UNIT - I

*Introduction– definition of audit – objects of

audit – classification of audit – Internal audit –

Periodical audit – Continuous audit – Interim

audit – Balance sheet audit- Internal check –

Internal control. Procedure of audit – audit

programme – test check – Auditing vs.

Investigation.

3.

*AUDITING -MEANING

*The wordAudit is derived from Latin word “Audire”

which means ‘to hear’. Auditing is the verification of

financial position as disclosed by the financial

statements.

*According to AAS-1 “An audit is an independent

examination of financial information, of any entity,

whether profit oriented or not, and irrespective of its

size or legal form, when such an examination is

conducted with a view to, expressing an opinion

thereon.

4.

*AUDITING -DEFINITION

*“Auditing isan examination of accounting records

undertaken with a view to establishment whether they

correctly and completely reflect the transactions to which

they purport to relate.”-L.R.Dicksee

*“Auditing is the systematic examination of financial

statements, records and related operations to determine

adherence to generally accepted accounting principles,

management policies and stated requirement.” -

R.E.Schlosser

5.

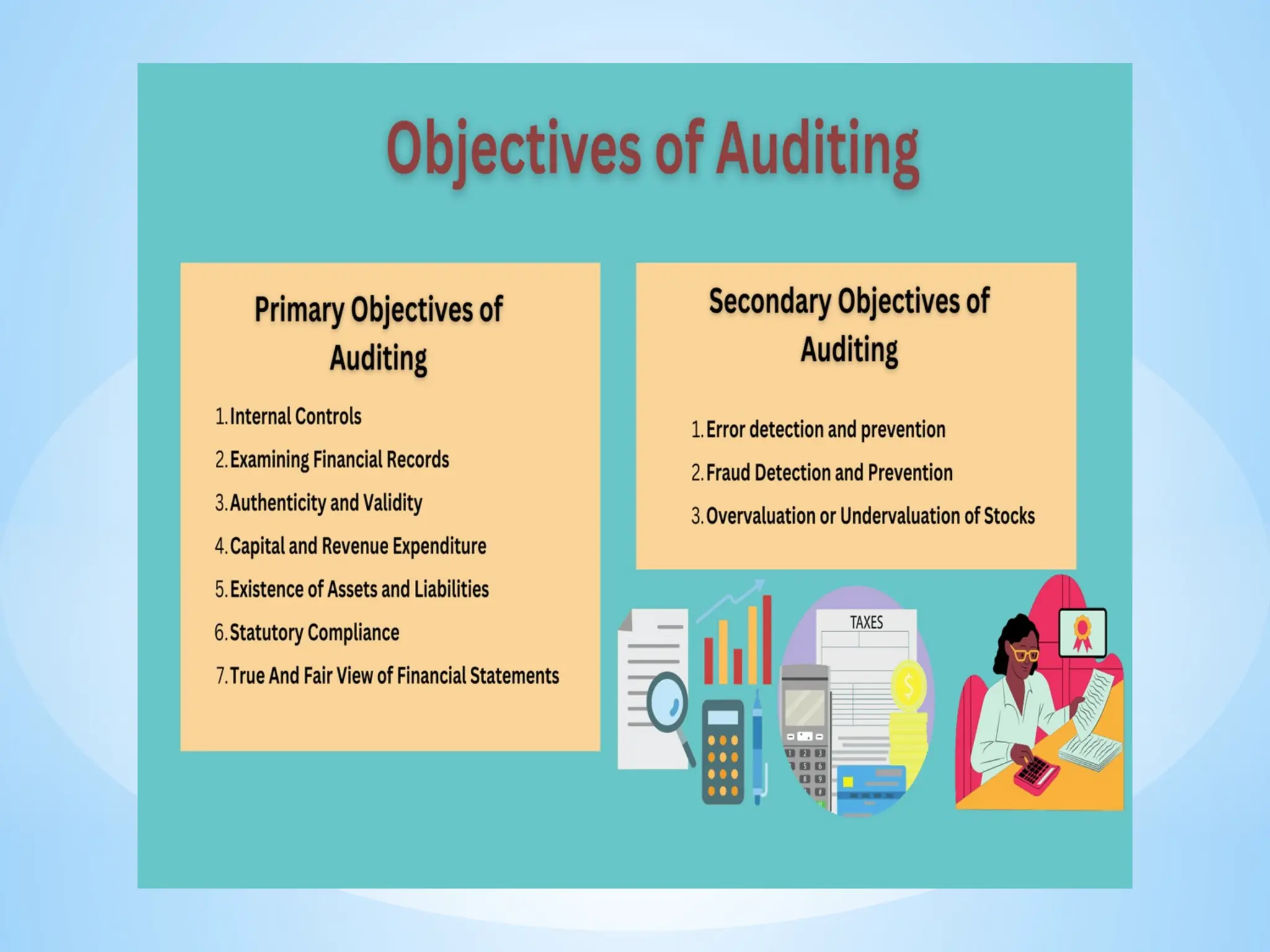

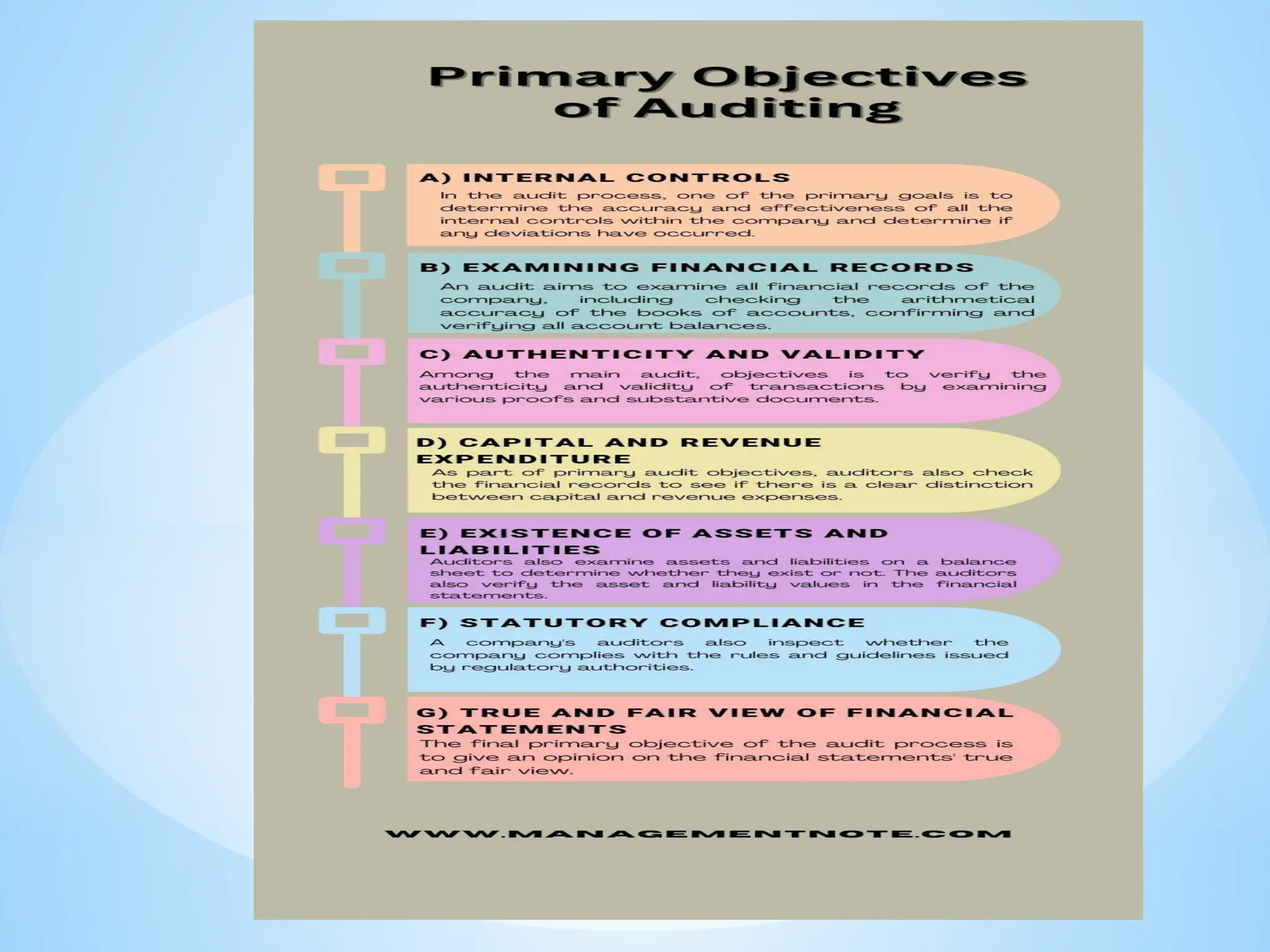

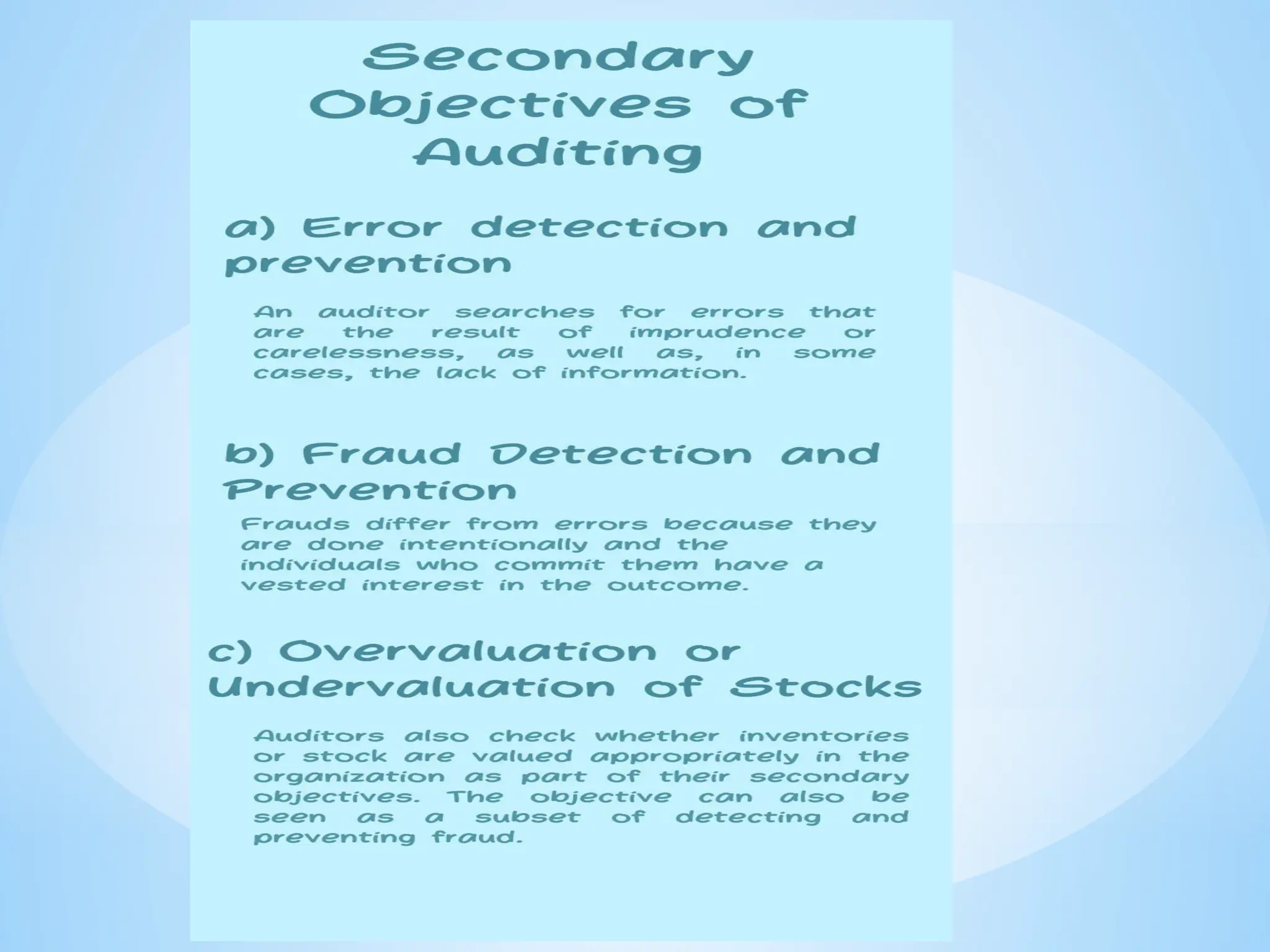

*Objectives of Auditing

*Theobjectives of the auditing have been

classified under two heads:

1.Primary objectives

2.Secondary objectives

9.

