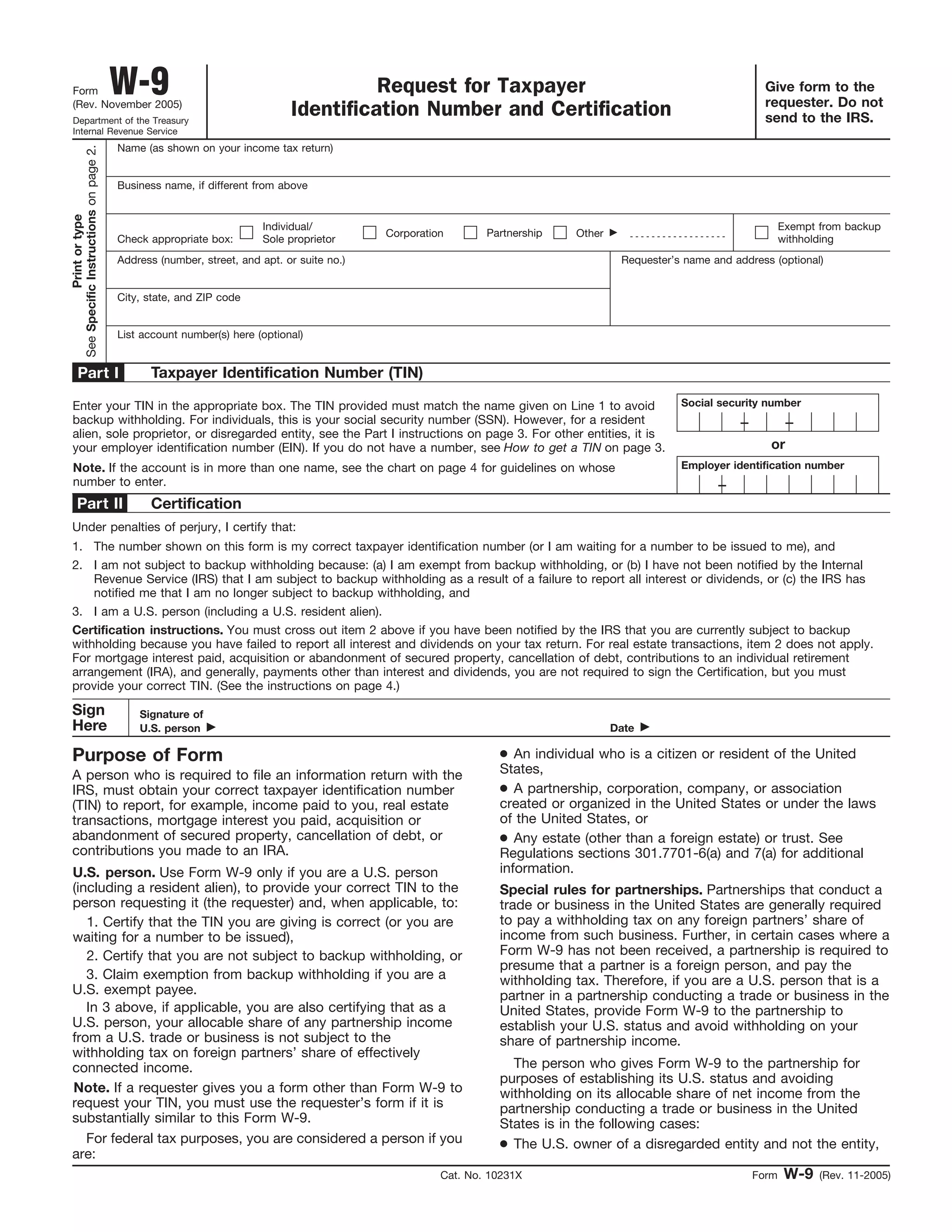

This document is an IRS Form W-9, which is used to request a taxpayer identification number from an individual or entity. It provides instructions on how to complete the form, including what information to provide in each section. The form is being completed by the Museum Store Association, Inc. to provide their taxpayer ID number to the requester for tax reporting purposes.