MEANING OF VALUATION

Venture capital valuation is the process of

determining how much a startup is worth

when investors (like VCs) are deciding

whether to invest.

VCs consider market opportunity, team

expertise, product or service, traction,

competitive landscape, financial projections,

and risk factors when determining whether to

invest in a startup or not.

3.

The twomost common VCs use to determine the

value of a startup are the “Venture Capital”

method and the “Berkus” method.

VCs will conduct thorough research to verify any

estimations and assumptions made during the

valuation process.

This includes market research, customer

interviews, and financial audits to ensure

your startup’s claims are accurate and

achievable.

4.

Venture capitalvaluation is the process of

determining how much a startup is worth when

investors (like VCs) are deciding whether to

invest.

This can be both before and after the

investment (“pre-money” vs. “post-money”

valuation).

In short, it helps VCs decide how much equity

they should get in exchange for their investment.

5.

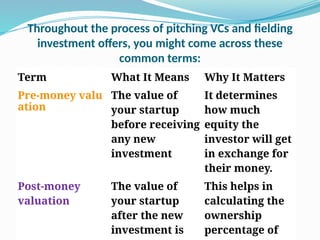

Throughout the processof pitching VCs and fielding

investment offers, you might come across these

common terms:

Term What It Means Why It Matters

Pre-money valu

ation

The value of

your startup

before receiving

any new

investment

It determines

how much

equity the

investor will get

in exchange for

their money.

Post-money

valuation

The value of

your startup

after the new

investment is

This helps in

calculating the

ownership

percentage of

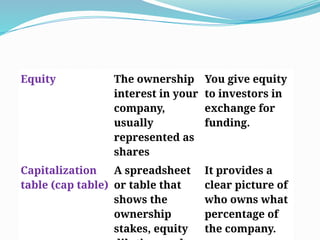

6.

Equity The ownership

interestin your

company,

usually

represented as

shares

You give equity

to investors in

exchange for

funding.

Capitalization

table (cap table)

A spreadsheet

or table that

shows the

ownership

stakes, equity

It provides a

clear picture of

who owns what

percentage of

the company.

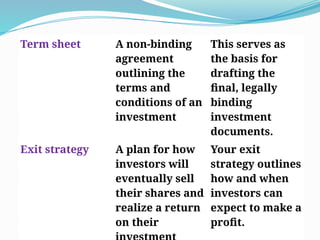

7.

Term sheet Anon-binding

agreement

outlining the

terms and

conditions of an

investment

This serves as

the basis for

drafting the

final, legally

binding

investment

documents.

Exit strategy A plan for how

investors will

eventually sell

their shares and

realize a return

on their

Your exit

strategy outlines

how and when

investors can

expect to make a

profit.

8.

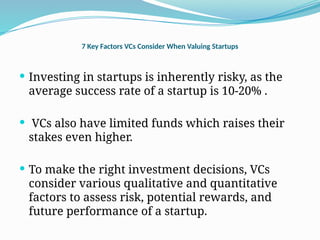

7 Key FactorsVCs Consider When Valuing Startups

Investing in startups is inherently risky, as the

average success rate of a startup is 10-20% .

VCs also have limited funds which raises their

stakes even higher.

To make the right investment decisions, VCs

consider various qualitative and quantitative

factors to assess risk, potential rewards, and

future performance of a startup.

9.

Common factors VCsconsider when determining the value of a startup (and

whether it’s worth investing or not):

Market Opportunity: The size and growth

potential of the target market. A larger, rapidly

growing market increases the startup’s potential

value.

Team Expertise: The skills, experience, and

track record of the founding team. A strong,

experienced team boosts investor confidence

and increases the startup’s value.

10.

Product orService: The uniqueness, quality,

and demand for the product or service. A highly

innovative or in-demand product can

significantly raise the startup’s value.

Traction and Performance: Metrics like user

growth, revenue, and customer retention.

Positive traction shows the startup’s potential for

success and increases its value.

11.

Competitive Landscape:The number and

strength of competitors. Less competition or a

strong competitive edge can enhance the

startup’s value.

Financial Projections: Future revenue, profit

potential, and scalability. Realistic, positive

financial projections can boost the startup’s

value.

12.

Risk Factors:Potential risks and how they are

mitigated. Lower risk levels generally increase

the startup’s value.

Based on these factors, VCs determine which

venture capital valuation method(s) are the

most appropriate to come to an accurate value.

13.

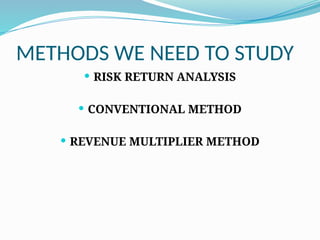

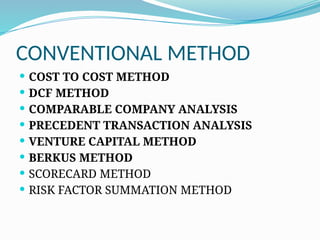

METHODS WE NEEDTO STUDY

RISK RETURN ANALYSIS

CONVENTIONAL METHOD

REVENUE MULTIPLIER METHOD

14.

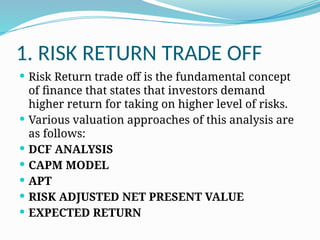

1. RISK RETURNTRADE OFF

Risk Return trade off is the fundamental concept

of finance that states that investors demand

higher return for taking on higher level of risks.