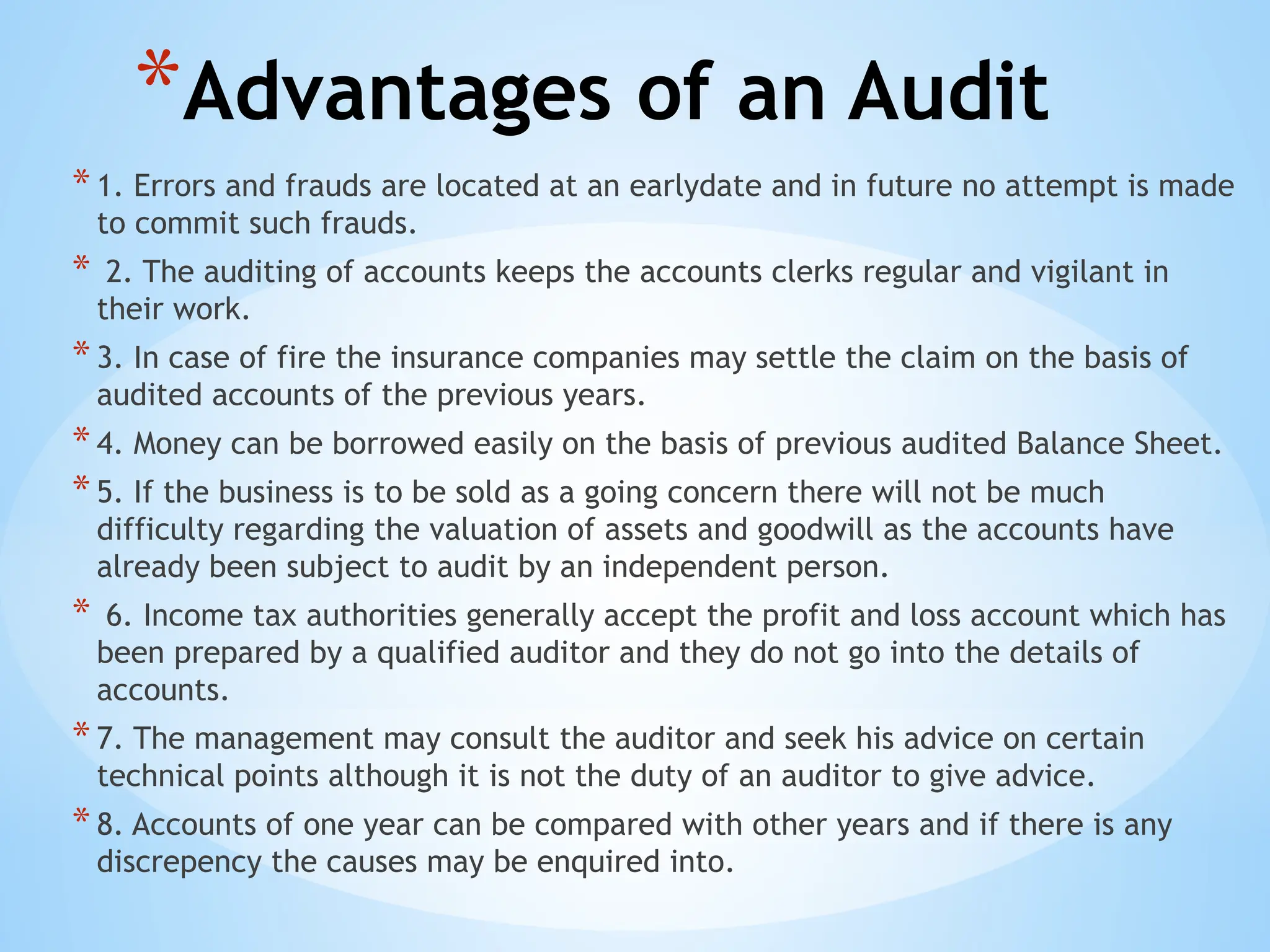

*Advantages of anAudit

*1. Errors and frauds are located at an earlydate and in future no attempt is made

to commit such frauds.

