Download to read offline

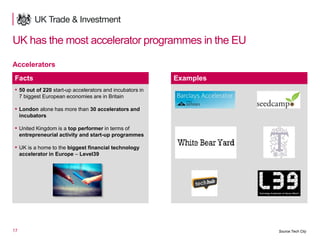

The document summarizes opportunities in the UK ICT sector landscape. It notes that the UK has a large ICT sector turnover estimated at £190 billion annually. It also has strong clusters for technology in several cities like London, Cambridge, Manchester, and Bristol. The UK has a large market for big data, cloud computing, software and IT services. It provides funding opportunities for startups and SMEs through programs like Innovate UK and has a strong venture capital environment and many business incubators and accelerators compared to other European countries.

![601.озорные наигрыши [ноты]](https://cdn.slidesharecdn.com/ss_thumbnails/601-150606081046-lva1-app6892-thumbnail.jpg?width=640&height=640&fit=bounds)