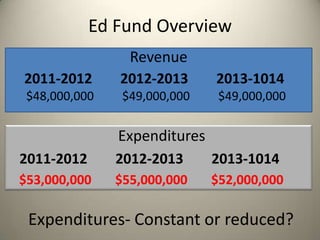

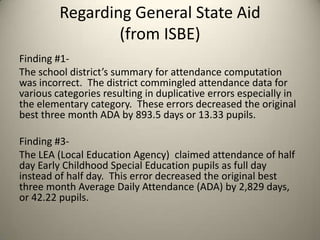

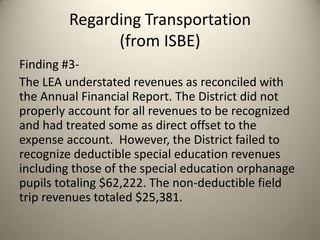

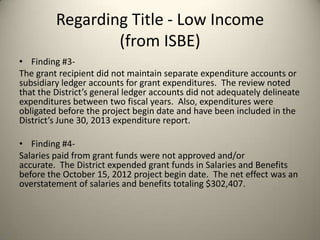

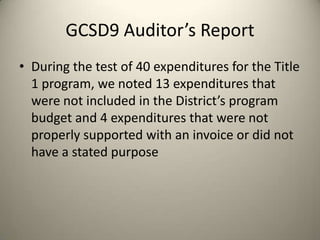

This document summarizes a town hall meeting on March 25, 2014 about the finances of the Granite City School District. It discusses how the district claims rising teacher salaries and benefits are causing budget deficits, but provides evidence that calls these claims into question. Audits found errors in how the district reported attendance data and categorized special education students, underestimated some revenues, and had issues with journal entries, expenditure reporting, and supporting documentation for Title grants. The district has also faced questions around administrative spending and unnecessary expenses. An forensic audit is suggested to truly understand the district's finances.