* 2. The auditing of accounts keeps the accounts clerks regular and vigilant in

their work.

*3. In case of fire the insurance companies may settle the claim on the basis of

audited accounts of the previous years.

*4. Money can be borrowed easily on the basis of previous audited Balance Sheet.

*5. If the business is to be sold as a going concern there will not be much

difficulty regarding the valuation of assets and goodwill as the accounts have

already been subject to audit by an independent person.

* 6. Income tax authorities generally accept the profit and loss account which has

been prepared by a qualified auditor and they do not go into the details of

accounts.

*7. The management may consult the auditor and seek his advice on certain

technical points although it is not the duty of an auditor to give advice.

*8. Accounts of one year can be compared with other years and if there is any

discrepency the causes may be enquired into.

10.

Importance of Auditing

*Auditedaccounts help a sole trader in knowing

the value of the business for the purpose of sale.

*Dispute over correctness of profits can be

avoided.

*Shareholders, who do not know about day-to-day

administration of the company , can judge the

performance of management from audited

accounts.

*It helps management in detecting and preventing

errors and frauds.

*Management gets advice on financial affairs from

the auditors.

11.

Importance of Auditing

*Longand short term creditors depend on audited

financial statements while taking decision to grant

credit to business houses.

*Taxation authorities depend on audited statements

in assessing the income tax, sales tax and wealth

tax liability of the business.

*Audited accounts are useful for the government

while granting subsidies etc.

*It can be used by insurance companies to settle the

claims arising on account of loss by fire.

*Audited accounts serve as a basis for calculating

purchase consideration in case of amalgamation

and absorption.

13.

