports and rail work, as well as $19bn construction projects, and $3.2bn of social infrastructure projects. (Gulf-Times.com) BRES posts QR1.37bn in net profit – Barwa Real Estate Company (BRES) has posted a net profit of QR1.37bn in 2013 versus QR1.14bn in 2012. The EPS amounted to QR3.53 for 2013 compared to QR2.92 in 2012. The Board of Directors recommended distribution of cash dividend of QR2.00 per share vs. QR1.50 with the 2012 results. (QE) Muntajat, Milaha signs 2-year transport contract – Qatar Chemical and Petrochemical Marketing & Distribution Company (Muntajat) signed a two-year agreement with Qatar Navigation (Milaha) to transport petrochemicals shipments from Qatar. The agreement covers containerized exports of polymers and melamine from Mesaieed to key hub ports in the region. The total annual volume of exports is expected to reach around 150,000 TEU (twenty foot equivalent units). (Peninsula Qatar) Qatari Diar to open US office to explore investments – Qatari Diar Real Estate Investment Company will open a regional office in Washington DC later in 2014 to pursue new strategic investments throughout the western hemisphere. Qatari Diar‟s Group CEO Khaled Mohamed al-Sayed said that the company‟s new regional base will manage existing projects and explore other strategic investments within the North American region. (Gulf-Times.com) DOHI looks to expand in GCC market – Doha Insurance Company (DOHI) is seeking to expand its footprints beyond Qatar, especially in GCC countries. DOHI has already announced its plan to raise capital via a rights issue, which will help in its expansion plans. (Peninsula Qatar) QIIK’s AGM approves QR3.75 cash dividend – Qatar International Islamic Bank‟s (QIIK) AGM has approved the board of directors‟ recommendation for QR3.75 cash dividend. (QE) GISS approves 20% cash dividend, 25% bonus shares – Gulf International Services‟ (GISS) AGM has approved the Overall Activity Buy %* Sell %* Net (QR) Qatari 73.37% 73.84% (3,785,583.25) Non-Qatari 26.62% 26.15% 3,785,583.25

- 3. Page 3 of 5 board‟s recommendation for 20% cash dividend, representing QR2.00 per share and 25% bonus shares for 2013. (QE) QIGD appoints Chairman, Vice Chairman – The Qatari Investors Group (QIGD) has appointed Abdullah Bin Nasser Al Misnad as the company‟s Chairman and Sheikh Hamad Bin Faisal Al Thani as the Vice Chairman for the 2014-2016 period. (QE) QA launches four weekly flights to Cyprus – Qatar Airways will launch four weekly flights to Cyprus from 29 April 2014 as part of a recent agreement for strengthening air transport between Cyprus and Qatar. (Bloomberg) Qatargas loads 2,000th LNG cargo from Ras Laffan – Qatargas recently loaded the 2,000th LNG cargo from the Common Lean LNG Storage & Loading Asset facility at Ras Laffan. This milestone was achieved in less than five years since the first loading from the facility. (Gulf-Times.com) Qatar to benefit from two major Internet projects – Two huge internet cable projects, one submarine and one terrestrial, have been kicked off recently, which are expected to increase broadband capacity for the Gulf region (including Qatar). The first project is the new Southeast Asia-Middle East-Western Europe 5 (SEA-ME-WE 5), a 20,000-kilometer cable that will connect Asia, Africa and Europe. The Middle-East Europe Terrestrial System (MEETS) will start in 1Q2014, covering a consortium of providers such as Vodafone Qatar, Zain, Zajil, and du Telecom. (Gulf-Times.com) International US surprises oil market with sale from strategic reserves – The United States will hold the first test sale of crude oil from its emergency oil stockpile held since 1990, offering a modest 5mn barrels in what some observers saw as a subtle message to oil exporter, Russia. The US Energy Department said the test sale had been planned for months, which has been timed to meet demand from refiners coming out of annual maintenance cycles. However, oil traders noted that Russia's effort to take over the Crimea region from Ukraine has prompted calls for use of booming US energy resources to relieve Europe‟s dependence on Russian natural gas. Oil prices