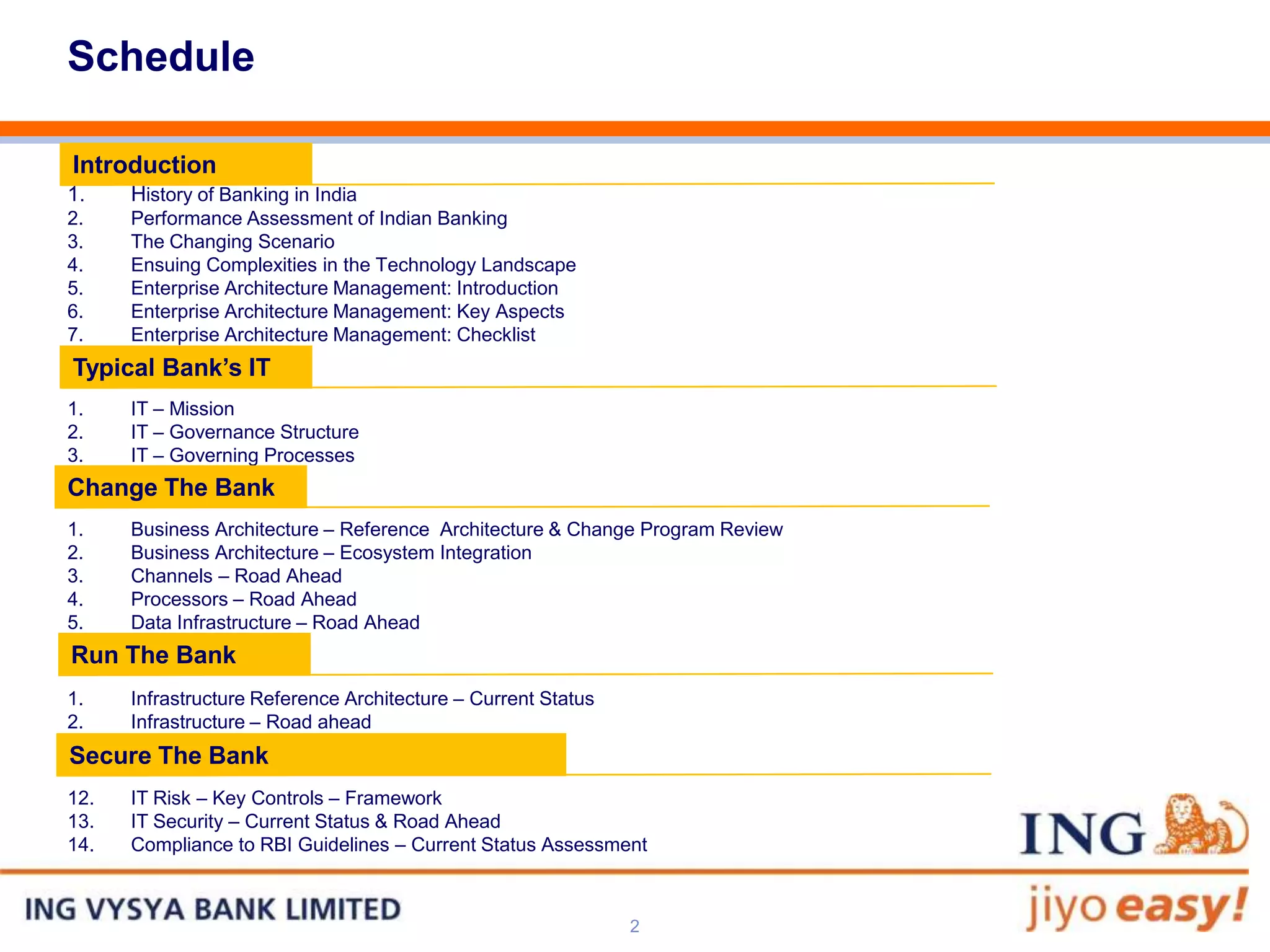

