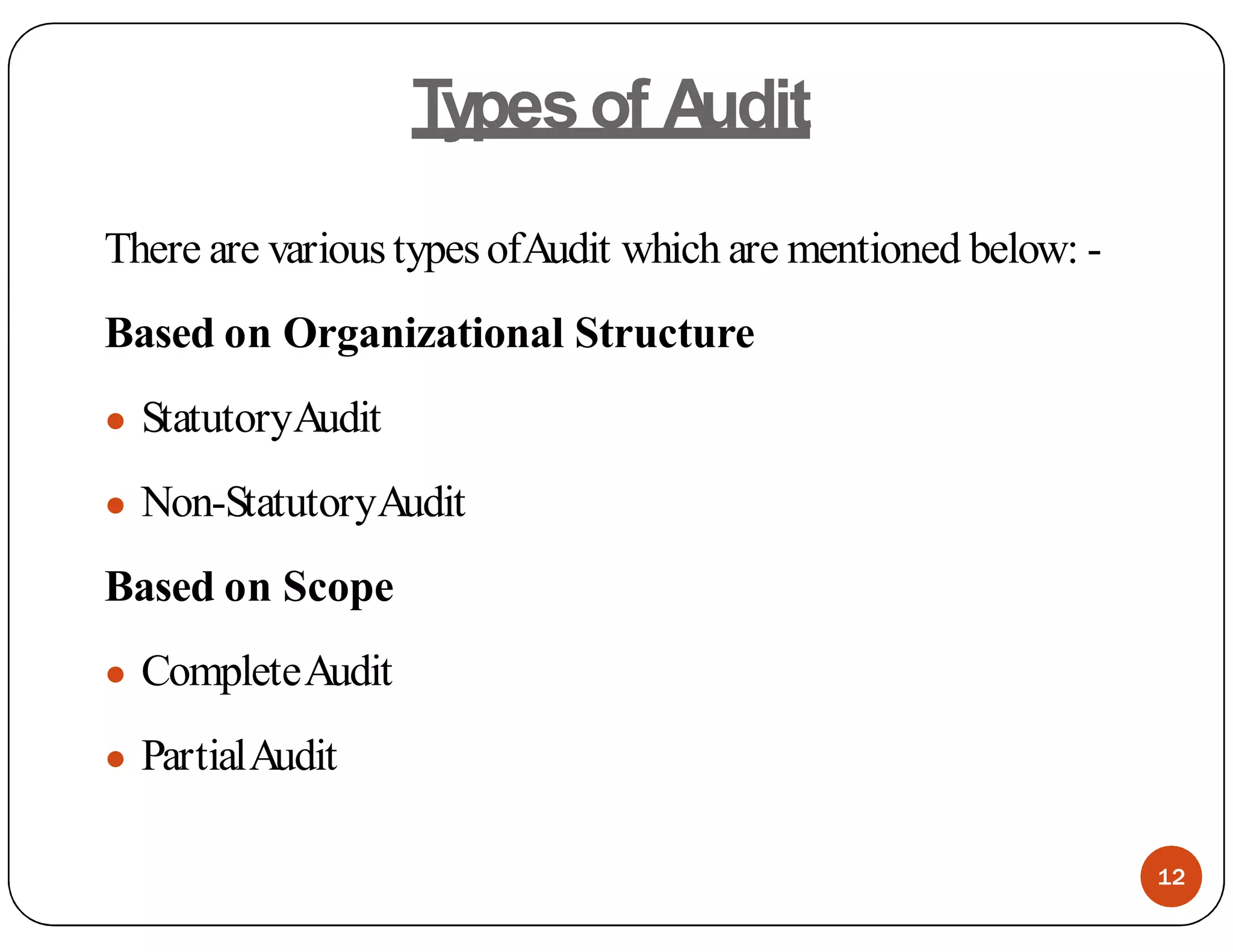

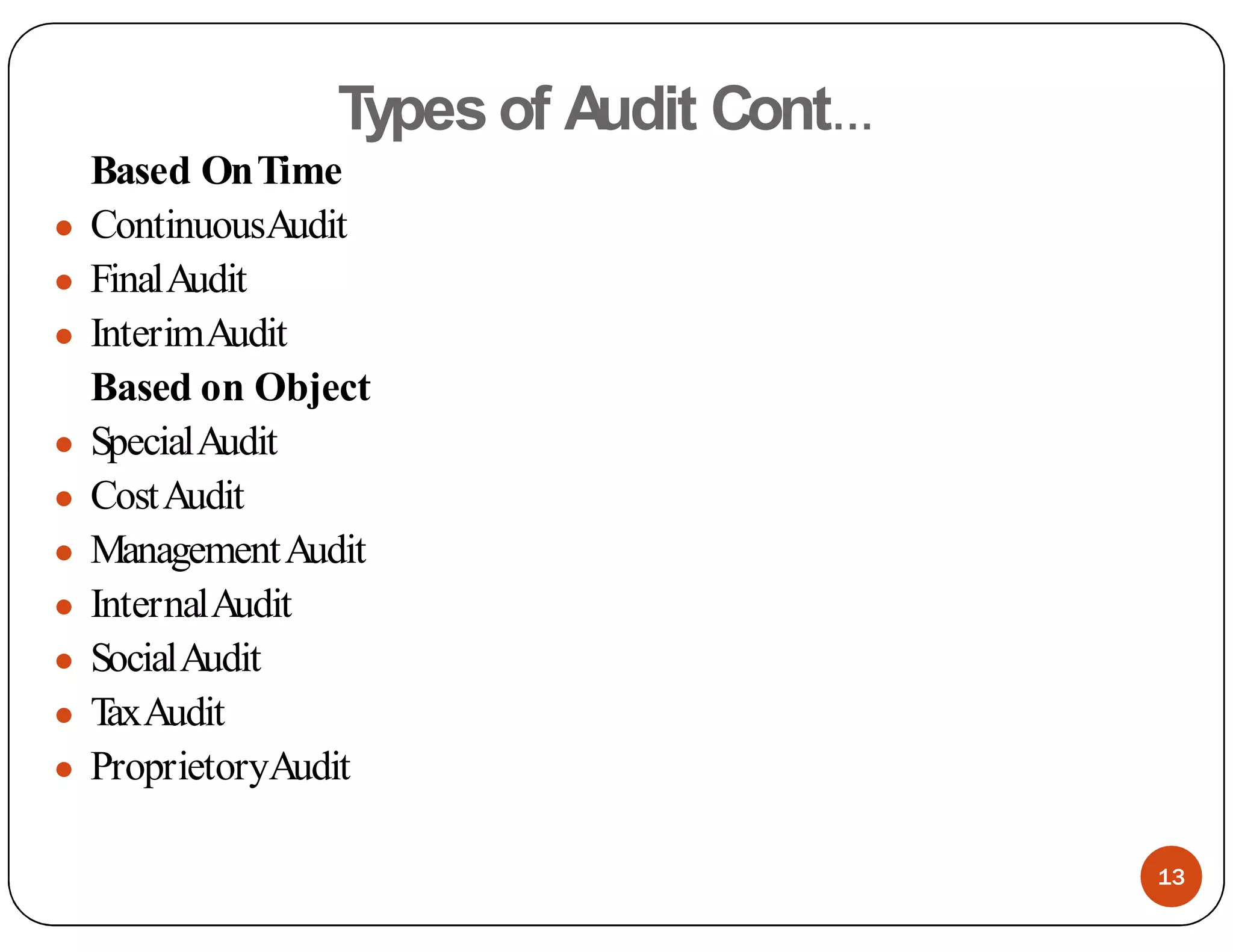

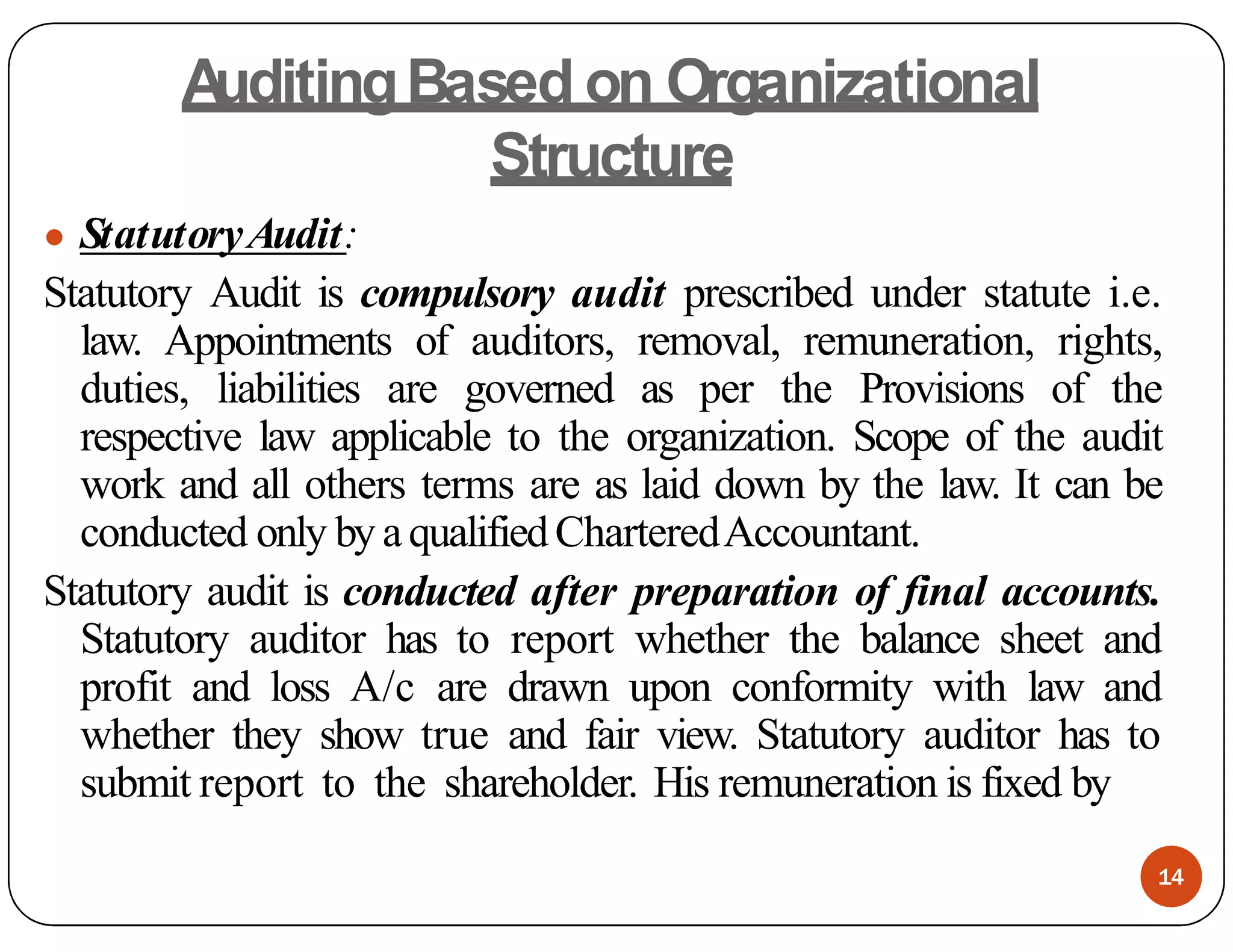

