The document provides an overview and introduction to the Foreign Contribution (Regulation) Act 1976 in India. Some key points:

- The Act regulates the acceptance and use of foreign contributions by certain individuals and organizations to ensure it does not compromise national security or elections.

- Organizations need prior permission or registration to receive foreign funds. Registered organizations must maintain separate accounts and submit annual audited reports.

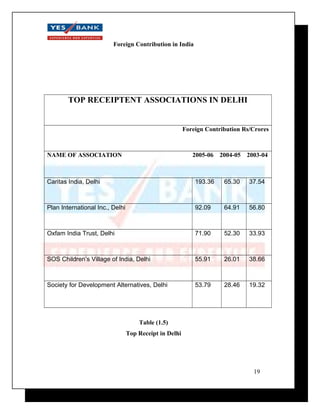

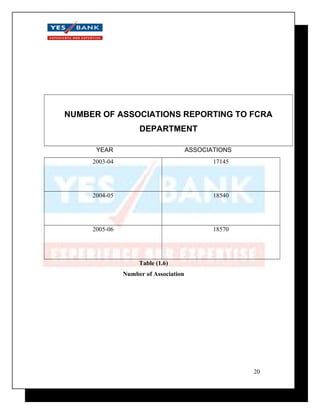

- Over 34,000 organizations are registered under the Act across religious, cultural, economic, educational and social categories. The top recipient states are Tamil Nadu, Delhi, and Andhra Pradesh.

- The Act also regulates foreign hospitality received by certain public officials and politicians to/from foreign countries.

![[DSC Europe 25] Nikola Vasiljevic - Player segmentation by combat playstyles ...](https://cdn.slidesharecdn.com/ss_thumbnails/mnvbf0yvrwaqsipzrrv3-2-nikola-vasiljevic-player-segmentation-by-playstyles-in-action-shooter-games-260114111931-b4d766cd-thumbnail.jpg?width=640&height=640&fit=bounds)

![[DSC Europe 25] Srba Markovic - From Pilot to Production: Overcoming AI Deplo...](https://cdn.slidesharecdn.com/ss_thumbnails/yjjmrtytmwbalxlba7px-4-srba-markovic-from-pilot-to-production-overcoming-ai-deployment-blockers-with-260114111931-4a892d44-thumbnail.jpg?width=640&height=640&fit=bounds)

![[DSC Europe 25] Stefan Brankovic - #ResumeIsDead. AI-Powered Interviews and C...](https://cdn.slidesharecdn.com/ss_thumbnails/qnmbsv0xq3uysdrq3sev-2-stefan-brankovic-job-bolt-260114111931-a065aa3d-thumbnail.jpg?width=640&height=640&fit=bounds)