1. 8/28/2009 Wealth Management Research

US pocket summary

A weekly overview of market performance and Wealth Management Research's outlook, investment strategy and forecasts.

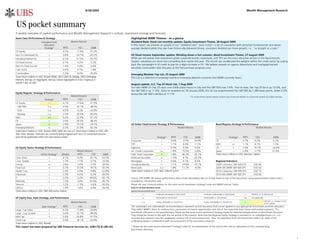

Asset Class Performance & Strategy Highlighted WMR Themes - at a glance

Extended Asset Market Returns Dividend Ruler Stock List monthly update, Equity Investment Theme, 28 August 2009

Allocation In this report, we provide an update of our "dividend ruler" stock screen—a list of companies with attractive fundamentals and above-

Strategy* MTD YTD 2008 average dividend yields that also have historically delivered strong, consistent dividend per share growth, i.e., "as straight as a ruler."

US Equity - 4.7% 17.6% -37.3%

Non-US Developed Eq. + 3.8% 24.7% -43.2% US fixed income September update: Winding down a hot summer, Bond Investment Theme, 27 August 2009

Emerging Market Eq. + 0.2% 51.9% -53.2% While we still believe that investment grade corporate bonds, municipals, and TIPS are the most attractive sectors of the fixed income

US Fixed Income -- 0.7% 4.2% 5.2% market, valuations are much less compelling than earlier this year. This month we recalibrated the weights within the credit sector by scaling

back the overweight in IG credit to pay for a slight increase in HY. We believe spreads on agency debentures and mortgage-backed

Non-US Fixed Income + 1.4% 5.4% 4.4%

securities could widen later this year as the Fed purchase programs end.

Cash (USD) - 0.0% 0.1% 1.8%

Commodities + 0.2% 8.2% -35.6% Emerging Markets Top List, 25 August 2009

Total return indices in USD: Russell 3000, MSCI EAFE & Canada, MSCI Emerging This List is a selection of sovereign bonds in Emerging Markets countries that WMR currently favors.

Markets, BarCap US Aggregate, BarCap Global Aggregate ex-USD, Citigroup 3-

month T-bill, DJ UBS

August update, U.S. Top 25 Stock List, 1 Aug 2009

The UBS WMR US Top 25 stock rose 6.8% (total return) in July and the S&P 500 rose 7.6%. Year to date, the Top 25 list is up 15.0%, and

the S&P 500 is up 11.0%. Since its inception on 18 January 2006, the list has outperformed the S&P 500 by 1,383 basis points, down 3.3%

Equity Regions' Strategy & Performance versus the S&P 500's decline of 17.1%.

Market Returns *To access these reports please contact your Financial Advisor or access the reports via online services

Strategy* MTD YTD 2008

US Equity --- 4.7% 17.6% -37.3%

S&P 500 n.a 4.4% 14.1% -38.5%

DJIA n.a 4.5% 9.2% -33.8%

Nasdaq n.a 2.5% 28.6% -40.5%

EMU ++ 6.0% 22.9% -47.1%

UK n 3.9% 28.3% -48.3%

Japan n 2.9% 10.2% -29.1% US Dollar Fixed Income Strategy & Performance Bond Regions Strategy & Performance

Emerging Markets ++ 0.2% 51.9% -53.2% Market Returns Market Returns

Total return indices in USD: Russell 3000, MSCI for non-US. Price return indices in USD: S&P

500, DJIA, Nasdaq. Forecasts are currently being aligned with new US investment process

and will be published within the next several weeks. Strategy* MTD YTD 2008 Strategy* MTD YTD 2008

Treasuries -- 0.6% -3.5% 14.0% US -- 0.7% 4.2% 5.2%

TIPS + 1.1% 6.0% -1.1% EMU ++ 1.1% 8.1% 1.0%

US Equity Sector Strategy & Performance Agencies - 0.3% 0.3% 9.6% UK n 1.6% 16.7% -24.6%

Market Returns Inv. Grade Corporates ++ 1.8% 15.5% -6.8% Japan -- 2.4% -2.7% 27.4%

Sector Strategy* Weekly MTD YTD 2008 High Yield Corporates + 1.8% 40.3% -26.1% Total return indices in USD: Barclays Capital .

