Back to the future - the return of DB surpluses (slides) - 9 December 2025.pdf

1.

Back to theFuture: The Return of DB surpluses

Key Thoughts

9 December 2025

2.

Objectives

What the sessionwill cover

• What history tells us about surplus use and the

lessons for today

• How surpluses have evolved and why they’re

back on the agenda

• The scale of surpluses in the past and the likely

tax revenues from surplus in the future

• The government’s budget reforms on surplus and

their implications for schemes

• Aberdeen / Stagecoach

Statutory surplus era(1987 – 2006)

Background

• Prior to 1987 tax relief was available on contributions, investments rolled up tax free and

refunds were returned without a tax charge – were companies using schemes as a tax favoured

savings vehicle to avoid Corporation Tax?

• Finance Act 1986 introduced a 40% refund tax charge and ‘excessive’ surplus rule

• DB schemes must reduce surplus to no more than 5% of liabilities on a prescribed basis to

maintain their full tax-exempt status by:

• Increasing member benefits, reducing employer and/or employee contributions,

refunding to the employer or any mix of the above

• In the early 1990s, approximately 40% of large DB schemes (>12 members) had an excessive

statutory surplus (>105% funded) with approximately a further 10% in surplus (100 – 105%

funded)

5.

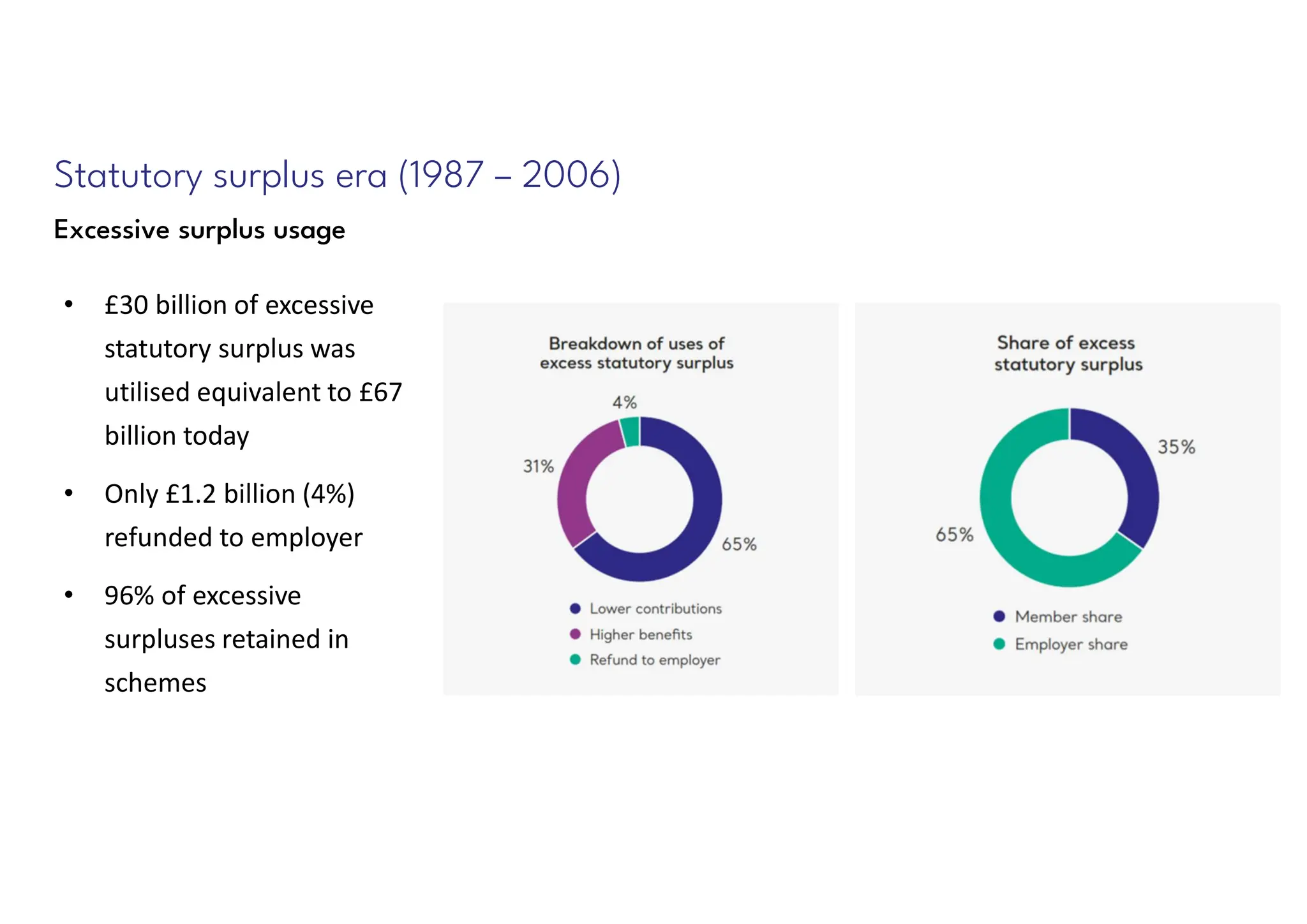

Statutory surplus era(1987 – 2006)

Excessive surplus usage

• £30 billion of excessive

statutory surplus was

utilised equivalent to £67

billion today

• Only £1.2 billion (4%)

refunded to employer

• 96% of excessive

surpluses retained in

schemes

6.

Statutory surplus era(1987 – 2006)

