The document provides an economic and market summary for the week of November 26th, 2012. Key points include:

- Global stock markets rebounded last week on hopes of a US fiscal cliff agreement. However, resolving the fiscal cliff remains uncertain.

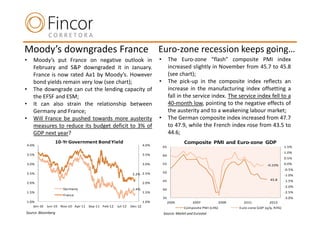

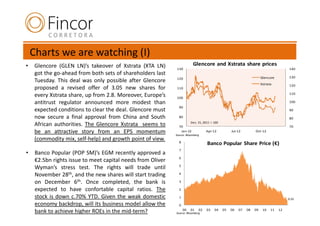

- In the eurozone, Moody's downgraded France's credit rating and further loan delays weighed on markets. Flash PMIs pointed to ongoing eurozone contraction in Q4.

- In Portugal, the sixth review found the bailout program on track, but unemployment and recession risks remain.

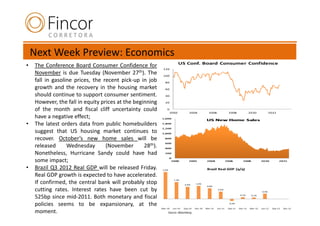

- US housing data continued to show recovery, while initial jobless claims fell. China's manufacturing PMI rose above 50, supporting steady recovery there.