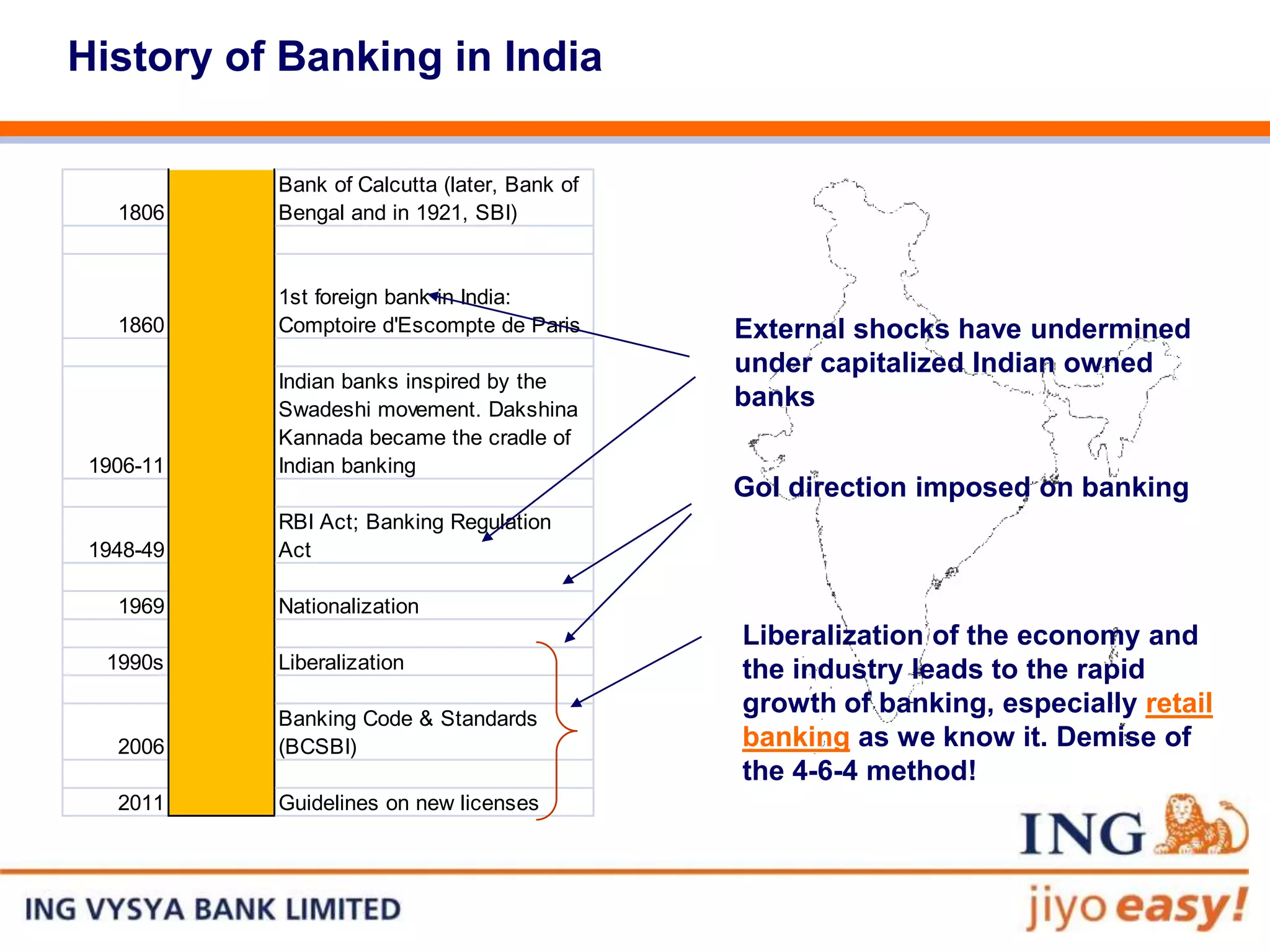