dipped to their lowest levels in a month after news of the test sale, which closes in two days. US Officials said the release would ensure that oil stored in vast salt caverns could still reach local refiners affected by recent changes in pipeline infrastructure. (Reuters) Reuters: British economy set to grow fastest among G7 – Britain's economy will grow faster than any other G7 nation in coming quarters, but the Bank of England (BoE) will not raise interest rates until next year to avoid choking off the recovery. A Reuters poll of over 50 economists suggested that Britain's GDP will grow 0.6% every quarter through to September 2015. Based on these forecasts, Britain's economy is set to reach its pre- crisis level by the end of June and be the fastest growing among the group of seven (G7) major industrialized nations. Britain's economy will expand 2.7% this year and 2.4% in 2015 and 2016, similar to forecasts made by the Organization for Economic Cooperation & Development (OECD). The Eurozone economy, Britain's main trading partner, is expected to grow by just 1.1% this year and 1.4% in 2015, with any deterioration in that growth becoming a key risk for Britain's growth. (Reuters) Germany sees balanced budget from 2015 – German Finance Minister Wolfgang Schaeuble unveiled plans to achieve a consistently balanced budget from 2015, the first time that the country will be spending less than its revenue intake since 1969. Schaeuble stated that the government wants to go out of this legislative period without any new budgetary debt. Germany will run up only a small public deficit of €6.5bn in 2014 – its smallest in 40 years – down from €22.1bn in 2013. However, Schaeuble said the country‟s budget will be balanced from next year at least until 2018 without taking any debt. (ET) OPEC raises 2014 global oil demand view – OPEC said the global oil demand will increase more than expected in 2014, raising its prediction for a second straight month as economic growth picks up in Europe and the US. The OPEC‟s view on oil demand growth is in contrast with that of the US, which has cut its forecast. In a monthly report, the OPEC stated that global demand will rise by 1.14mn bpd this year, up 50,000 bpd from its previous forecast. The group also raised its projection for global demand for OPEC's crude in 2014. The OPEC cited further signs of strong oil demand in the world's top consumer, the US, as well as a stabilizing rate of demand contraction in Europe – where oil consumption has been held back for years by weak economies. (Reuters) Italy presents sweeping tax cuts, plans to raise deficit goal – Italian Prime Minister Matteo Renzi presented a sweeping package of tax cuts, saying they can help in reviving the Eurozone's third largest economy without breaking the EU budget deficit limits. Renzi said income tax would be reduced by a total of €10bn annually for 10mn low and middle income workers from May 1. He further added that the cuts will be financed by reductions in the central government spending, extra borrowing and by resources freed up thanks to the recent fall in Italy's borrowing costs. (Reuters) Regional Saudi Arabia poised for S&P upgrade – Saudi Arabia is poised for a sovereign upgrade from Standard & Poor‟s (S&P) as central bank reserves of OPEC‟s biggest member swelled the most in the last five years, according to some financial institutions, such as, Credit Agricole Private Banking, Commerzbank and Riyadh-based MASIC. Credit default swaps for Saudi Arabia, rated AA- at S&P, stood at 63 basis points on March 11. The dollar-denominated debt from Saudi Electricity Company to Saudi Basic Industries Corp. rose after Fitch Ratings upgraded the country on March 7. The central bank‟s total reserves including cash and gold swelled to $720bn at the end of January. (Bloomberg) Samba arranges SAR7.2bn financing for Saudia – Samba Financial Group, along with a consortium of banks, has provided Shari‟ah-compliant financing facilities worth SR7.2bn to the Saudi Arabian Airlines (Saudia). The transaction enabled Saudia to purchase 26 aircraft of different types, which were added to