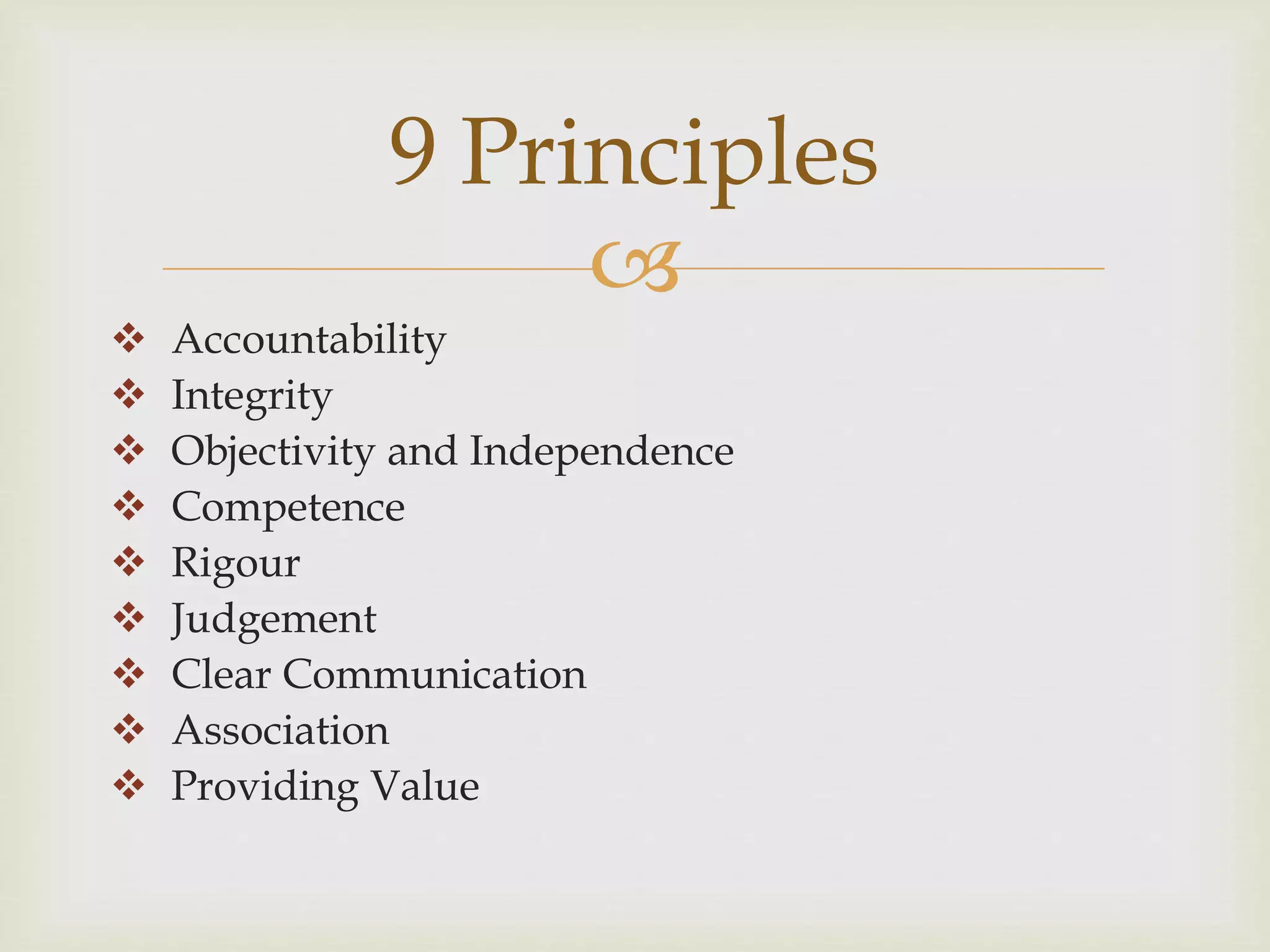

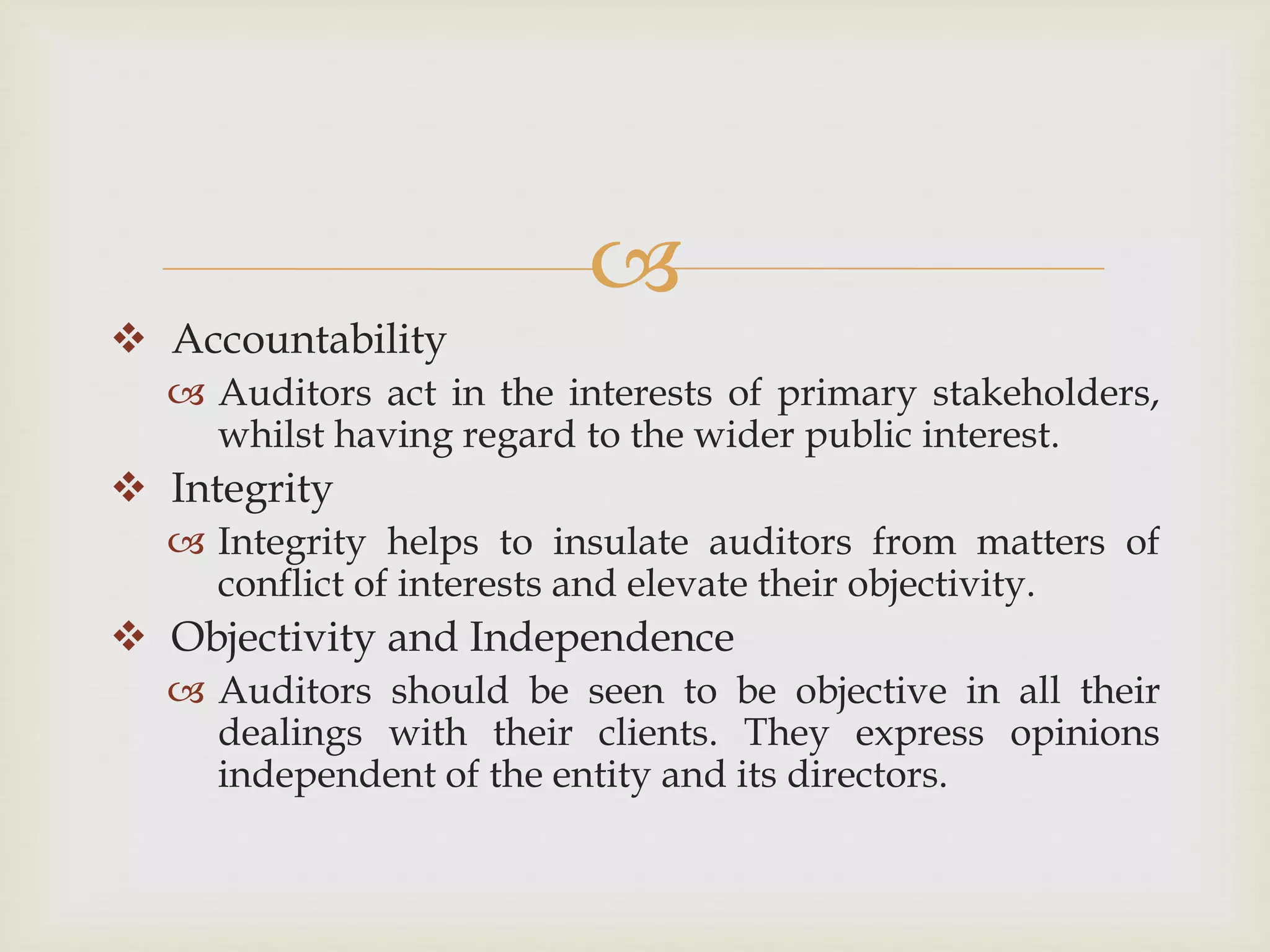

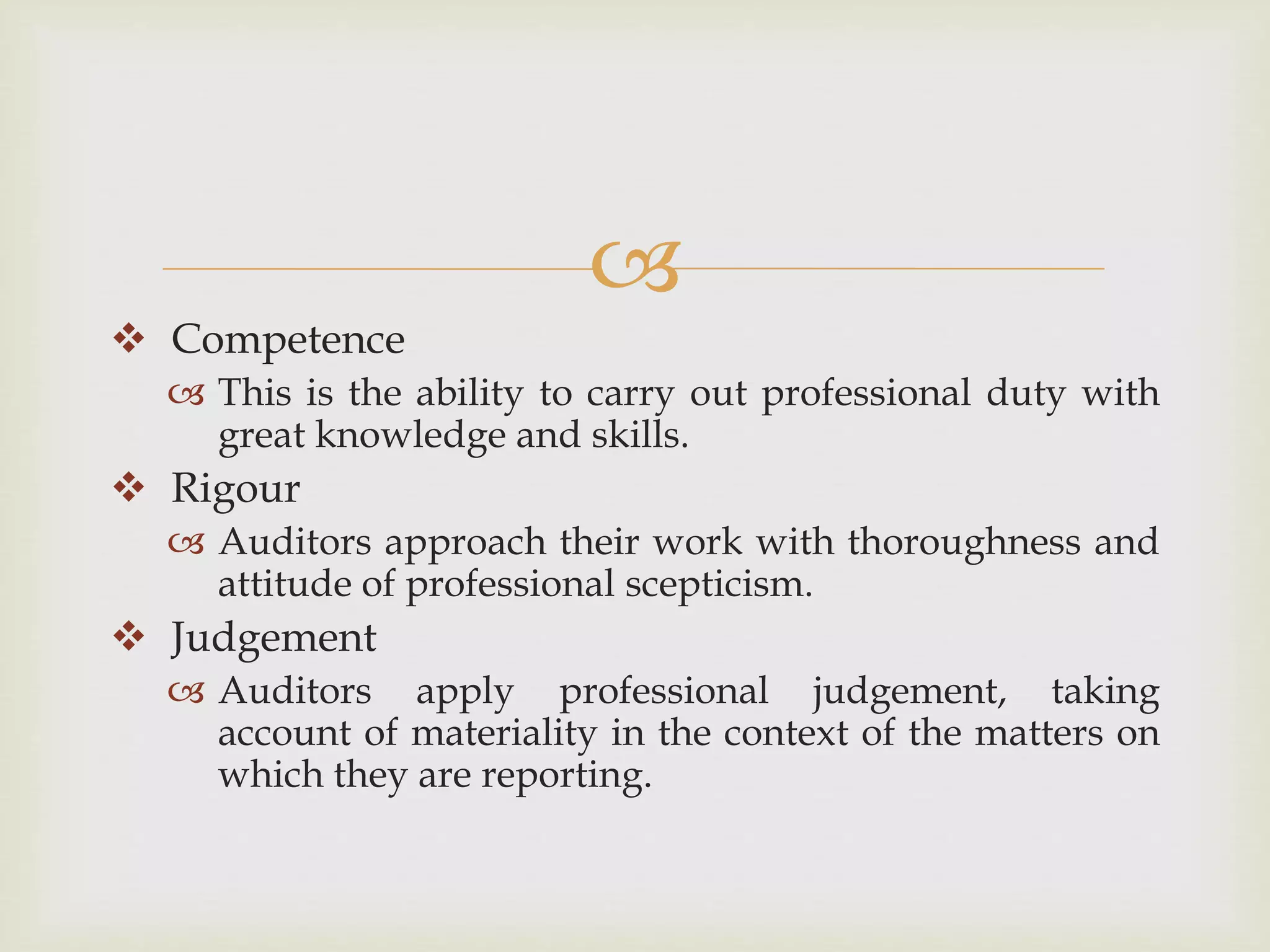

The document outlines 9 principles for auditors: accountability, integrity, objectivity and independence, competence, rigour, judgement, clear communication, association, and providing value. It provides a brief definition for each principle, emphasizing auditors' responsibility to act in the interests of stakeholders, maintain objectivity and independence in their work, approach tasks with thoroughness and professional skepticism, and clearly communicate their opinions.

![AUDIT REPORT [ AUDITING ]](https://cdn.slidesharecdn.com/ss_thumbnails/auditingtypesofauditreport-210303052610-thumbnail.jpg?width=640&height=640&fit=bounds)