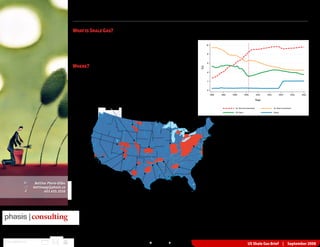

The document summarizes key shale gas plays in the United States and Canada. It identifies the major established shale gas basins in the US, including the Barnett shale in Texas, Woodford shale in Oklahoma, Fayetteville shale in Arkansas, Antrim shale in Michigan, and Devonian/Ohio shale along the Appalachian basin. It notes that while Canada has large shale gas potential, commercial production has not been achieved. The document provides details on the thickness, depth, gas content, production and major players for several US and Canadian shale gas plays.

Fortunate Sun Mining Company Ltd. is a mineral exploration company based in Vancouver BC, Canada, and listed on the TSX Venture Exchange (TSX-V). The company is engaged in the acquisition and exploration of Precious Metals projects with a primary focus on Mexico. Our aim is to create wealth for our shareholders in the Precious Metals Sector by identifying high quality exploration/ development projects that possess world class potential.

Petrichor Energy (TSX.V - PTP) Corporate PresentationViral Network Inc

Petrichor Energy Inc. is an emerging oil and gas exploration company focused on acquiring, exploring and developing new oil and natural gas reserves in North and South America. The company has been developing its current properties, located in the southern United States, for the past three years.

Petrichor Energy is growing its operations by implementing two primary objectives. The first is exploiting the potential of its low risk oil and gas fields in Texas and Mississippi. The second is to find new and highly prospective exploration projects in both North and South America — and to develop them into commercially feasible operations. By applying the latest geophysical and geological technologies when selectively drilling new wells, the company expects to increase its success ratio, as well as reduce the risk typically associated with oil and gas exploration.

Fortunate Sun Mining Company Ltd. is a mineral exploration company based in Vancouver BC, Canada, and listed on the TSX Venture Exchange (TSX-V). The company is engaged in the acquisition and exploration of Precious Metals projects with a primary focus on Mexico. Our aim is to create wealth for our shareholders in the Precious Metals Sector by identifying high quality exploration/ development projects that possess world class potential.

Petrichor Energy (TSX.V - PTP) Corporate PresentationViral Network Inc

Petrichor Energy Inc. is an emerging oil and gas exploration company focused on acquiring, exploring and developing new oil and natural gas reserves in North and South America. The company has been developing its current properties, located in the southern United States, for the past three years.

Petrichor Energy is growing its operations by implementing two primary objectives. The first is exploiting the potential of its low risk oil and gas fields in Texas and Mississippi. The second is to find new and highly prospective exploration projects in both North and South America — and to develop them into commercially feasible operations. By applying the latest geophysical and geological technologies when selectively drilling new wells, the company expects to increase its success ratio, as well as reduce the risk typically associated with oil and gas exploration.

US Natural Gas Situation as of June 2016Bruce LaCour

Natural gas price is beginning to increase and the switch from coal to gas for electricity production as well as the LNG export movement will place increased upward pressure on the natural gas price.

Shale gas is natural gas i.e. trapped within Shale. For to extract it we have use some extraction techniques like Horizontal Drilling or Hydraulic Fracking.

ACC - Shale Gas and New U.S. Chemical Industry Investment: $164 Billion and C...Marcellus Drilling News

The slide deck used by the American Chemistry Council at a Hudson Institute event held on April 6. The slide deck shares data from a recently updated study from the ACC showing current and planned projects related to shale gas and gas liquids is $164 billion. The American manufacturing scene is being transformed by the shale energy revolution.

Opening Global Markets to Booming U.S. Shale Gas and NGL ProductionICF

ICF International experts join an industry expert from Vinson and Elkins, LLP to discuss the boom in shale gas and natural gas liquids (NGL) production.

Key topics covered include:

• Marketing issues created by the boost in production

• Outlook for gas supply development

• Regulatory and contractual considerations that shape infrastructure development investments

US Natural Gas Situation as of June 2016Bruce LaCour

Natural gas price is beginning to increase and the switch from coal to gas for electricity production as well as the LNG export movement will place increased upward pressure on the natural gas price.

Shale gas is natural gas i.e. trapped within Shale. For to extract it we have use some extraction techniques like Horizontal Drilling or Hydraulic Fracking.

ACC - Shale Gas and New U.S. Chemical Industry Investment: $164 Billion and C...Marcellus Drilling News

The slide deck used by the American Chemistry Council at a Hudson Institute event held on April 6. The slide deck shares data from a recently updated study from the ACC showing current and planned projects related to shale gas and gas liquids is $164 billion. The American manufacturing scene is being transformed by the shale energy revolution.