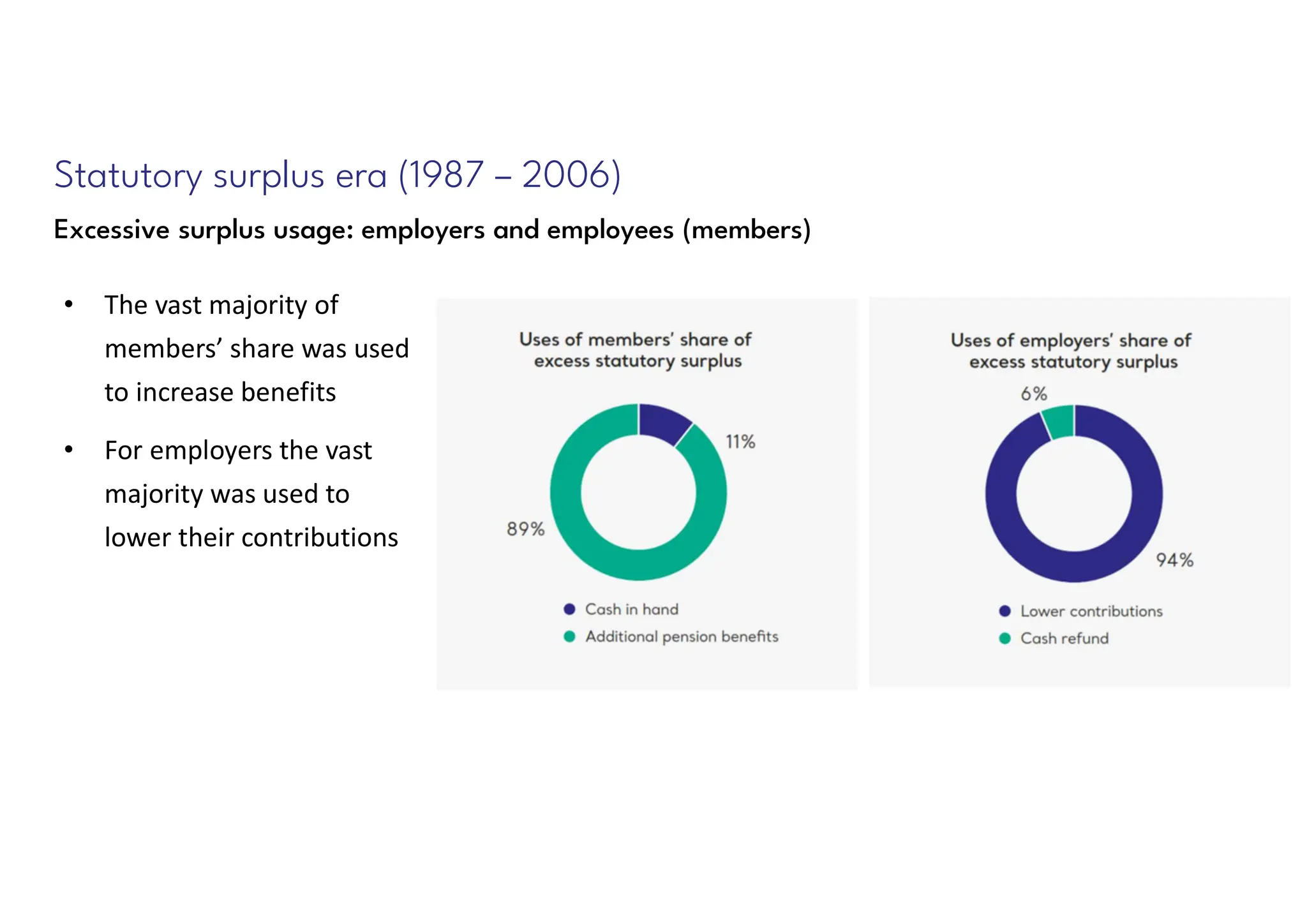

Excessive surplus usage: employers and employees (members)

• The vast majority of

members’ share was used

to increase benefits

• For employers the vast

majority was used to

lower their contributions

7.

