Downloaded 39 times

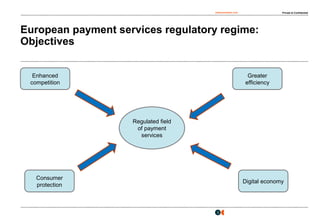

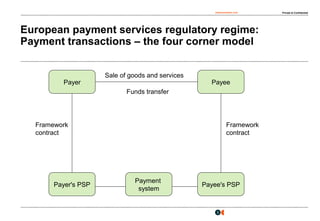

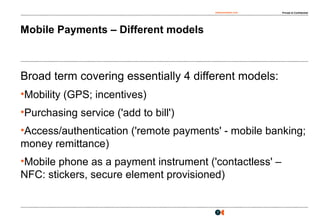

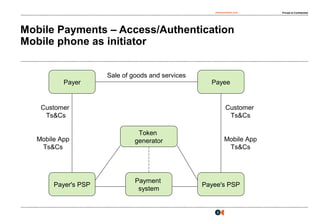

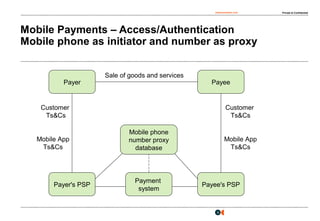

This document discusses regulatory issues surrounding transformational mobile payment projects in Europe. It provides an overview of the European payment services regulatory regime, including its objectives to enhance competition and consumer protection. It also outlines key measures like the Payment Services Directive. The document then examines how this framework applies to different mobile payment models involving access/authentication or using a mobile phone as a payment instrument. It identifies specific regulatory issues regarding payment services, data protection, and customer lifecycles. Finally, it notes the convergence of financial services and digital businesses in payments and increasing diversity of payment methods.