Opening Global Markets to Booming U.S. Shale Gas and NGL ProductionICF

ICF International experts join an industry expert from Vinson and Elkins, LLP to discuss the boom in shale gas and natural gas liquids (NGL) production.

Key topics covered include:

• Marketing issues created by the boost in production

• Outlook for gas supply development

• Regulatory and contractual considerations that shape infrastructure development investments

A webinar slide presentation from Williams detailing their Northeast Supply Enhancement pipeline project--a Transco pipeline project that will increase capacity and flows heading into northeastern markets. In particular, Transco wants to provide more natural gas to utility giant National Grid beginning with the 2019-2020 heating season.

Putting the SPARK into Virtual Training.pptxCynthia Clay

This 60-minute webinar, sponsored by Adobe, was delivered for the Training Mag Network. It explored the five elements of SPARK: Storytelling, Purpose, Action, Relationships, and Kudos. Knowing how to tell a well-structured story is key to building long-term memory. Stating a clear purpose that doesn't take away from the discovery learning process is critical. Ensuring that people move from theory to practical application is imperative. Creating strong social learning is the key to commitment and engagement. Validating and affirming participants' comments is the way to create a positive learning environment.

RMD24 | Retail media: hoe zet je dit in als je geen AH of Unilever bent? Heid...BBPMedia1

Grote partijen zijn al een tijdje onderweg met retail media. Ondertussen worden in dit domein ook de kansen zichtbaar voor andere spelers in de markt. Maar met die kansen ontstaan ook vragen: Zelf retail media worden of erop adverteren? In welke fase van de funnel past het en hoe integreer je het in een mediaplan? Wat is nu precies het verschil met marketplaces en Programmatic ads? In dit half uur beslechten we de dilemma's en krijg je antwoorden op wanneer het voor jou tijd is om de volgende stap te zetten.

Buy Verified PayPal Account | Buy Google 5 Star Reviewsusawebmarket

Buy Verified PayPal Account

Looking to buy verified PayPal accounts? Discover 7 expert tips for safely purchasing a verified PayPal account in 2024. Ensure security and reliability for your transactions.

PayPal Services Features-

🟢 Email Access

🟢 Bank Added

🟢 Card Verified

🟢 Full SSN Provided

🟢 Phone Number Access

🟢 Driving License Copy

🟢 Fasted Delivery

Client Satisfaction is Our First priority. Our services is very appropriate to buy. We assume that the first-rate way to purchase our offerings is to order on the website. If you have any worry in our cooperation usually You can order us on Skype or Telegram.

24/7 Hours Reply/Please Contact

usawebmarketEmail: support@usawebmarket.com

Skype: usawebmarket

Telegram: @usawebmarket

WhatsApp: +1(218) 203-5951

USA WEB MARKET is the Best Verified PayPal, Payoneer, Cash App, Skrill, Neteller, Stripe Account and SEO, SMM Service provider.100%Satisfection granted.100% replacement Granted.

Kseniya Leshchenko: Shared development support service model as the way to ma...Lviv Startup Club

Kseniya Leshchenko: Shared development support service model as the way to make small projects with small budgets profitable for the company (UA)

Kyiv PMDay 2024 Summer

Website – www.pmday.org

Youtube – https://www.youtube.com/startuplviv

FB – https://www.facebook.com/pmdayconference

Tata Group Dials Taiwan for Its Chipmaking Ambition in Gujarat’s DholeraAvirahi City Dholera

The Tata Group, a titan of Indian industry, is making waves with its advanced talks with Taiwanese chipmakers Powerchip Semiconductor Manufacturing Corporation (PSMC) and UMC Group. The goal? Establishing a cutting-edge semiconductor fabrication unit (fab) in Dholera, Gujarat. This isn’t just any project; it’s a potential game changer for India’s chipmaking aspirations and a boon for investors seeking promising residential projects in dholera sir.

Visit : https://www.avirahi.com/blog/tata-group-dials-taiwan-for-its-chipmaking-ambition-in-gujarats-dholera/

VAT Registration Outlined In UAE: Benefits and Requirementsuae taxgpt

Vat Registration is a legal obligation for businesses meeting the threshold requirement, helping companies avoid fines and ramifications. Contact now!

https://viralsocialtrends.com/vat-registration-outlined-in-uae/

Unveiling the Secrets How Does Generative AI Work.pdfSam H

At its core, generative artificial intelligence relies on the concept of generative models, which serve as engines that churn out entirely new data resembling their training data. It is like a sculptor who has studied so many forms found in nature and then uses this knowledge to create sculptures from his imagination that have never been seen before anywhere else. If taken to cyberspace, gans work almost the same way.