Cons. Discr. + 3.1% 5.3% 25.1% -33.5% Preferred Securities n -1.5% 9.1% -25.2%

Cons. Staples + 1.3% 1.1% 5.7% -15.4% Mortgages n 0.4% 4.1% 8.3% Regional Indicators

Energy ++ 2.8% 3.0% 5.3% -34.9% Emerging Markets n 2.1% 19.4% -10.2% 2009 Consensus S&P 500 EPS USD 60

Financials n 3.2% 13.3% 19.1% -55.3% Municipals n.a 1.8% 11.2% -4.0% 2009 UBS WMR S&P 500 EPS USD 54

Health Care --- 2.0% 3.5% 9.8% -22.8% Total return indices in USD: BAS / Merrill Lynch 2010 Consensus S&P 500 EPS USD 75

Industrials + 3.3% 6.2% 9.2% -39.9% 2010 UBS WMR S&P 500 EPS USD 65

IT + 2.0% 3.2% 40.6% -43.1% Source: UBS WMR, All market performance data is from Bloomberg data as of date listed on top of this document, using representative indices and is

Materials + 1.5% 3.0% 32.9% -45.7% provided for information only.

Telecom - 2.2% -1.3% -0.4% -30.5% Please ask your Financial Advisor for the most recent Investment Strategy Guide and WMR Forecast Tables.

Utlities -- 1.4% 1.8% 4.0% -29.0% Scale for tactical deviation charts

Total return indices in USD: S&P 500 sector indices Symbol Description/Definition

+ moderate overweight vs. benchmark - moderate underweight vs. benchmark n Neutral, i.e. on benchmark

US Equity Size, Style Strategy, and Performance ++ overweight vs. benchmark -- underweight vs. benchmark n/a not applicable

Indicates +/- change in most

Market Returns +++ strong overweight vs. benchmark --- strong underweight vs. benchmark + -

recent update

Style Strategy* MTD YTD 2008 The overweight and underweight recommendations represent tactical deviations that can be applied to any appropriate benchmark portfolio allocation.

Large- Cap Value + 6.3% 11.8% -36.8% They reflect WMR’s short- to medium-term assessment of market opportunities and risks in the respective asset classes and market segments. The

Large - Cap Growth + 3.0% 23.1% -38.4% benchmark allocation is not specified here. Please see the most recent Investment Strategy Guide for definitions/explanations of benchmark allocation.

They should be chosen in line with the risk profile of the investor. Note that the Regional Equity Strategy is provided on an unhedged basis (i.e., it is

Mid-Cap n 5.9% 26.8% -41.5%

assumed that investors carry the underlying currency risk of such investments). Thus, the deviations from the benchmark reflect our views of the

Small-Cap - 5.0% 18.1% -33.8% underlying equity in combination with our assessment of the associated currencies.

Total return indices in USD: Russell

This report has been prepared by UBS Financial Services Inc. (UBS FS) & UBS AG * Please see the most recent Investment Strategy Guide for an interpretation of the tactical tilts and an explanation of the corresponding

benchmark allocation.

1

2. 8/28/2009 Wealth Management Research

US pocket summary

Currency Markets Performance & WMR Forecasts Central Bank Target Rates Overview and WMR Forecasts

Market Returns Forecast

2010

current MTD YTD 2008 in 3 m in 6 m in 12 m in % Current Aug Sept Oct Nov Dec Jan Feb Mar Apr May Jun Jul

USDCAD 1.0877 0.9% -10.8% 22.1% 1.08 1.05 1.00 Fed 0.25 0.25 0.25 0.25 0.25 0.25 0.25 0.25 0.25 0.25 0.25 0.25 0.25

EURUSD 1.4341 0.6% 2.6% -4.2% 1.45 1.50 1.57 ECB 1.00 1.00 1.00 1.00 1.00 1.00 1.00 1.00 1.00 1.00 1.00 1.00 1.00

GBPUSD 1.6284 -2.6% 11.6% -26.5% 1.67 1.72 1.77 BoE 0.50 0.50 0.50 0.50 0.50 0.50 0.50 0.50 0.50 0.50 0.50 0.50 0.50

USDCHF 1.0594 -0.9% -0.9% -5.7% 1.05 1.01 0.99 BoJ 0.10 0.10 0.10 0.10 0.10 0.10 0.10 0.10 0.10 0.10 0.10 0.10 0.10

USDSEK 7.1254 -0.9% -9.1% 21.1% 6.90 6.53 6.11 SNB 0.25 0.25 0.25 0.25 0.25 0.25 0.25 0.25 0.25 0.25 0.25 0.25 0.25

USDJPY 93.5200 -1.2% 3.2% -18.9% 97.00 100.00 105.00 BoC 0.25 0.25 0.25 0.25 0.25 0.25 0.25 0.25 0.25 0.25 0.25 0.25 0.25

AUDUSD 0.8392 0.4% 19.4% -19.7% 0.83 0.85 0.88 RBA 3.00 3.00 3.00 3.00 3.00 3.00 3.00 3.00 3.00 3.00 3.00 3.00 3.00

Please refer to most recent WMR Forecast Tables for further details.

Please refer to most recent WMR Forecast Tables for further details.

