Downloaded 185 times

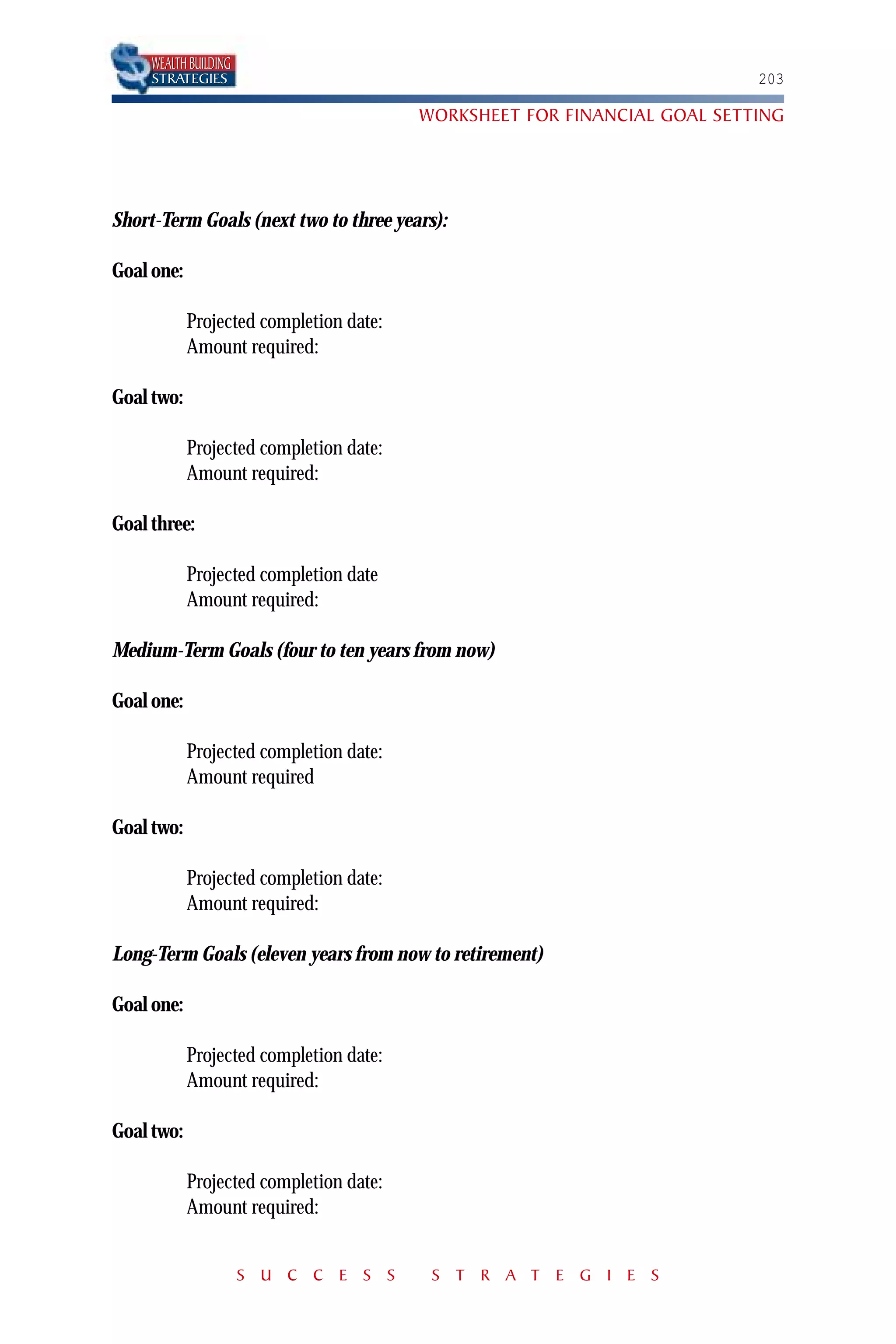

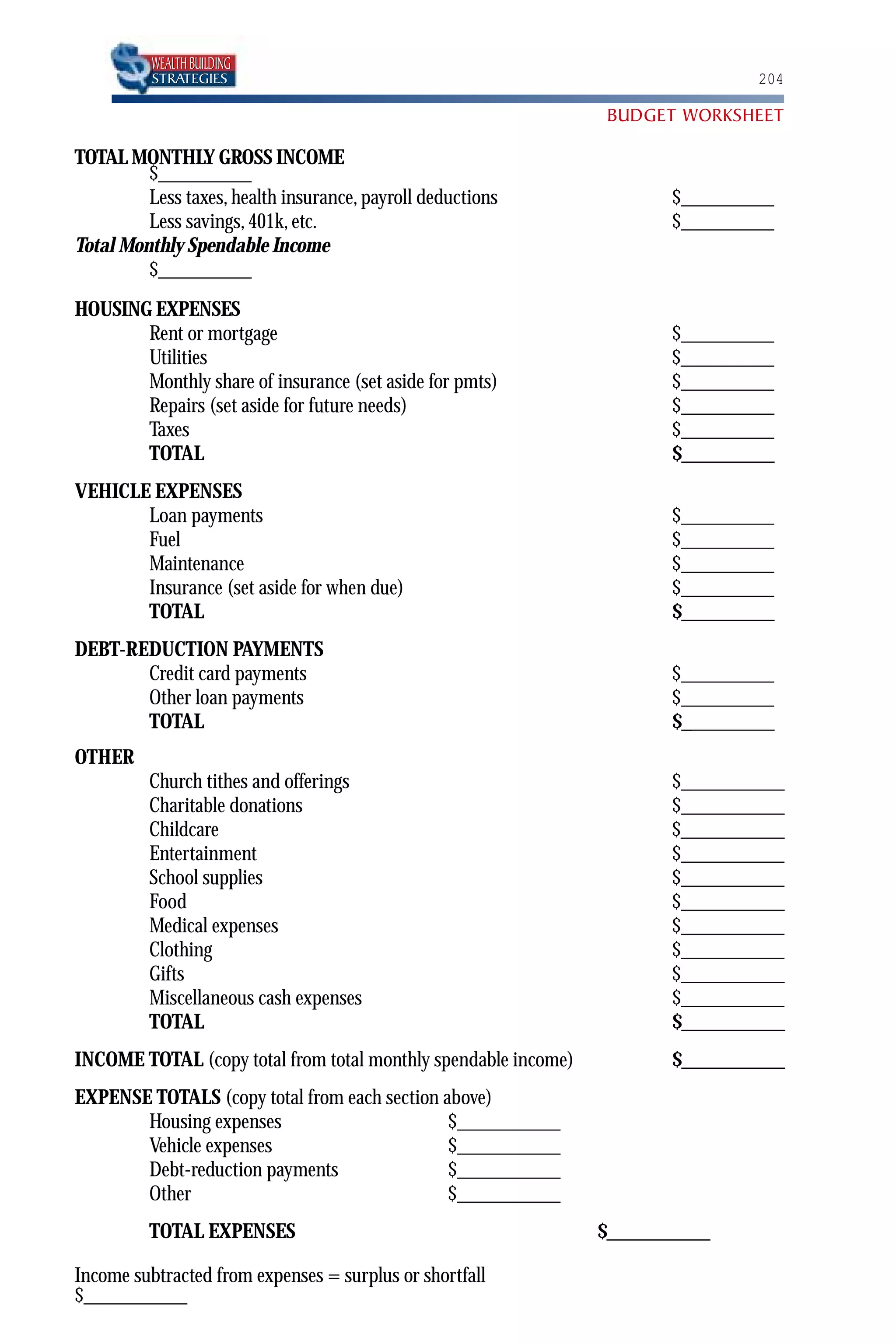

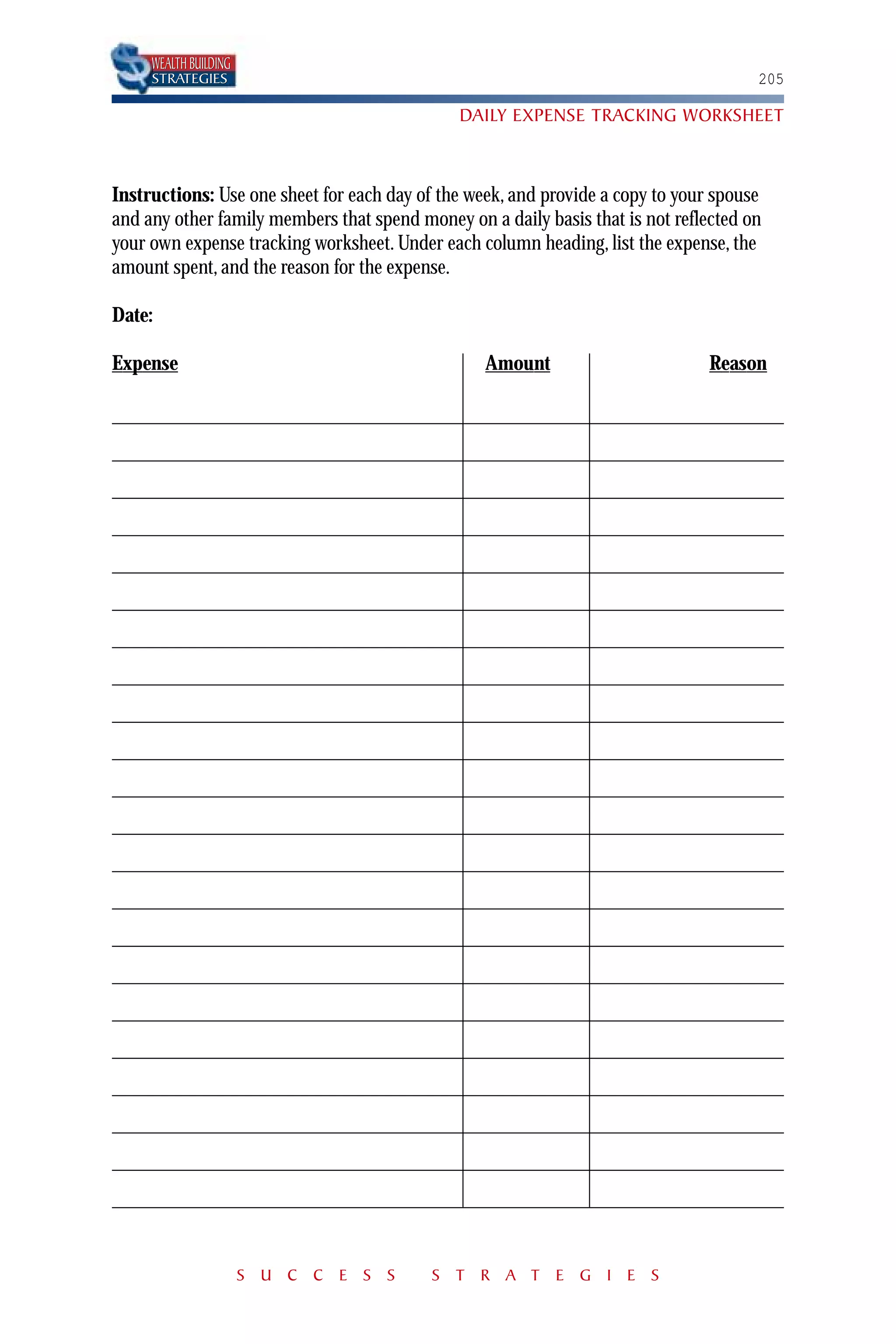

The document discusses the importance of setting financial goals, as goals provide a roadmap for building wealth over time. It notes that anyone can save money and invest, regardless of income, to work towards goals like financial security and retirement. Regular, disciplined savings and wise investments of even small amounts can significantly grow wealth over the long run.

![NOW i KNOW ! Cikaldana newsletter no. 02-2016 [on Ideal Retirement Fund Amount]](https://cdn.slidesharecdn.com/ss_thumbnails/nowiknow02-2016-160818100737-thumbnail.jpg?width=640&height=640&fit=bounds)

![Xlr8 presentation k_akers_aug 2011 v3 abridged [compatibility mode]](https://cdn.slidesharecdn.com/ss_thumbnails/xlr8presentationkakersaug2011v3abridgedcompatibilitymode-110822202149-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)