Premium MEAN Stack Development Solutions for Modern BusinessesSynapseIndia

Stay ahead of the curve with our premium MEAN Stack Development Solutions. Our expert developers utilize MongoDB, Express.js, AngularJS, and Node.js to create modern and responsive web applications. Trust us for cutting-edge solutions that drive your business growth and success.

Know more: https://www.synapseindia.com/technology/mean-stack-development-company.html

Business Valuation Principles for EntrepreneursBen Wann

This insightful presentation is designed to equip entrepreneurs with the essential knowledge and tools needed to accurately value their businesses. Understanding business valuation is crucial for making informed decisions, whether you're seeking investment, planning to sell, or simply want to gauge your company's worth.

Attending a job Interview for B1 and B2 Englsih learnersErika906060

It is a sample of an interview for a business english class for pre-intermediate and intermediate english students with emphasis on the speking ability.

Enterprise Excellence is Inclusive Excellence.pdfKaiNexus

Enterprise excellence and inclusive excellence are closely linked, and real-world challenges have shown that both are essential to the success of any organization. To achieve enterprise excellence, organizations must focus on improving their operations and processes while creating an inclusive environment that engages everyone. In this interactive session, the facilitator will highlight commonly established business practices and how they limit our ability to engage everyone every day. More importantly, though, participants will likely gain increased awareness of what we can do differently to maximize enterprise excellence through deliberate inclusion.

What is Enterprise Excellence?

Enterprise Excellence is a holistic approach that's aimed at achieving world-class performance across all aspects of the organization.

What might I learn?

A way to engage all in creating Inclusive Excellence. Lessons from the US military and their parallels to the story of Harry Potter. How belt systems and CI teams can destroy inclusive practices. How leadership language invites people to the party. There are three things leaders can do to engage everyone every day: maximizing psychological safety to create environments where folks learn, contribute, and challenge the status quo.

Who might benefit? Anyone and everyone leading folks from the shop floor to top floor.

Dr. William Harvey is a seasoned Operations Leader with extensive experience in chemical processing, manufacturing, and operations management. At Michelman, he currently oversees multiple sites, leading teams in strategic planning and coaching/practicing continuous improvement. William is set to start his eighth year of teaching at the University of Cincinnati where he teaches marketing, finance, and management. William holds various certifications in change management, quality, leadership, operational excellence, team building, and DiSC, among others.

What are the main advantages of using HR recruiter services.pdfHumanResourceDimensi1

HR recruiter services offer top talents to companies according to their specific needs. They handle all recruitment tasks from job posting to onboarding and help companies concentrate on their business growth. With their expertise and years of experience, they streamline the hiring process and save time and resources for the company.

Discover the innovative and creative projects that highlight my journey throu...dylandmeas

Discover the innovative and creative projects that highlight my journey through Full Sail University. Below, you’ll find a collection of my work showcasing my skills and expertise in digital marketing, event planning, and media production.

"𝑩𝑬𝑮𝑼𝑵 𝑾𝑰𝑻𝑯 𝑻𝑱 𝑰𝑺 𝑯𝑨𝑳𝑭 𝑫𝑶𝑵𝑬"

𝐓𝐉 𝐂𝐨𝐦𝐬 (𝐓𝐉 𝐂𝐨𝐦𝐦𝐮𝐧𝐢𝐜𝐚𝐭𝐢𝐨𝐧𝐬) is a professional event agency that includes experts in the event-organizing market in Vietnam, Korea, and ASEAN countries. We provide unlimited types of events from Music concerts, Fan meetings, and Culture festivals to Corporate events, Internal company events, Golf tournaments, MICE events, and Exhibitions.

𝐓𝐉 𝐂𝐨𝐦𝐬 provides unlimited package services including such as Event organizing, Event planning, Event production, Manpower, PR marketing, Design 2D/3D, VIP protocols, Interpreter agency, etc.

