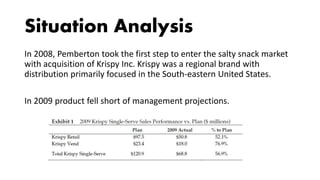

Pemberton Products is launching a relaunch of its Krispy Natural cracker brand. The document discusses the players involved, Pemberton's background in snacks, and the past performance of Krispy Natural. It then analyzes the US cracker market and details changes to the marketing strategy, including improvements to the product and expanded flavors. Test market results showed higher than expected market share gains and strong consumer willingness to buy. Pemberton plans to leverage these positive findings for a national rollout.