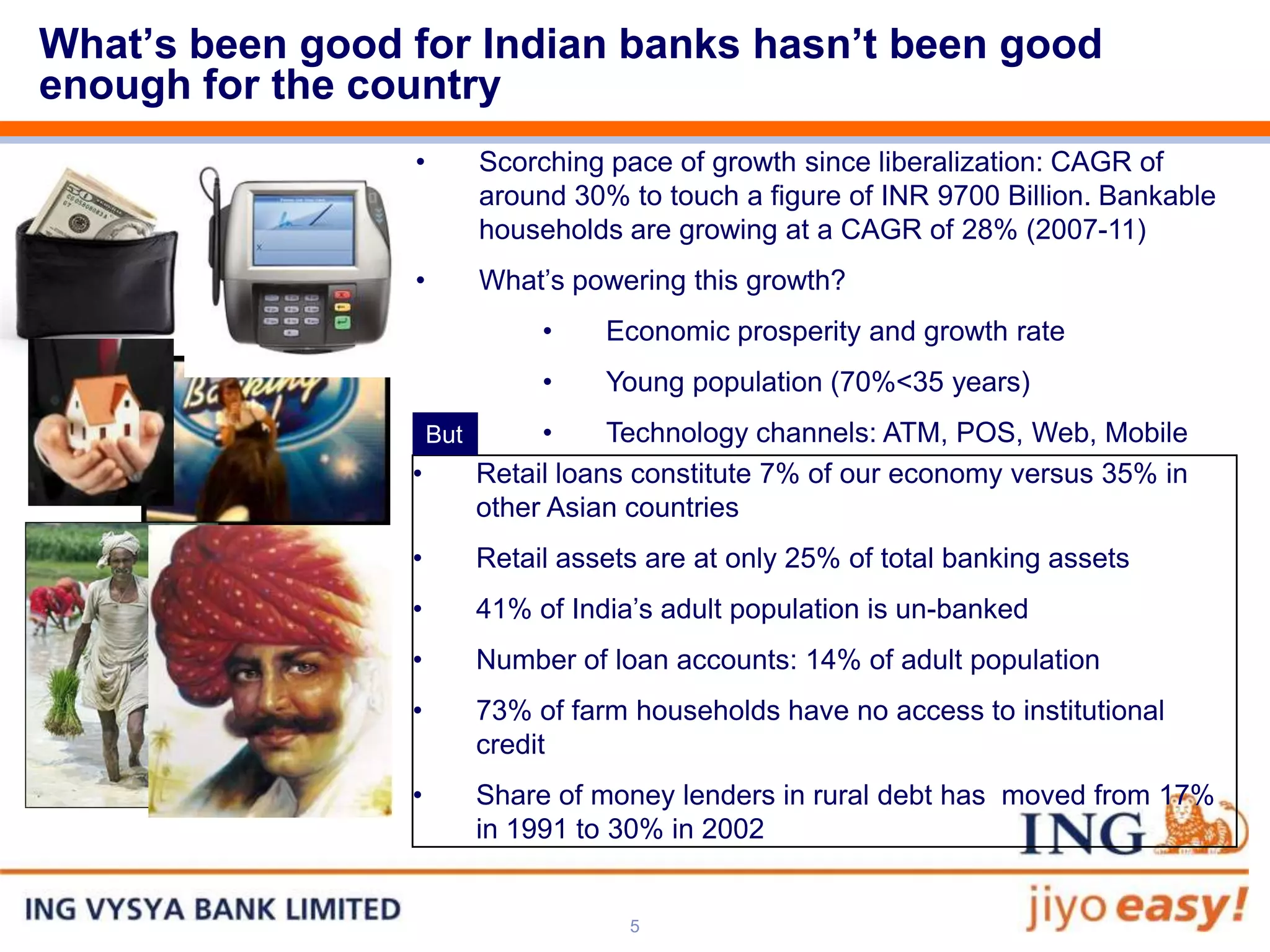