its international fleet and raised its capacity to meet its expansion plans. The financing package provides Saudia the financial flexibility to boost its fleet strength, thereby empowering it to strengthen its presence within the growing commercial aviation sector in the region. (Bloomberg, Zawya) GE Power Conversion to supply components to SEC – GE Power Conversion will supply efficient and flexible components for the Saudi Electricity Company (SEC), in a contract worth $23mn. GE will be supplying twenty-four 18MW MV7000 variable speed drives to SEC‟s Jeddah South and Shuqaiq steam power plants. Each project consists of four 660-MW power blocks, which are considered to be the world‟s largest steam power plants. Hyundai Heavy Industries has been awarded the overall contract. (GulfBase.com) APC signs SR3,375mn contract with SK Gas – The Advanced Petrochemical Company (APC) has signed a MoU with SK Gas Company for setting up a state-of-the-art propane dehydrogenation plant in South Korea. The project cost is

- 4. Page 4 of 5 estimated to be around SR3,375mn. APC or its subsidiary, Advanced Global Investment Company, will hold a minimum of 25% equity stake in the plant. The plant is scheduled to begin operation in 1Q2016, with a design capacity of 600,000 metric tons of propylene per year. The MoU will become effective from March 12, 2014. (Tawadul) Al Basel Group launches investment arm – The Al Basel Group of Companies has launched its investment arm named „Amani Investments‟. The new company will offer financial and investment solutions for both companies and individuals in the UAE, Saudi Arabia and Qatar. Amani will serve mid-range and high-end clients by offering to manage their savings and assets portfolio as well as providing turnkey advice on investments in real estate and stocks. (GulfBase.com) Aviation plays key role in UAE-US trade – According to the US-UAE Business Council, trade between the US and the UAE reached $26.9bn in 2013, with commercial aviation partnerships playing a central role. Transportation equipment worth $9.4bn, including Boeing aircraft and GE engines, were the largest subset, making up for 38% of the total US exports to the UAE in 2013. (GulfBase.com) DEWA invests AED52bn in energy-efficiency projects – DEWA‟s Managing Director & Chief Executive, Saeed Mohammed Al Tayer, said that the authority has planned an estimated investment of AED52bn in energy-efficiency projects. The authority is building electricity and water distribution networks at a total investment of AED7bn to support its demand side management. (GulfBase.com) NBAD raises $358mn with second Kangaroo bond – National Bank of Abu Dhabi (NBAD) raised $358mn from its second Kangaroo bond sale, paying half a percentage point less for a five-year debt than what it did a year ago. According to ANZ Banking Group, the bonds which will mature in March 2019, were priced to yield 125 basis points more than the swap rate. According to ANZ prices, the lender‟s inaugural Kangaroo bond in February last year was priced at a spread of 175 basis points. The gap for those notes narrowed to 109 basis points as of today. (Bloomberg) DIC, DOZ add 181 firms in 2013 – Dubai Internet City (DIC) and Dubai Outsource Zone (DOZ) have added 181 new companies in 2013. DIC and DOZ are part of Tecom Investments, a member of Dubai Holding. There are 1,600 business partners including over 60% of the Fortune 500 companies in the sector covering software, hardware and internet services including Microsoft, Oracle, Dell, Facebook Hewlett Packard, DELL and IBM ME, as well as leading global multinational companies and local SMEs. The number of Fortune 500 companies based in DIC largely increased their presence over the course of 2013. (GulfBase.com) ADSB’s BoD recommends 10% cash dividend – Abu Dhabi Ship Building Company‟s (ADSB) board of directors has recommended the distribution of 10% cash dividend for 2013. (ADX) Sharjah Islamic declares AED242.6mn cash dividend – Sharjah Islamic Bank‟s (SIB) AGM has approved the distribution of 10% cash dividend amounting to AED242.6mn for 2013. (GulfBase.com) Gulf Mushroom