Download to read offline

![The business case for reducing emissions To suggest amends/updates to content, email: Toby.Pickard@igd.com

Please give us feedback

Section three: Reputation

Customer and consumer confidence

Retailers and manufacturers must ensure that

consumers trust the brands they buy. Trust can be

undermined by concerns about the way in which a

product is manufactured or where ingredients come

from. For example, the use of ingredients that have

caused deforestation will have a negative impact on

brand reputation.

On the contrary, some initiatives can enhance

reputation; a reduction in food waste sent to landfill will

have a positive impact on business or brand reputation.

Brands that engage consumers in their sustainability

credentials are more likely to build long-term trust. This

translates into a stronger commercial performance and

a more sustainable market share.

Tangible measures of consumer confidence are sales

growth and market share. Companies can include

questions about their environmental credentials

in regular brand tracking questionnaires. This will

allow organisations to identify if their environmental

performance is perceived to be improving.

Employee recruitment and retention

Employees are more likely to want to work for a business

with a good sustainability reputation.

Studies have shown that recruitment of higher calibre

individuals and improved retention can be achieved

through having a positive reputation.

Employees may be prepared to accept a lower salary to

work for a business that fits with their ideals.

Success in this area can be measured by employee

turnover, the number of unfilled vacancies as well as

via internal questionnaires and exit interviews that

measure the views of employees on an organisation’s

environmental credentials.

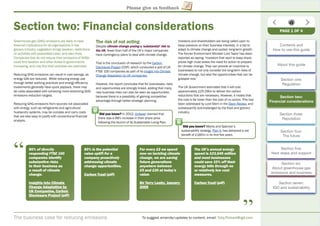

Below is a list of organisations and indexes that

benchmark organisations on sustainability credentials.

It may be worth considering entering into the awards or

at least understanding their criteria for success to help

improve reputation?

- Interbrand Best Green Brand

- Goodbrand Social Equity Index

- WPP Top Green Brands Index

- BitC Corporate Responsibility Index

- FTSE4Good Index

- Dow Jones Sustainability Index

- The Times Green Company awards

- IGD FIA Awards

- BusinessGreen Leaders Awards

- Green Retailer of the Year

- Green Supplier of the Year

- Green Wholesaler of the Year

- Guardian Green Business Awards

- Carbon Disclosure Project

- International Green Awards

79% of CFOs believe ESG

[environmental, social,

governance] programmes

add value to the business by

maintaining good corporate

reputation and/or brand equity.

McKinsey Global Survey ofy y

CFOs: Valuing corporate socialg p

responsibility.p y

“

“

The Co-operative Group report

that its ethical policy has

positively impacted customer

attrition. 88% of The Co-operative

Food’s customers believe that its

ethical policy made the business

more appealing.

BitC

Did you know? Marks & Spencer claim that

candidates often mention Plan A as a reason why

they want to work for them, and their employee

survey confirms that Plan A contributes to job

satisfaction.

Did you know? Over half of the student

population (58%) would take a 15% pay cut to

“work for an organisation whose values are like my

own“

Talent Report: What workers want in 2012 (pdf)

PAGE 3 OF 3

Contents and

How to use this guide

About this guide

Section one:

Regulation

Section two:

Financial considerations

Section three:

Reputation

Section four:

The future

Section five:

Next steps and support

Section six:

About greenhouse gas

emissions and business

Section seven:

IGD and sustainability

Did you know? United Biscuits achieved Platinum

status for the second year running in Business in

the Community’s Corporate Responsibility (CR)

Index 2011.](https://image.slidesharecdn.com/20ad433a-6b39-48bc-83c3-c9cf744646d1-150715143548-lva1-app6891/85/The-business-case-for-reducing-emissions-14-320.jpg)

The document provides guidance to businesses on reducing greenhouse gas emissions. It discusses three key drivers for reducing emissions: regulation, financial considerations, and reputation. Regarding regulation, it outlines major UK and EU policies aimed at reducing emissions, including the Climate Change Act, Carbon Reduction Commitment, and Energy Performance of Buildings Regulations. It also provides a hierarchy of actions for reducing emissions and tips for measuring and cutting emissions.

![Environmental_Sustainability_Matrix[4]](https://cdn.slidesharecdn.com/ss_thumbnails/21e034b0-2dcd-4b88-9663-4ebb36354e65-150715143437-lva1-app6891-thumbnail.jpg?width=640&height=640&fit=bounds)