5 gst-bundled supply

•Download as PPTX, PDF•

1 like•63 views

Summarized overview of GST prepared on the basis of detailed study

Recommended

More Related Content

Recently uploaded

Recently uploaded (20)

Featured

Featured (20)

5 gst-bundled supply

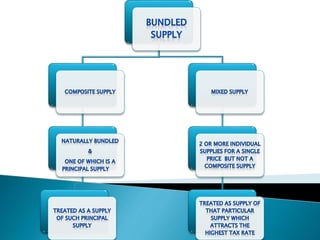

- 2. •Where goods are packed and transported with insurance, the supply of goods, packing. materials, transport and insurance is a composite supply and supply of goods is the principal supply. •The entire supply will be treated as supply of principal and the rate of tax of principal will apply for other items. 1. •In case of purchase of ticket in Rajdhani Train where the cost of ticket includes the services for Transportation of passengers, cost of foods and supply of bed rolls. All these services are bundled together and here the principal supply will be transportation of passengers. 2. •A luxury Hotel in Delhi provides a 3 Nights package with the breakfast and one day Delhi sightseeing. The inclusion of Delhi sightseeing in this package is not a natural requisite to accommodation in the hotel. Hence, this does not amount to composite supply. This is a mixed supply. 3.

- 3. •A supply of package consisting of canned foods, sweets, chocolates, cakes, dry fruits, and fruit juice when supplied for a single price. Here it is further assumed that canned food is taxable @ 12%, sweets at zero rate, chocolates @ 18%, cakes 18%, dry fruits 18%, and fruit juice @ 28%. •Here the Highest rate will be charged @ 28 % on entire value of supply. •If these items are supplied separately then it will not be a mixed supply. 4. •A combo pack for Rs 10,000 is supplied which consist of a Tie, Pen, Calculator, Wallet, Watch . The Tie is taxable say@ 10%, Pen @ 8%,Caculator12% ,Wallet 18% and Watch @ 28%. •Here the combo pack will be considered as Mixed supply and will be taxable at highest rate which is 28%. 5.