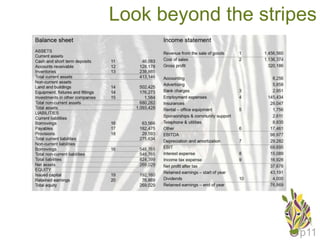

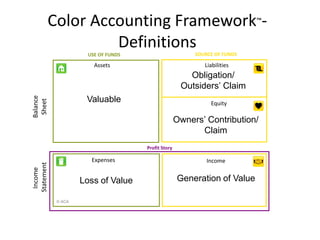

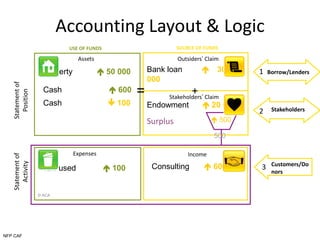

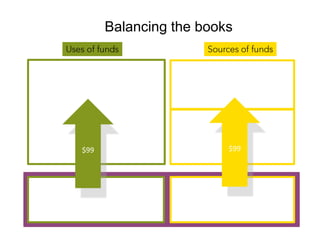

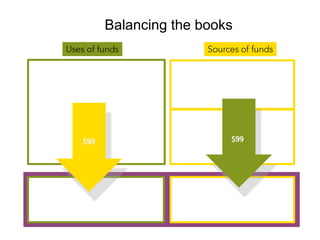

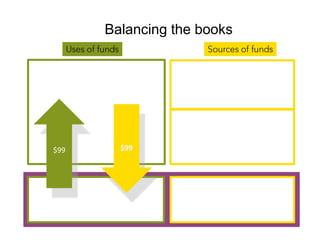

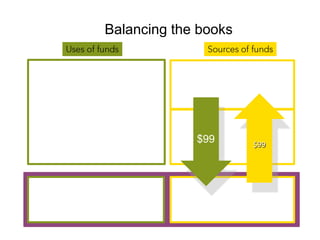

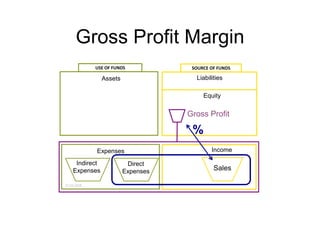

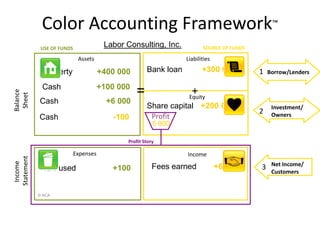

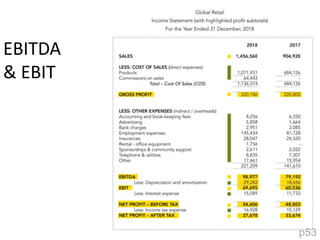

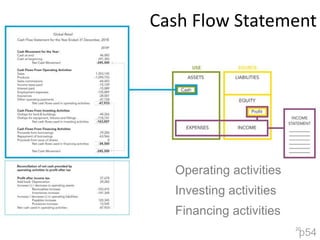

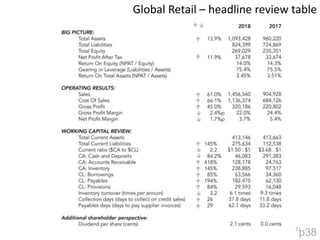

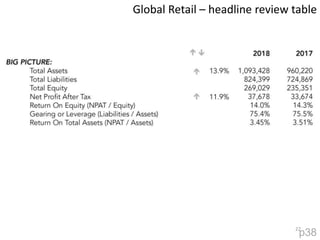

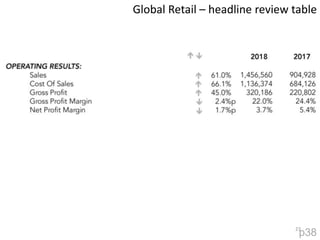

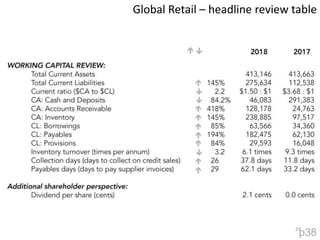

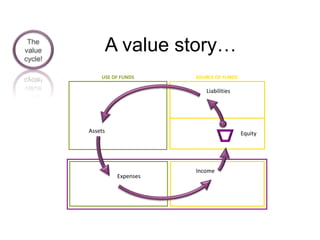

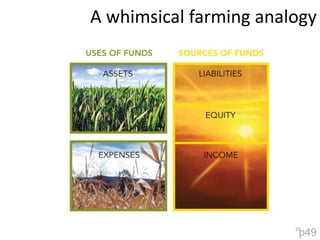

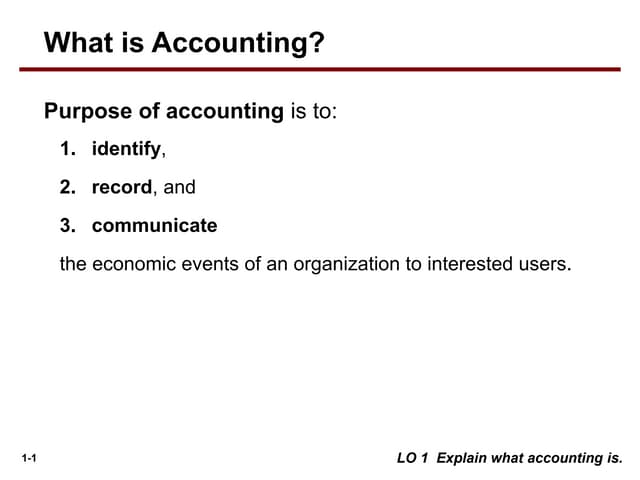

The document discusses the foundational elements of business acumen for learning professionals, emphasizing the significance of understanding financial metrics and accounting principles. It covers the duality of accounting, essential transactions, and the importance of balancing sources and uses of funds to create value. Additionally, it includes various financial statements and examples to illustrate income, expenses, assets, and liabilities.