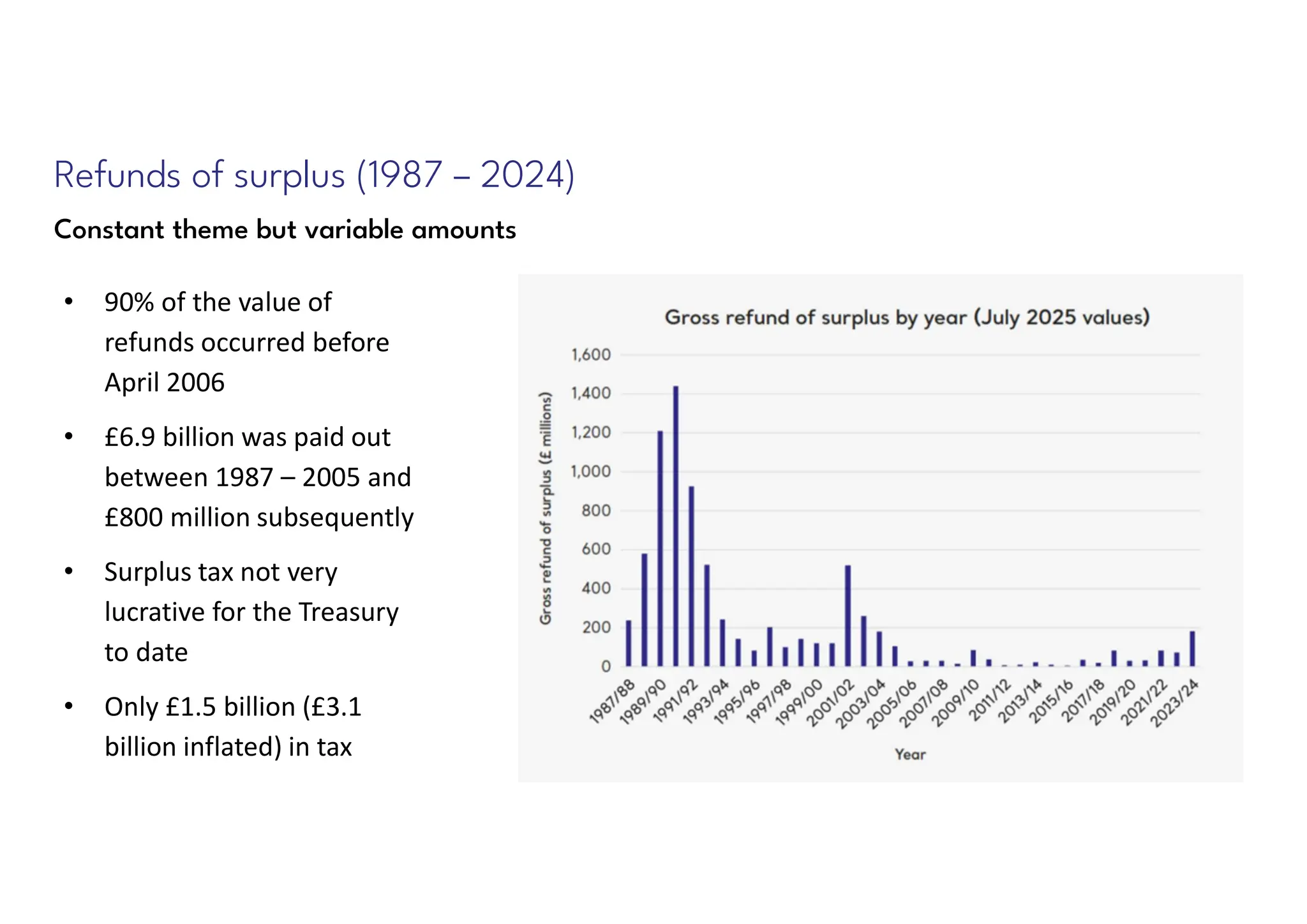

Refunds of surplus(1987 – 2024)

Constant theme but variable amounts

• 90% of the value of

refunds occurred before

April 2006

• £6.9 billion was paid out

between 1987 – 2005 and

£800 million subsequently

• Surplus tax not very

lucrative for the Treasury

to date

• Only £1.5 billion (£3.1

billion inflated) in tax

8.

Recent developments

Budget usesof surplus

The November 2025 Budget contained two surplus uses that are noteworthy:

• The investment reserve in the British Coal Staff Superannuation Scheme will be transferred

to scheme members at a cost to the taxpayer of £2 billion

• The PPF (and FAS) will provide inflation protection on pre 1997 benefits where members’

former schemes provided it, from January 2027, at a cost of £1.3 billion in 2026/27 (and £60

million+ per annum thereafter)

These public sector surplus uses equate to approximately the first 7.5 years of ‘Mansion Tax’

that will be levied by the High Value Council Tax Surcharge (2028/29 through mid-2035)

9.

Recent developments

Budget taxrelaxation

The November 2025 Budget also introduced that well funded DB schemes can make direct lump

sum payments to members over Normal Minimum Pension Age (currently 55) if scheme rules

and trustees permit (from April 2027)

• Now treated as authorised payments

• Easier for trustees and employers to agree surplus sharing without adding long-term

