1. Fixed and Floating exchange rate

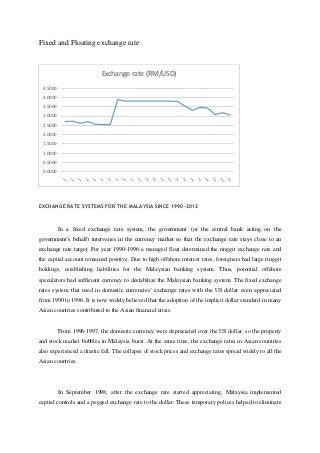

EXCHANGE RATE SYSTEMS FOR THE MALAYSIA SINCE 1990-2012

In a fixed exchange rate system, the government (or the central bank acting on the

government's behalf) intervenes in the currency market so that the exchange rate stays close to an

exchange rate target. For year 1990-1996 a managed float determined the ringgit exchange rate and

the capital account remained positive. Due to high offshore interest rates, foreigners had large ringgit

holdings, establishing liabilities for the Malaysian banking system. Thus, potential offshore

speculators had sufficient currency to destabilize the Malaysian banking system. The fixed exchange

rates system that used in domestic currencies’ exchange rates with the US dollar even appreciated

from 1990 to 1996. It is now widely believed that the adoption of the implicit dollar standard in many

Asian countries contributed to the Asian financial crisis.

From 1996-1997, the domestic currency were depreciated over the US dollar, so the property

and stock market bubbles in Malaysia burst. At the same time, the exchange rates in Asian countries

also experienced a drastic fall. The collapse of stock prices and exchange rates spread widely to all the

Asian countries.

In September 1998, after the exchange rate started appreciating, Malaysia implemented

capital controls and a pegged exchange rate to the dollar. These temporary polices helped to eliminate

0.0000

0.5000

1.0000

1.5000

2.0000

2.5000

3.0000

3.5000

4.0000

4.5000

Exchange rate (RM/USD)

2. transactions not related to trade and foreign direct investment, thus closing the offshore market,

suspending ringgit credit to foreigners and reducing outflows. Malaysia’s economy has remained

healthy and vibrant since moving to a pegged exchange rate system. The benefits of a fixed system

include highly effective fiscal policies, which can result in high domestic income and output with

fiscal expansion.

For the current practice the exchange rate, Malaysia is currently undergoing fiscal expansion

policies to help increase domestic income and hence spending. On July 21, 2005, Bank Negara

announced the end of the peg to the US dollar immediately after China's announcement of the end of

the currency Chinese peg to the U.S. dollar. According to Bank Negara, Malaysia allows the ringgit

to operate in a managed float against several major currencies. This has resulted in the value of the

ringgit rising closer to its perceived market value, although Bank Negara has intervened in financial

markets to maintain stability in the trading level of the ringgit Malaysia is continuing with its pegged

exchange rate, helping maintain stable interest rates and keeping inflation low.

Asian Financial Crisis 1997

The influence of financial crisis that occur in 1997 was started at Thai crisis in July 1997, and

Malaysia experienced serious devaluation of its currency. During the crisis, the market value of the

Malaysia ringgit had dropped to half of the pre-crisis level until January 1998. At the start of 1997,

the KLSE Composite index was above 1,200, the ringgit was trading above 2.50 to the dollar, and the

overnight rate was below 7%.

In July 1997, within days of the Thai baht devaluation, the Malaysian ringgit was "attacked"

by speculators. The overnight rate jumped from under 8% to over 40%.This led to rating downgrades

and a general sell off on the stock and currency markets. By end of 1997, ratings had fallen many

notches from investment grade to junk, the KLSE had lost more than 50% from above 1,200 to under

600, and the ringgit had lost 50% of its value, falling from above 2.50 to under 4.57 on (23 January

1998) to the dollar.

Malaysian moves involved fixing the local currency to the US dollar, stopping the overseas

trade in ringgit currency and other ringgit assets therefore making offshore use of the ringgit invalid,

restricting the amount of currency and investments that residents can take abroad, and imposed for

foreign portfolio funds, a minimum one-year "stay period" which since has been converted to an exit

3. tax. The decision to make ringgit held abroad invalid has also dried up sources of ringgit held abroad

that speculators borrow from to manipulate the ringgit, for example by "selling short."