Various valuation approaches of this analysis are

as follows:

DCF ANALYSIS

CAPM MODEL

APT

RISK ADJUSTED NET PRESENT VALUE

EXPECTED RETURN

15.

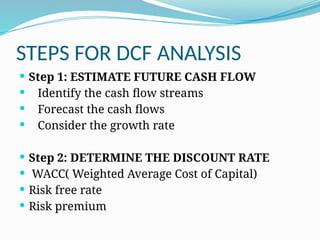

STEPS FOR DCFANALYSIS

Step 1: ESTIMATE FUTURE CASH FLOW

Identify the cash flow streams

Forecast the cash flows

Consider the growth rate

Step 2: DETERMINE THE DISCOUNT RATE

WACC( Weighted Average Cost of Capital)

Risk free rate

Risk premium

16.

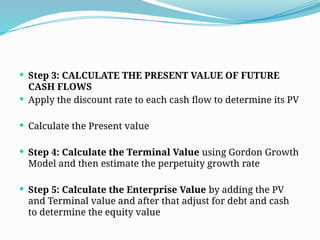

Step 3:CALCULATE THE PRESENT VALUE OF FUTURE

CASH FLOWS

Apply the discount rate to each cash flow to determine its PV

Calculate the Present value

Step 4: Calculate the Terminal Value using Gordon Growth

Model and then estimate the perpetuity growth rate

Step 5: Calculate the Enterprise Value by adding the PV

and Terminal value and after that adjust for debt and cash

to determine the equity value

17.

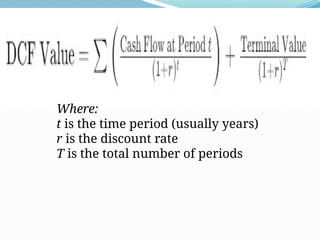

Where:

t is thetime period (usually years)

r is the discount rate

T is the total number of periods

18.

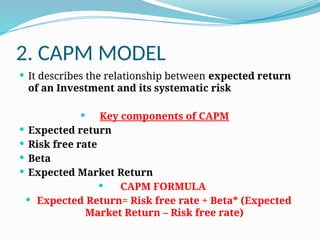

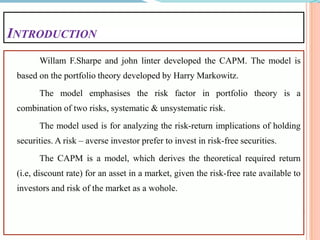

2. CAPM MODEL

It describes the relationship between expected return

of an Investment and its systematic risk

Key components of CAPM

Expected return

Risk free rate

Beta

Expected Market Return

CAPM FORMULA

Expected Return= Risk free rate + Beta* (Expected

Market Return – Risk free rate)

20.

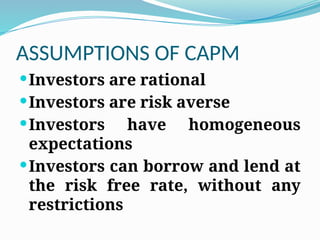

ASSUMPTIONS OF CAPM

Investorsare rational

Investors are risk averse

Investors have homogeneous

expectations

Investors can borrow and lend at

the risk free rate, without any

restrictions

21.

Markets areefficient

Investors have access to a risk free

asset

Investment horizon is infinite

No taxes on buying & selling of

securities

All Assets are tradable

Beta is the complete measure of risk

24.

assumptions

Arbitrage –Investors are free to buy and sell the

assets without any restrictions and there is NO

TRANSACTION COST.

Risk free Asset

Linear Relationship

32.

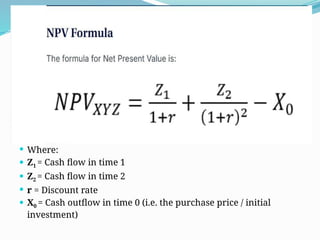

Net PresentValue (NPV) is the value of all future

cash flows (positive and negative) over the entire life

of an investment discounted to the present.

NPV analysis is a form of intrinsic valuation and is

used extensively across finance and accounting for

determining the value of a business, investment

security, capital project, new venture, cost reduction

program, and anything that involves cash flow.

33.

Where:

Z1= Cash flow in time 1

Z2 = Cash flow in time 2

r = Discount rate

X0 = Cash outflow in time 0 (i.e. the purchase price / initial

investment)

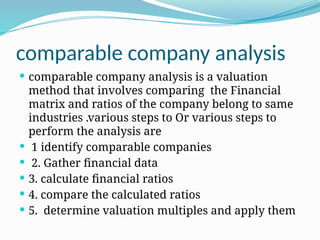

comparable company analysis

comparable company analysis is a valuation

method that involves comparing the Financial

matrix and ratios of the company belong to same

industries .various steps to Or various steps to

perform the analysis are

1 identify comparable companies

2. Gather financial data

3. calculate financial ratios

4. compare the calculated ratios

5. determine valuation multiples and apply them

36.

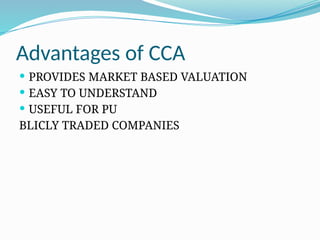

Advantages of CCA

PROVIDES MARKET BASED VALUATION

EASY TO UNDERSTAND

USEFUL FOR PU

BLICLY TRADED COMPANIES

37.

DISADVANTAGES

DIFFICULTY INFINDING COMPARABLE

COMPANIES

IGNORES COMPANY SPECIFIC FACTORS

SENSITIVE TO MARKET CONDITIONS