declares 20% bonus shares – The Gulf Mushroom Products Company‟s AGM has approved its board of directors‟ recommendation for 20% bonus shares (2 bonus shares for every 10 shares). With this, the company‟s shares will increase from 22,651,200 to 27,181,440. (GulfBase.com) NPI declares 16% cash dividend – National Pharmaceutical Industries Company‟s (NPI) AGM has approved its board‟s proposal to distribute 16% cash dividend (OMR0.016 baiza per share) for 2013. (MSM) BBK declares 10% cash dividend, 10% bonus shares – The Bank of Bahrain & Kuwait‟s (BBK) AGM has approved the distribution of 10% cash dividend, amounting to 10 fils per share and 10% bonus shares to the shareholders. (Bahrain Bourse)

- 5. Contacts Saugata Sarkar Ahmed M. Shehada Keith Whitney Sahbi Kasraoui Head of Research Head of Trading Head of Sales Manager - HNWI Tel: (+974) 4476 6534 Tel: (+974) 4476 6535 Tel: (+974) 4476 6533 Tel: (+974) 4476 6544 saugata.sarkar@qnbfs.com.qa ahmed.shehada@qnbfs.com.qa keith.whitney@qnbfs.com.qa sahbi.alkasraoui@qnbfs.com.qa QNB Financial Services SPC Contact Center: (+974) 4476 6666 PO Box 24025 Doha, Qatar DISCLAIMER: This publication has been prepared by QNB Financial Services SPC (“QNBFS”) a wholly-owned subsidiary of Qatar National Bank (“QNB”). QNBFS is regulated by the Qatar Financial Markets Authority and the Qatar Exchange; QNB is regulated by the Qatar Central Bank. This publication expresses the views and opinions of QNBFS at a given time only. It is not an offer, promotion or recommendation to buy or sell securities or other investments, nor is it intended to constitute legal, tax, accounting, or financial advice. We therefore strongly advise potential investors to seek independent professional advice before making any investment decision. Although the information in this report has been obtained from sources that QNBFS believes to be reliable, we have not independently verified such information and it may not be accurate or complete. While this publication has been prepared with the utmost degree of care by our analysts, QNBFS does not make any representations or warranties as to the accuracy and completeness of the information it may contain, and declines any liability in that respect. QNBFS reserves the right to amend the views and opinions expressed in this publication at any time. It may also express viewpoints or make investment decisions that differ significantly from, or even contradict, the views and opinions included in this report. COPYRIGHT: No part of this document may be reproduced without the explicit written permission of QNBFS. Page 5 of 5 Rebased Performance Daily Index Performance Source: Bloomberg Source: Bloomberg Source: Bloomberg Source: Bloomberg 80.0 90.0 100.0 110.0 120.0 130.0 140.0 150.0 160.0 170.0 180.0 Jun-10 Jan-11 Aug-11 Mar-12 Oct-12 May-13 Dec-13 QE Index S&P Pan Arab S&P GCC (0.0%) (1.4%) (0.2%) (0.9%) (0.1%) (2.8%) (3.8%)(4.2%) (3.6%) (3.0%) (2.4%) (1.8%) (1.2%) (0.6%) 0.0% SaudiArabia Qatar Kuwait Bahrain Oman AbuDhabi Dubai Asset/Currency Performance Close ($) 1D% WTD% YTD% Global Indices Performance Close 1D% WTD% YTD% Gold/Ounce 1,366.83 1.3 2.0 13.4 DJ Industrial 16,340.08 (0.1) (0.7) (1.4) Silver/Ounce 21.30 2.2 1.9 9.4 S&P 500 1,868.20 0.0 (0.5) 1.1 Crude Oil (Brent)/Barrel (FM Future) 108.02 (0.5) (0.9) (2.5) NASDAQ 100 4,323.33 0.4 (0.3) 3.5 Natural Gas (Henry Hub)/MMBtu 4.66 0.1 (2.4) 7.3 STOXX 600 327.95 (1.1) (1.5) (0.1) North American Spot LPG Propane Price 109.00 (0.5) 0.5 (13.8) DAX 9,188.69 (1.3) (1.7) (3.8) North American Spot LPG Normal Butane Price 120.75 0.2 (0.2) (11.0) FTSE 100 6,620.90 (1.0) (1.4) (1.9) Euro 1.39 0.3 0.2 1.2 CAC 40 4,306.26 (1.0) (1.4) 0.2 Yen 102.76 (0.3) (0.5) (2.4) Nikkei 14,830.39 (2.6) (2.9) (9.0) GBP 1.66 0.0 (0.6) 0.4 MSCI EM 944.63 (1.2) (2.3) (5.8) CHF 1.14 0.5 0.5 2.2 SHANGHAI SE Composite 1,997.69 (0.2) (2.9) (5.6) AUD 0.90 0.1 (0.9) 0.8 HANG SENG 21,901.95 (1.7) (3.3) (6.0) USD Index 79.61 (0.2) (0.1) (0.5) BSE SENSEX 21,856.22 0.1 (0.3) 3.2 RUB 36.50 (0.0) 0.2 11.1 Bovespa 45,861.81 0.4 (0.8) (11.0) BRL 0.42 0.3 (0.7) 0.3 RTS 1,098.69 (2.9) (5.2) (23.8) 163.1 144.4 131.8