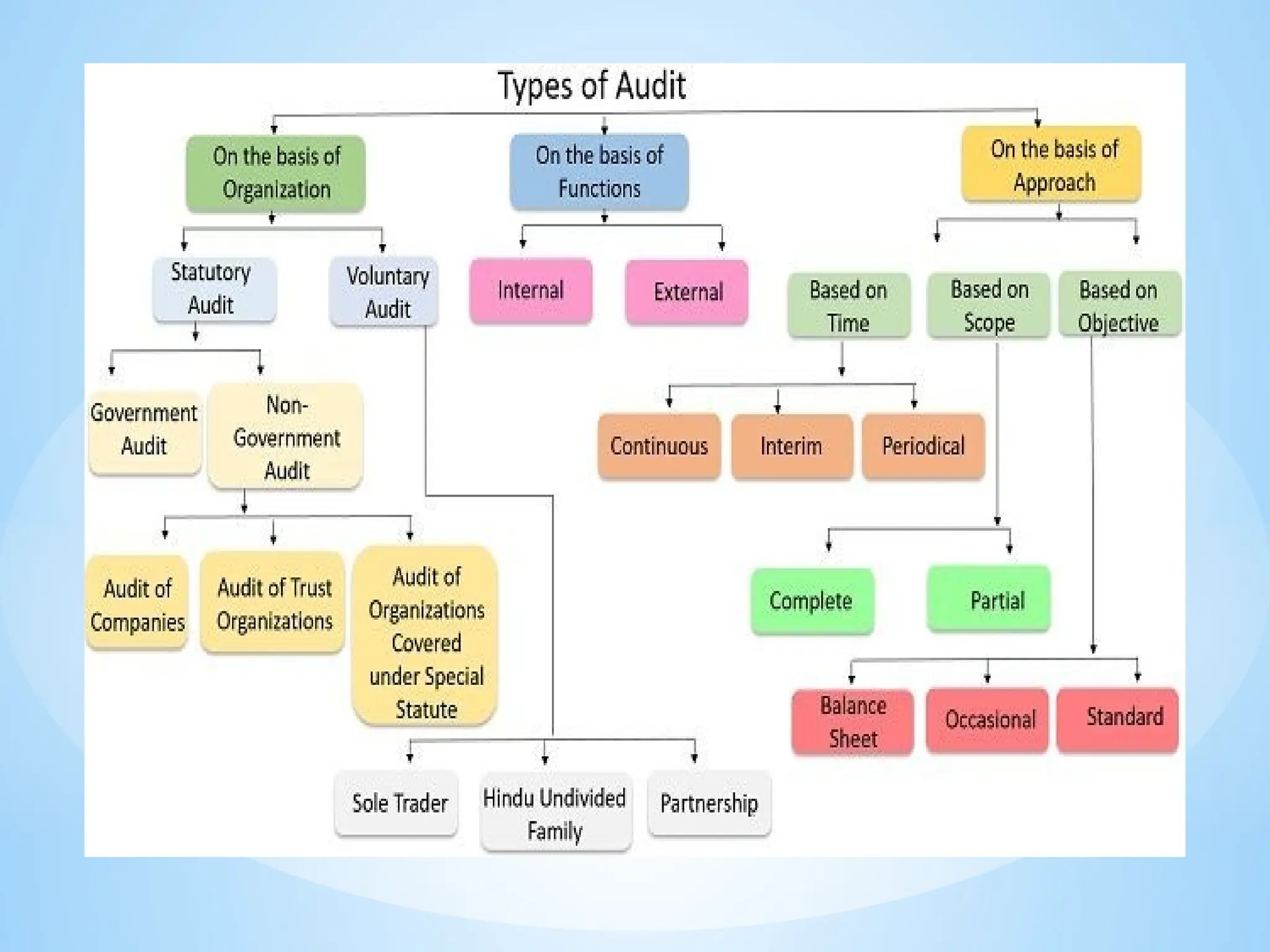

TYPES OF AUDIT

(1)On the basis of need of audit

a. External Need

*The auditor appointed to satisfy the External Needs of the

organization is known as EXTERNAL AUDITOR.

*If external need is a statutory need the same external auditor is

known as STATUTORY AUDITOR.

b. Internal Need

1. The auditor appointed to satisfy the internal or managerial

needs of the organization is known as INTERNAL AUDITOR.

2. According to AAS-7 The internal audit function constitutes a

separate component of internal control established with the

objective of determining whether other internal controls are well

designed and properly operated.

14.

(2) ON THEBASIS OF PERIOD OF AUDIT

(a)Continuous Audit

(b)(b) Interim Audit

(c)(c) Final/Annual Audit

*Continuous Audit:

The Continuous Audit is conducted throughout the year

or at the regular short intervals of time.

“A continuous audit involves a detailed examination of all the

transactions by the auditor attending at regular intervals say

weekly, fortnightly or monthly, during the whole period of

trading.”

- T.R. Batliboi

15.

Advantages of continuousAudit

a. Complete checking of all the records: Since the audit is

carried out throughout the year, sufficient time is available for

detailed checking. Any enquiry and doubt arising in the course

of audit can be tackled in a better way.

b. Proper planning: Auditor can plan his audit work in a

systematic manner. He can evenly spread his work throughout

the year. It will improve efficiency of auditor.

c. Early detection of frauds and errors: The work of auditor

becomes easier for detecting frauds and errors, otherwise it

will involve more time.

d. Up-to-date accounts: The efficiency of account staff will

increase and their work will be up-to-date and accurate.

e. Valuable suggestions: Continuous audit will help the auditor

to understand the technicalities of business. This will help the

auditor to make suggestions for the improvement of business.

16.

DISADVANTAGES OF CONTINUOUSAUDIT:

*a. Expensive: It is an expensive system as it may

not suit the budget of small organizations.

*b. Dislocation of routine work: Frequent visits by

auditor may dislocate the smooth flow of office

work.

* c. Alteration of Figures: after the accounts have

been audited, the figures may be fraudulently

altered by the staff.

*d. Losing link in the audit work: As the work is

not completed continuously, the auditor may lose

continuity and certain questions and inquires may

be left unanswered.

17.

ANNUAL AUDIT

Annual auditis one which is carried out only at the end of

an accounting period.

It as an audit which is not commenced until after end of

the financial period and is then carried on until completed.

Annual audit is also called periodical, final or completed

audit.

*Characteristics:

*It is done at the close of the financial year books of account have

been closed and final accounts drawn by the management of the

entity.