liabilities

• Encourages a ‘Christmas surplus bonuses’ culture supporting run-on strategies

10.

Recent developments

Aberdeen /Stagecoach transaction

Aberdeen Group plc (“Aberdeen”) has become the sponsoring employer of the Stagecoach Group

Pension Scheme (“SGPS”) taking responsibility for funding and managing £1.2 billion of assets

• Aberdeen already has its own DB plan (£2.6 billion assets with a significant surplus)

• SGPS continues to ‘run on’

• Aberdeen gets a minority share of future surplus, majority earmarked for members

• Immediate pension uplift of 1.5% for all SGPS members (approximately £50 million value)

• Stagecoach gets to exit completely – covenant link severed

• Trustee board anticipated to remain as is

• Aberdeen adds AUM, positions for surplus-sharing upside, assumes governance and risk

• Market response: Aberdeen share price virtually unchanged

This presentation isbased on our understanding of current legislation which may change in future.

Punter Southall is a trading name of Punter Southall Defined Contribution Consulting Limited, which is authorised and

regulated by the Financial Conduct Authority. Our Financial Services Register reference number is: 121328. Registered

Office: 11 Strand London WC2N 5HR. Registered in England and Wales No 0873463

For any further questions, please contact:

Thank you

Richard Jones

richard.jones@puntersouthall.com