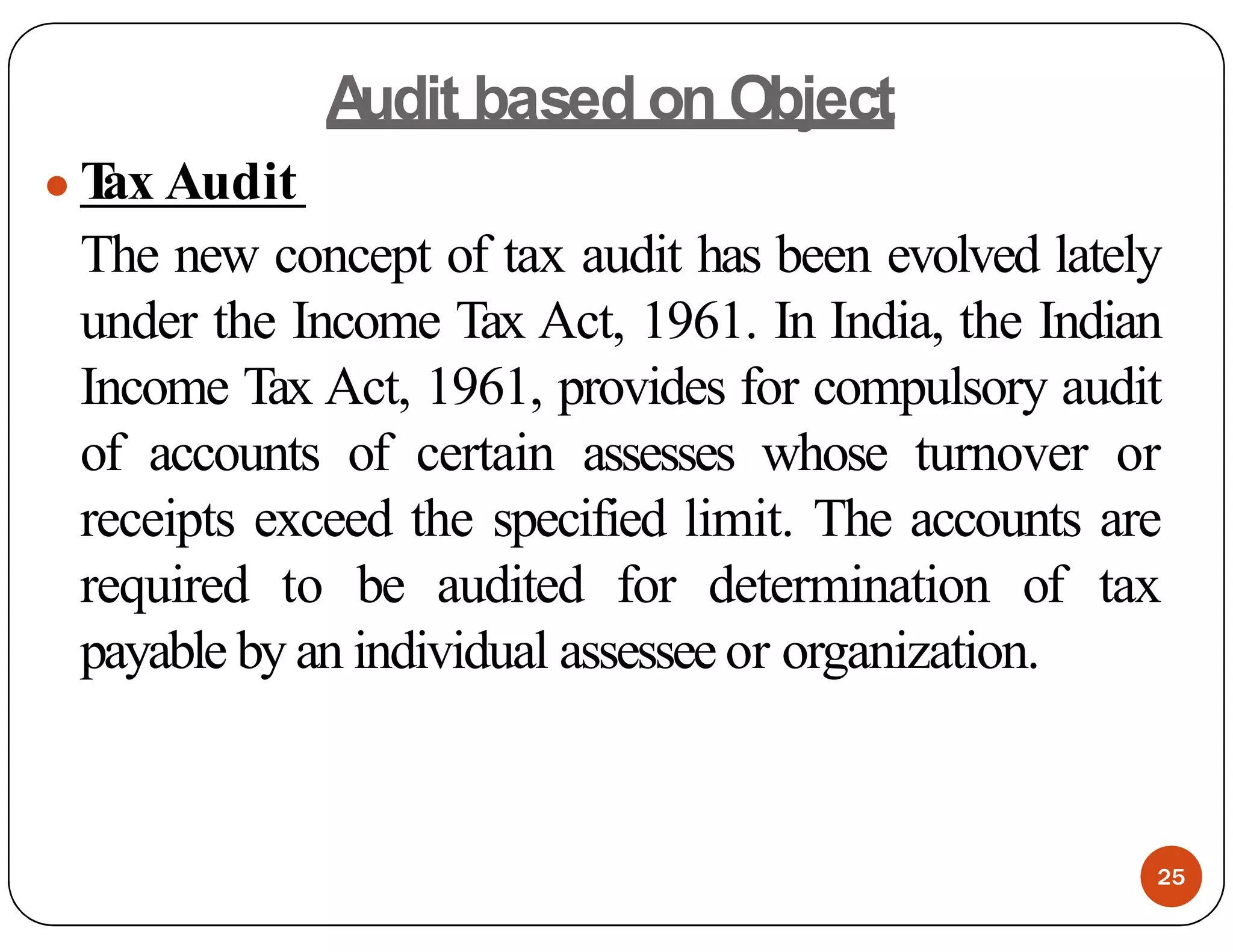

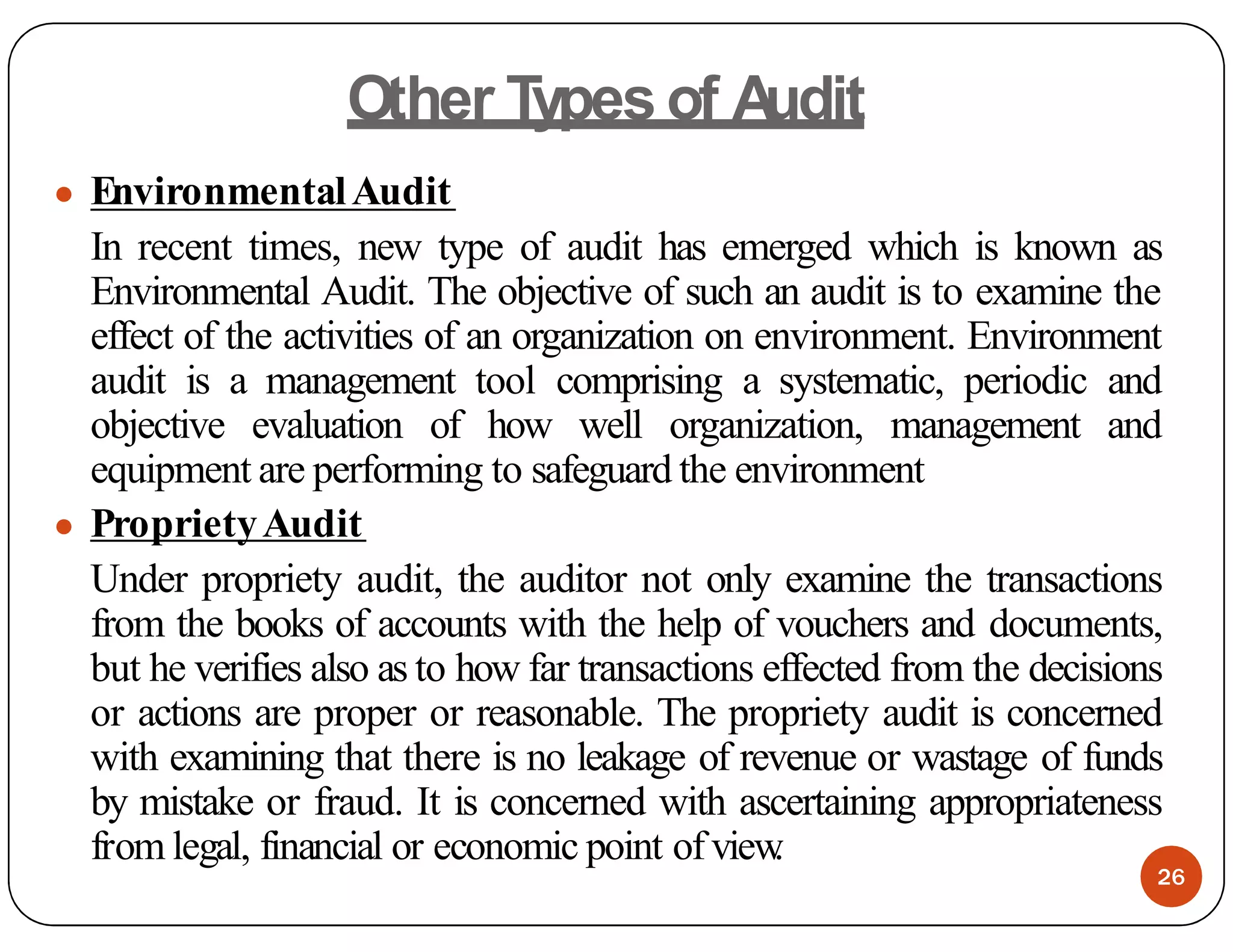

The document outlines various types of audits categorized by different criteria such as organizational structure, scope, time, and objective. Key types include statutory and non-statutory audits, complete and partial audits, as well as specialized audits like cost, management, and social audits. Each type serves distinct purposes, ranging from compliance with laws to evaluating organizational effectiveness and social responsibility.