Download to read offline

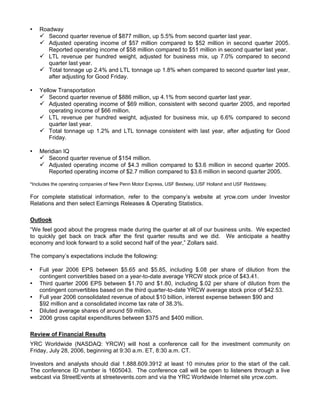

YRC Worldwide reported its highest ever quarterly earnings per share of $1.62 for Q2 2006, up 16% from $1.40 in Q2 2005. Revenue increased 23% to a record $2.57 billion due to strong execution and cost initiatives. Adjusted operating income rose 28% to $177 million from $138 million. The company expects full year 2006 EPS between $5.65-$5.85 and third quarter EPS between $1.70-$1.80.