Sports events - Golf competitions/billiards competitions/company sports events: dynamic and challenging

⭐ 𝐅𝐞𝐚𝐭𝐮𝐫𝐞𝐝 𝐩𝐫𝐨𝐣𝐞𝐜𝐭𝐬:

➢ 2024 BAEKHYUN [Lonsdaleite] IN HO CHI MINH

➢ SUPER JUNIOR-L.S.S. THE SHOW : Th3ee Guys in HO CHI MINH

➢FreenBecky 1st Fan Meeting in Vietnam

➢CHILDREN ART EXHIBITION 2024: BEYOND BARRIERS

➢ WOW K-Music Festival 2023

➢ Winner [CROSS] Tour in HCM

➢ Super Show 9 in HCM with Super Junior

➢ HCMC - Gyeongsangbuk-do Culture and Tourism Festival

➢ Korean Vietnam Partnership - Fair with LG

➢ Korean President visits Samsung Electronics R&D Center

➢ Vietnam Food Expo with Lotte Wellfood

"𝐄𝐯𝐞𝐫𝐲 𝐞𝐯𝐞𝐧𝐭 𝐢𝐬 𝐚 𝐬𝐭𝐨𝐫𝐲, 𝐚 𝐬𝐩𝐞𝐜𝐢𝐚𝐥 𝐣𝐨𝐮𝐫𝐧𝐞𝐲. 𝐖𝐞 𝐚𝐥𝐰𝐚𝐲𝐬 𝐛𝐞𝐥𝐢𝐞𝐯𝐞 𝐭𝐡𝐚𝐭 𝐬𝐡𝐨𝐫𝐭𝐥𝐲 𝐲𝐨𝐮 𝐰𝐢𝐥𝐥 𝐛𝐞 𝐚 𝐩𝐚𝐫𝐭 𝐨𝐟 𝐨𝐮𝐫 𝐬𝐭𝐨𝐫𝐢𝐞𝐬."

2. sedimentary rocks do exist in abundance (Siberia, Australia, 2. Woodford Building upon the success of the Barnett, producers

Northern Africa to name a few), there simply isn’t enough knowledge applied similar approaches to the relatively new Woodford Shale in

to evaluate potential opportunities, nor do technologies exist to tap Oklahoma. Whereas due to its immense development and number of

into this growing unconventional gas supply source. Furthermore, large-scale players there is an abundance of data on the Barnett shale

because the technical challenges to make a shale play commercial play, very little is known about Woodford and estimates of its potentials

are quite substantial, successful development will be dependent on are still being evaluated. It must be acknowledged that some producers

involving those players with the most experience. have obtained some promising initial results.

Thickness (ft) 120-260

Typical Type Horizontal

Depth (ft) 6,000-11,000

Gas Content (scf/t) 60-115

Gas in Place (Bcf/s) 40-120

Reserve (EUR - Tcf) 1.0CHECK

Mean Daily 2.3

Production (Bcf/d)

Key Players DVN, NFX, CHK, CLR

The Basins Drilling & Completion

(Million $)

2.6-3.5

Well Spacing (Acres) 80

1. Barnett The Barnett is the most prolific and active shale gas

play in the US. The play encompasses approximately 5,000 square miles,

and is located between Dallas and Fort Worth, Texas. It is estimated

that production activity in the Barnett Shale may well continue for

yet other 20 to 30 years. However, further development will be limited

by the highly urbanized nature of this area. As well, securing land is 3. Fayetteville The Fayetteville Shale is an unconventional play within

becoming more and more difficult especially for new entrants to this play. the Arkoma Basin, which covers a vast area in North Western Arkansas.

Compared to other shale plays throughout the US, the Fayetteville Shale

Thickness (ft) 50-100 is still an exploratory play.

Typical Type Horizontal

Thickness (ft) 50-325

Depth (ft) 6,500-8,500

Typical Type Horizontal

Gas Content (scf/t) 300-350

Depth (ft) 1,500-6,500

Gas in Place (Bcf/s) 30-40

Gas Content (scf/t) 60-220

Reserve (EUR - Tcf) 26.2-39

Gas in Place (Bcf/s) 55-65

Mean Daily 1.2-2.5

Production (Bcf/d) Reserve (EUR - Tcf) 6

Key Players DVN, XTO, COP, EOG, ECA, CHK, DNR, Mean Daily 1.4-3.5

KWK, CRZO, MRO, PLLL, RDS-B, Chief Production (Bcf/d)

Oil & Gas, RRC, Edge Resources

Key Players SWN, CHK, XTO, MCF, EPEX, MVOG

Drilling & Completion 2.6-2.8

(Million $) Drilling & Completion 2.5-3.5

(Million $)

Well Spacing (Acres) 80-160

Well Spacing (Acres) 80

www.phasis.ca 2 US Shale Gas Brief | September 2008

4. Ticker Company

6. Lewis

AOG Aurora Oil & Gas 8. Haynesville The Haynesville Shale is the most recent addition to the

Thickness (ft) 200-300

APC Anadarko Petroleum

US Shale plays. It is roughly located between North Louisiana, East Texas

Typical Type - and South Western Arkansas. Being such a new play, details on this play

