Download as PDF, PPTX

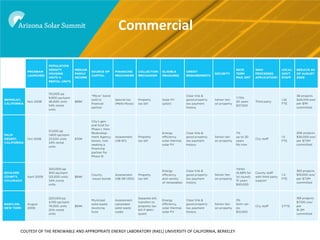

The Working Group 3 Policy & Finance group has 17 members representing utilities, solar industry, government, consultants, universities, and banking. The group discusses 15 different policies over 2 monthly calls and identified 3 main policies to focus on: 1) Residential solar readiness ordinance and financial mechanisms, 2) Commercial energy financing districts and concerns over superior liens, and 3) Utility-scale transmission initiatives and establishing renewable firm zones to inventory underused natural gas plants and pair them with solar generation.