The document provides the key findings of a 2022 M&A Trends Survey conducted by Deloitte. Some of the main findings include:

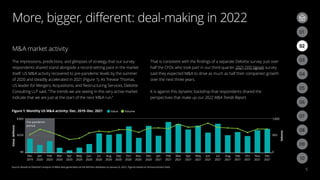

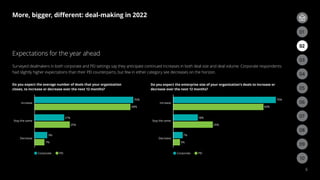

- 92% of respondents expect M&A deal volume to increase or stay the same over the next 12 months.

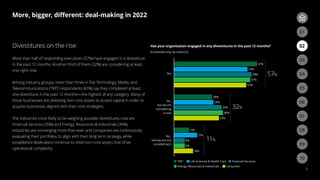

- 57% of corporate respondents engaged in a divestiture in the past year and 32% are considering one.

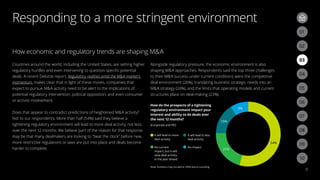

- 54% of respondents believe a tightening regulatory environment will lead to more M&A activity as dealmakers try to complete deals before new regulations.

- Alternative M&A strategies like partnerships and joint ventures are becoming more popular alongside traditional acquisitions and divestitures.