Vibrant India

•

0 likes•342 views

A general take on the Modi-phenomenon that has swept the stock markets! With structural changes finally being implemented by the new government we can expect a decade of massive growth. First uploaded as an Instablog on SeekingAlpha in September

Recommended

Recommended

More Related Content

What's hot

What's hot (20)

Viewers also liked

Viewers also liked (12)

Similar to Vibrant India

Similar to Vibrant India (20)

Recently uploaded

Recently uploaded (20)

Vibrant India

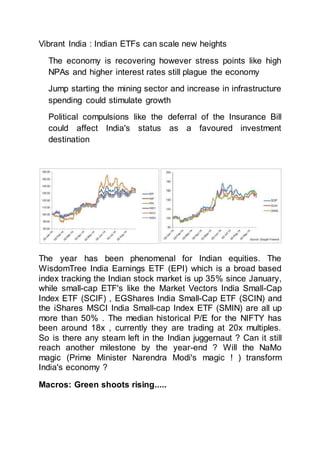

- 1. Vibrant India : Indian ETFs can scale new heights The economy is recovering however stress points like high NPAs and higher interest rates still plague the economy Jump starting the mining sector and increase in infrastructure spending could stimulate growth Political compulsions like the deferral of the Insurance Bill could affect India's status as a favoured investment destination The year has been phenomenal for Indian equities. The WisdomTree India Earnings ETF (EPI) which is a broad based index tracking the Indian stock market is up 35% since January, while small-cap ETF's like the Market Vectors India Small-Cap Index ETF (SCIF) , EGShares India Small-Cap ETF (SCIN) and the iShares MSCI India Small-cap Index ETF (SMIN) are all up more than 50% . The median historical P/E for the NIFTY has been around 18x , currently they are trading at 20x multiples. So is there any steam left in the Indian juggernaut ? Can it still reach another milestone by the year-end ? Will the NaMo magic (Prime Minister Narendra Modi's magic ! ) transform India's economy ? Macros: Green shoots rising.....

- 2. In the Union budget for FY2014-15 the finance minister Mr. Arun Jaitley, had estimated India's subsidy bill at $44bn or 2.03% of the gross domestic product. Oil subsidies account for 24% of the budget subsidy. This number was calculated assuming crude prices to be around $110 per bbl. However since then the Indian crude basket has fallen to $96.71/bbl (as on Sept 17,2014). If the drop in price sustains itself it will reduce oil under-recoveries thus improving the budget deficit Similarly despite fears of drought and a deficit in rainfall. The monsoon has been within normal limits for most parts of the country. In fact in September it has recorded one of the heaviest spells of this season, decreasing the overall monsoon deficit to 11%.

- 3. Agriculture accounts for 46% of the total employment in the country and a good monsoon augurs well for the sector and results in a domino feel-good effect on the economy. This feel-good effect is also evident in the quarterly consumer confidence survey conducted by the RBI. After years of being despondent the consumer finally feels optimistic about his future under the BJP government 135 125 115 105 95 85 75 Current Situation Index Future Expectation Index

- 4. But one of the leading sign of a recovering economy is the growth in commercial vehicles sales. Industry figures show that sales growth of CVs seem to have bottomed out. Potential red flags A big stress point in the economy is the rise in NPA's in the banking sector. A large chunk of NPA's are owned by public sector banks. Higher NPA's in PSU banks was historically due to their large exposure to the agri & priority sector. However the recent Supreme Court judgement for cancelling 214 coal block licenses is likely to add to their woes. Out of the 214 blocks only 46 blocks were active. The apex court has stipulated a fine of $4.86/ton of coal that was mined from these blocks. The State Bank of India, the largest PSU bank in India has a

- 5. $670mn exposure to the mining & power sector. Implications of the decision, will likely be felt by the companies that own the active blocks as well as by the banks that had provided them funding based on the coal allocations. Another risk to investments in India are high Interest rates. The RBI Governor will announce its bi-monthly review of monetary policies on Sept 30. Even though inflation seems to be under control, the RBI is unlikely to reduce interest rates till the fourth quarter of FY15. Another risk is the political opportunism which can block key reform initiatives by the new government. During the recent Parliamentary session the government was unable to clear the Insurance Bill. The bill was supposed to be one of the most important reform initiative by the new government. Though the government has a majority in the Lok Sabha, they do not have the requisite numbers in the Rajya Sabha. The Congress-led opposition blocked the Bill and it was referred to a Parliamentary Standing committee. It's ironic, because before the elections the Congress party was one of the staunchest supporters of the bill. But after losing the elections it started raising objarections to some amendments made by the BJP government. Such political compulsions could spoil the love affair that investors had with the new government! Investment outlook vs competing economies

- 6. S&P recently upgraded the sovereign credit outlook from 'negative' to 'stable'. The upgrade was based on the decisive mandate that Modi's government has received and on the expectations that they would be able to push for far reaching reforms which can put the country on a high growth trajectory. This reiterates what the fund managers have been doing for quite some time by investing in Indian stocks. So how does the Indian economy compare with its peers -viz. Brazil, China, Russia & South Africa ((BRIC's)) ? 3.00% 2.50% 2.00% 1.50% 1.00% 0.50% 0.00% -0.50% -1.00% Brazil China India Russia South Africa Brazil seems to be in a recession with two consecutive quarters of de-growth. While the Russian Federation continues to pander to its imperialistic ambitions as NATO imposes sanctions on the failing economy. Even though China has had higher growth rates, the Sanghai Composite has been underperforming the S&P NIFTY. Though the recent September Flash PMI was above 50, it seems likely that their years of high growth are over, and growth rates will fall to more sustainable levels.

- 7. 135.00 130.00 125.00 120.00 115.00 110.00 105.00 100.00 95.00 90.00 Sanghai Composite NIFTY In contrast the Indian economy is on the path to recovery. Also optimism regarding the new reform oriented government is very high. We can expect a period of consolidation in the stock market during the next few months before it resumes it move up.