Commodities Performance & WMR Forecasts Interest Rate WMR Forecasts

Market Returns Forecast Short Rates Bond Yields

current MTD YTD 2008 1-3 m 9-12m (3m LIBOR) (10y gov)

WTI Crude (US$/bbl) 72.49 4.4% 62.5% -53.5% Sideways 85 in % current in 12m current in 12m

Nat. Gas (US$/mmbtu) 2.84 -22.2% -49.4% -24.9% Bullish 6.20 USA 0.36 0.30 3.45 4.25

Gold (US$/oz) 944.60 0.6% 9.1% 5.8% Bullish 1150 Canada 0.56 0.30 3.39 3.80

Aluminum (US$/mt) 1851.00 -0.9% 22.8% -36.1% Bearish 1800 EMU 0.80 1.00 3.25 4.00

Copper (US$/mt) 6257.50 9.4% 105.7% -54.2% Bullish 7000 UK 0.69 0.60 3.56 4.30

Silver (US$/oz) 14.22 4.3% 30.7% -23.0% Bullish 15.00 Switzerland 0.32 0.30 1.98 2.80

Corn (Usc/bushel) 323.00 -4.9% -20.6% -10.6% Bullish 480 Japan 0.39 0.30 1.31 1.80

Bullish = we target the upper range, Sideways = we expect a sideways move, Bearish = we Please refer to most recent WMR Forecast Tables for

target the lower range. Please refer to most recent WMR Forecast Tables for our short term further details.

and long term views for 3 months and 12 months, respectively.

Growth & Inflation WMR Forecasts Reports of Note Published in the Last Week - at a glance

GDP Growth Inflation US economics: Cyclical recovery at the doorstep, Economic Theme, 28 Aug 2009

(Real GDP % chg. yoy) (CPI; % change yoy) In this edition of our monthly US economic outlook, we reiterate the rough roadmap for recovery that we laid out last month and introduce our

in % 2008 2009F 2010F 2008 2009F 2010F detailed 2010 forecasts. We also test the hypothesis of a strong business fixed investment recovery despite a lackluster consumer recovery. In our

view, historically low capacity utilization and a lack of vigorous consumer demand speak strongly against a robust recovery in business investment.

World 3.2 -0.8 2.8 5.7 1.6 2.8

USA 0.4 -2.5 2.2 3.8 -0.7 1.8 As good as it gets, Investment Strategy Guide, 27 August 2009

Canada 0.7 -1.5 2.2 2.4 0.5 2.1 Equity markets have continued to move higher this month, buoyed by additional evidence that the global economy is on the path to recovery. We

EMU 0.7 -4.0 0.2 3.3 0.5 1.3 recommend holding a pro-cyclical portfolio tilt. This includes a preference for equities and commodities over fixed income and cash, a preference

Germany 1.3 -6.0 0.3 2.6 0.5 1.5 for cyclical over defensive equity sectors, and a preference for corporate bonds over other parts of the fixed in-come market.

France 0.7 -2.5 0.5 2.8 0.6 1.5

Italy -0.9 -4.0 -0.1 3.3 1.0 1.8 Equity markets: The case for having equities in portfolios, Market Update, 26 Aug 2009

Even after a huge rally, with shares rising more than 45% from their lows in March, there is still a case for including equities in a portfolio.

Spain 1.0 -3.7 -0.8 4.1 0.8 2.0

The case is built on a longer-term outlook rather than on any quick-win trading opportunities. The gains stemming from the relief that a

UK 0.7 -3.4 -0.2 3.6 0.7 1.4 full-fledged depression had been avoided are now mostly behind us. As more normal, cyclical patterns re-emerge, our valuation analysis

Switzerland 1.6 -2.8 -0.4 2.4 -0.4 0.6 still suggests that equities should offer good longer-term returns.

Japan -0.7 -6.0 1.5 1.4 -0.8 0.5

Asia ex Japan 6.0 3.0 6.1 6.2 0.3 2.6 Investing in volatile times, Part 3: Achieving financial goals in a changed world, UBS life themes, 26 Aug 2009

China 9.0 7.8 8.5 6.1 -1.2 1.6 Defining your goals is a vital first step to long-term investment success and peace of mind. The aftermath of the financial crisis will impact

Please refer to most recent WMR Forecast Tables for further details. the investment landscape in several ways, including probable changes to tax policies and pension programs. Your goals need to be defined

and structured in a comprehensive personal financial plan.

Financial crisis thermometers: Bi-weekly update, Economic Theme, 24 Aug 2009

In this report, we give our stance on where we stand in the current financial crisis by measuring financial, economic and credit health with

the help of "thermometers". The financial health thermometer for the US and Eurozone deteriorated mildly, while it improved for the UK

and stalled for Japan over the course of the last two weeks. The US credit health thermometer improved in July and now stands below its

level immediately preceding the collapse of Lehman Brothers last fall.

*To access these reports please contact your Financial Advisor or access the reports via online services 2