Download to read offline

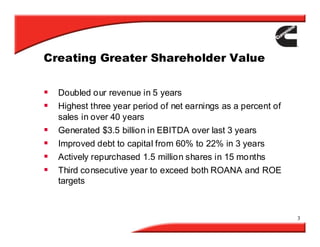

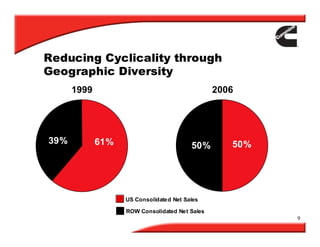

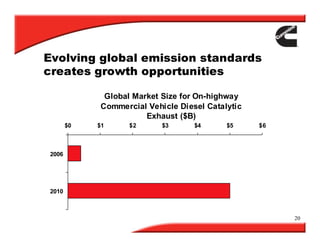

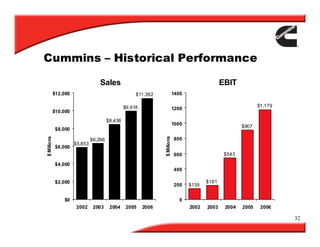

- Cummins has doubled revenue over the past 5 years and achieved the highest 3-year period of net earnings as a percent of sales in over 40 years. - The company has diversified globally and by end markets to reduce cyclicality, aggressively pursued low cost leadership, and built greater earnings stability. - Cummins is investing in new engine platforms and technologies to capitalize on growth opportunities from evolving global emission standards.