*The audit work is completed at a stretch i.e. in a single

continuous session.

*Generally this type of audit suitable to small organizations.

18.

INTERIM AUDIT

*An auditconducted between two annual audits is called

interim audit.

*More commonly it is known in case of banks as half yearly

review.

*Interim audit helps management to take timely and

appropriate decisions for example declaration of interim

dividend or valuation of shares to decide swap ratio in case

of a merger.

*Interim audit is gaining statutory status now a days various

regulating authorities like SEBI and RBI requires periodic

audited financial statements in between the two annual

audited financial statements.

*However, it is generally carried out by professionally

qualified auditors.

19.

*Final Audit

*Final Auditmeans when the audit work is conducted after

the close of financial year. A final audit is commonly

understood to be an audit which is not commenced until

after end of the financial period and is then carried on until

completed.

Balance Sheet Audit

1. Balance Sheet Audit relates to the verification of

various items of balance sheet such as assets, liabilities,

reserves and surplus, provisions and profit and loss balance.

2. The procedure under this audit is to follow a

backward process. First the item is located in balance sheet,

and then it is located in original record for the purpose of

verification.

20.

*Final Audit

*Final Auditmeans when the audit work is conducted after

the close of financial year. A final audit is commonly

understood to be an audit which is not commenced until

after end of the financial period and is then carried on until

completed.

Balance Sheet Audit

1. Balance Sheet Audit relates to the verification of

various items of balance sheet such as assets, liabilities,

reserves and surplus, provisions and profit and loss balance.

2. The procedure under this audit is to follow a

backward process. First the item is located in balance sheet,

and then it is located in original record for the purpose of

verification.

21.

INTERNAL CHECK

*Definition :

F.R.M.De Paula defines it as "Internal check means

practically a continuous internal audit carried on by the staff

itself, by means of which the work of each individual is

independently, checked by other members of the staff".

Objects of Internal Check :

1) To prevent the commission of any error or fraud by a clerk.

2) To prevent the misappropriation of cash or goods by any

clerk by keeping a check on the receipts and payments of cash

and receipts and delivery of the goods.

3) To throw responsibility on a particular clerk when the fraud

or mistake is detected.

4) To detect a fraud or an error quickly and easily. 5) To have

an accurate record of all business transactions.

22.

INTERNAL CONTROL

Control isa wider term and will include all types of

management controls.

It is a means of assisting modern business management in

discharging its function.

The term internal control has been defined as "the whole

system of controls, financial or otherwise established by the

management in order to carry on the business of the company

in an orderly manner safe guard its assets and secure as far as

possible the accuracy and reliability of its record.

" According to this definition, internal control means

a/. accounting control

b/. operation controls i.e.; quality control, budgetary control,

internal checks and internal audit etc.

23.

TEST CHECK

In thosebusiness houses where a satisfactory and

effective system of internal check is in operation, it is not

necessary for the auditor to do detailed checking.

The usual practice is that a certain number of entries of each

class is selected and checked and if they are found correct,

the remaining entries are also taken to be correct.

This is known as "Test checking".

The selection of items and the extent of test checking would

mainly depend upon the auditor's judgement and assessment

of a particular situation

24.

Preparation of AuditProgramme

Audit programme is a description, memorandum or

outline of the work to be done in an audit and often of

the time allotted and personnel assignments, prepared

by an auditor for the guidance and control of

assistants. It is the auditors plan of action, specifying

the procedures to be followed.

Objects of audit programme :

• To obtain informations regarding the accounting system,

policies and control techniques of the client.

• To ascertain the extent to which internal control techniques

can be banked upon.

• To lay down the nature, time and extent of audit

techniques to be adopted.

• To co-ordinate the total works.

25.

Advantages of auditprogramme : Disadvantages

Division of work as per ability i. Mechanization of work

Determination of responsibilities ii. No motivation for free decision

Progress of work iii. Want of constructive thinking

Change of employees won’t affect work iv. Want of moral influence

Uniformity in work v. Planned frauds are undisclosed

Protection in court of law vi. Disabilities remain concealed

Complete examination vii. Plea against auditor

Time saver

Facility of review

Pursuance of audit principles