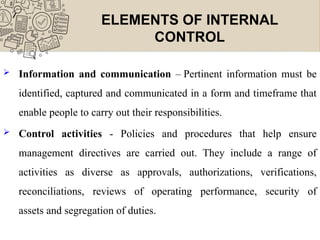

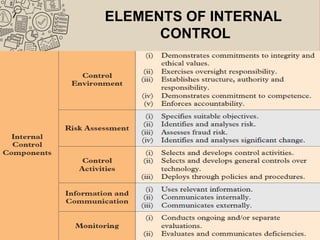

An internal control system is essential for organizations to manage risks and achieve goals, as defined by both Bursa Malaysia and COSO. It encompasses various components such as control environment, risk assessment, and control activities, which are vital for maintaining operational integrity and compliance with laws. Types of controls include preventive measures to avoid errors and detective measures to identify and address issues after they occur.