Download to read offline

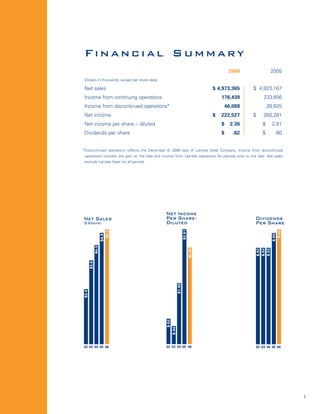

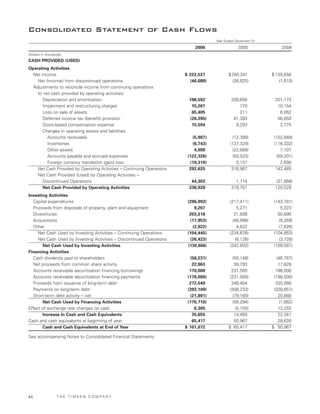

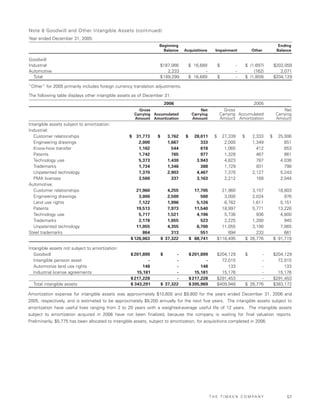

The document is Timken's 2006 annual report which discusses the company's vision for profitable growth through transforming the company. Some key points: - In 2006, Timken embarked on significant changes including investing in growth markets, improving its portfolio through divesting non-strategic businesses, and restructuring. - Financially, net sales reached $5 billion and net income per share was $2.36, among the highest in Timken's history. - The company increased manufacturing capacity in aerospace and heavy industry and expanded its presence in Asia. It also acquired businesses and developed new capabilities to better serve customers. - Timken improved its portfolio through selling businesses and pursuing restructuring activities to improve