6 gst-e-way bill

•Download as PPTX, PDF•

0 likes•76 views

Summarized overview of GST prepared on the basis of detailed study

Recommended

More Related Content

Recently uploaded

Recently uploaded (20)

Featured

Featured (20)

6 gst-e-way bill

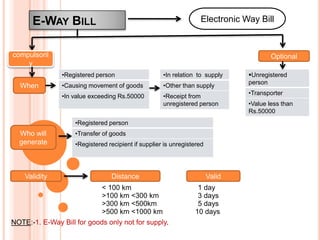

- 1. E-WAY BILL Electronic Way Bill compulsoril y When •Registered person •Causing movement of goods •In value exceeding Rs.50000 •In relation to supply •Other than supply •Receipt from unregistered person Optional Unregistered person •Transporter •Value less than Rs.50000 Who will generate •Registered person •Transfer of goods •Registered recipient if supplier is unregistered Validity Distance Valid < 100 km 1 day >100 km <300 km 3 days NOTE:-1. E-Way Bill for goods only not for supply. >300 km <500km 5 days >500 km <1000 km 10 days

- 2. E-WAY BILL GENERATION Who When Part Form Every Registered person under GST Before movement of goods Fill Part A Form GST INS-1 Registered person is consignor or consignee (mode of transport may be owned or hired) OR is recipient of goods Before movement of goods Fill Part B Form GST INS-1 Registered person is consignor or consignee and goods are handed over to transporter of goods Before movement of goods Fill Part A & Part B Form GST INS-1 Transporter of goods Before movement of goods Fill form GST INS- 1 if consignor does not. Unregistered person under GST and recipient is registered. Compliance to be done by Recipient as if he is the Supplier.