ATN Atlas Energy Depth (ft) 3,000-6,000 are still scarce. Its potential upsides are its geographical proximity to

BP BP Gas Content (scf/t) 15-45 areas of high expertise and large resources in a play that is thought to be

CHK Chesapeake Gas in Place (Bcf/s) 8-50

many times larger than the Barnett and with higher gas in place. Though

the Haynesville is not yet commercial, with most wells -horizontal and

CLR Continental Resources Reserve (EUR - Tcf) 10.7 vertical- being tested for, it is thought to be nearing commerciability

COG Cabot Oil & Gas Mean Daily - with very promising initial production rates. On the downside, is the

Production (Bcf/d)

COP ConocoPhillips consideration-still speculative at this point- that physical characteristics

CRK Comstock Resources

Key Players BP, CLR, APC of the shale may yield poorer decline rates then the Barnett or other plays.

Drilling & Completion 0.4-0.7

CRZO Carrizo Oil & Gas (Million $)

Thickness (ft) 100-300

DNR Denbury Resources Well Spacing (Acres) 80-320

Typical Type Likely Horizontal

DTE DTE Energy Co.

Depth (ft) 11,500

DVN Devon Energy

Gas Content (scf/t) N/A

ECA EnCana

Gas in Place (Bcf/s) N/A (Expected to be higher then Barnett)

EOG EOG Resources

Reserve (EUR - Tcf) N/A

EP El Paso 7. Marcellus Similar to the Devonian/Ohio Shale, the Marcellus Shale

Mean Daily Test Wells Only

is part of the vast Appalachian basin and shares many characteristics Production (Bcf/d)

EPEX Edge Petroleum

with the other plays in this basin (i.e. Devonian/Ohio). The Marcellus

EQT Equitable Resources Key Players CHK, GDP, CRK, HK, COG, FST, XCO, EP

Shale formation runs along a 600 miles stretch between the states of

FST Forest Oil Pennsylvania, West Virginia and New York. There has been a revived Drilling & Completion 5-8

(Million $)

GDP Goodrich Petroleum interest in the Marcellus Shale in the last ten months, mostly as a result of

very promising production. Much like the Devonian/Ohio, while limited Well Spacing (Acres) 60

HK Petrohawk Energy

resources hinders speed, low transportation costs and the vicinity of the

KWK Quicksilver Resources highly populated East Coast market are an attractive aspect of this play.

MCF Contango Oil & Gas

MRO Marathon Oil Thickness (ft) 150

MVOG Maverick Oil and Gas Typical Type Horizontal

NFX Newfield Exploration Depth (ft) 7,000-10,000

PLLL Parallel Petroleum Gas Content (scf/t) 100Mcf/af

RDS-B Shell Gas in Place (Bcf/s) -

RRC Range Resources Reserve (EUR - Tcf) 50

SWN Southwestern Mean Daily 1-3.5 MMcf/d

Production (Bcf/d)

WLL Whiting Petroleum Key Players RRC, EOG, CHK, APC, XCO, EQT, COG,

XCO EXCO Resouces SWN, ATN ,Chief Oil & Gas LLC, East

Resources Inc., Fortuna Energy Inc.

XTO XTO Energy

Drilling & Completion 1.2-2.5

- Chief Oil & Gas (Million $)

- East Resources Well Spacing (Acres) 80

- Fortuna Energy

www.phasis.ca 4 US Shale Gas Brief | September 2008

5. Impact of Technology on Shale Gas

In general, Shale Gas is a classical example where technology and

efficient processes make a huge impact on returns, more so then

in other conventional and unconventional plays. The adoption of

horizontal drilling, especially in the profilic Barnett Shale, is crucial

to maximizing profits from a well. But not all shale plays are the

same: producers quickly realized that understanding the geological

characteristics of the play is key to applying the right technology.

Technology advances in fracturing and horizontal drilling were

crucial in making Shale Gas a developable unconventional resource.

Fracturing Hydraulic fracturing is necessary in order to stimulate

the shale and allow the gas to be extracted. While fracturing is not

new to the industry, the way it is employed in the Shale play (multi-

stage) is somewhat different.

Horizontal Drilling Drilling horizontally is crucial in many Shale

gas plays, because it allows more gas to be extracted in less time. While

the costs of drilling horizontally are usually two to three times higher

then its vertical counterpart, the economics are often improved.

Techonology is key to successfully developing Shale gas plays, as well

applying the most efficient techniques to make a difference. Producers

and service companies, especially those with the largest access to capital

and infrastructure, must keep innvoating in order to both improve

production and succesfully apply their knowledge to new plays.

www.phasis.ca 5 US Shale Gas Brief | September 2008