Download to read offline

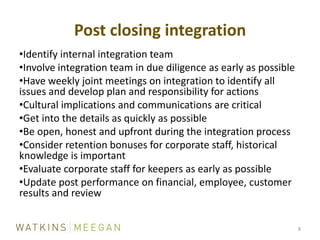

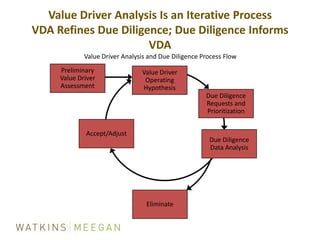

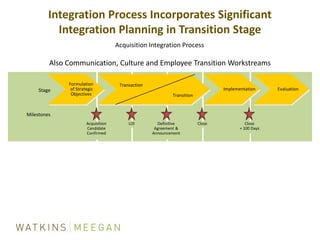

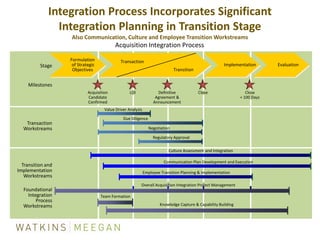

The document discusses CFO M&A strategies and experiences, including: - How ICF sourced deal opportunities through investment bankers and expanding contacts. - ICF's reliance on internal due diligence of contracts/backlog and external experts for accounting/legal/HR reviews. - ICF's M&A process of due diligence, negotiating deals to closing, and post-closing integration. - Key aspects of ICF's integration process including identifying teams, addressing culture/communication, and focusing on value drivers.