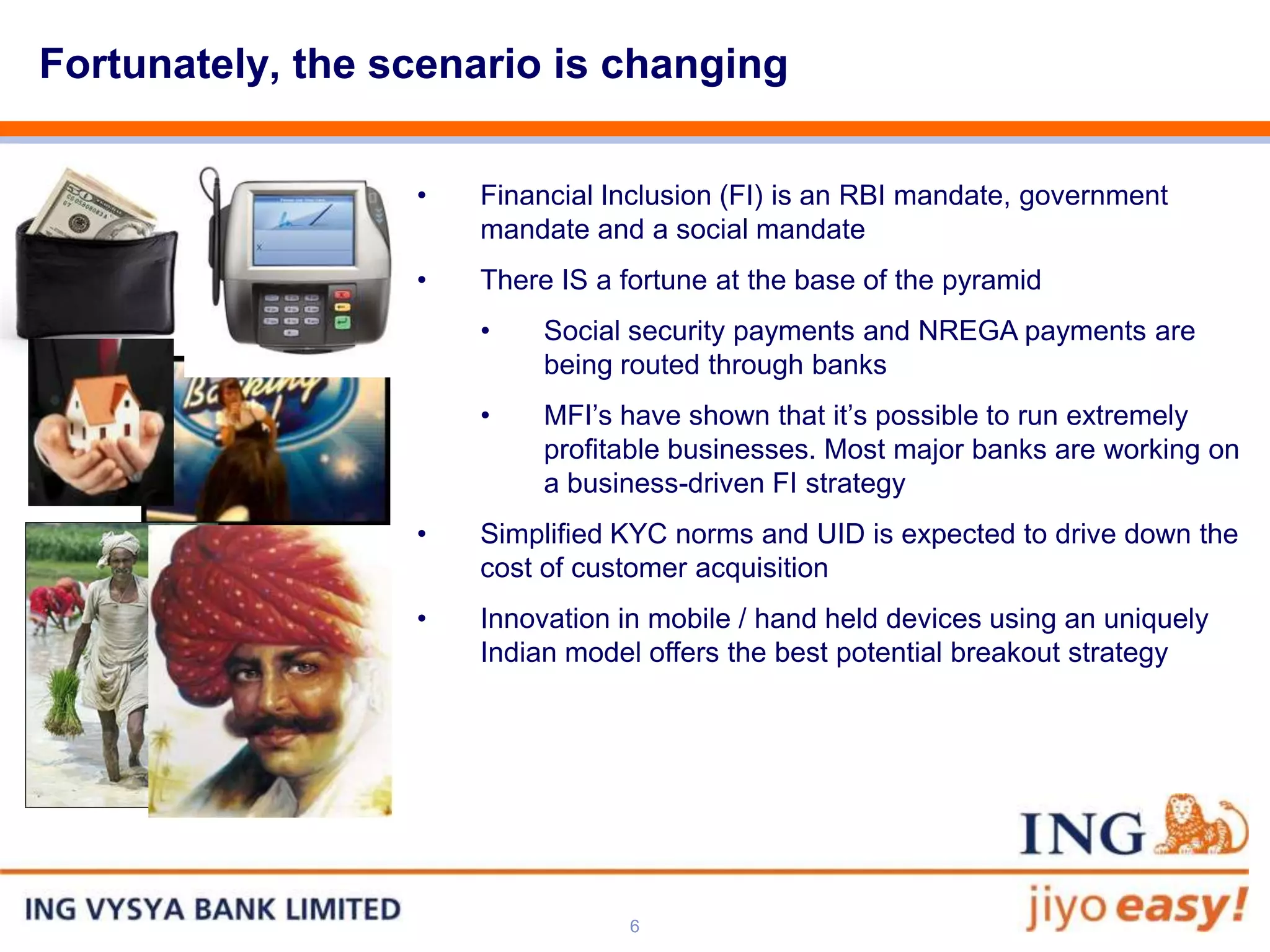

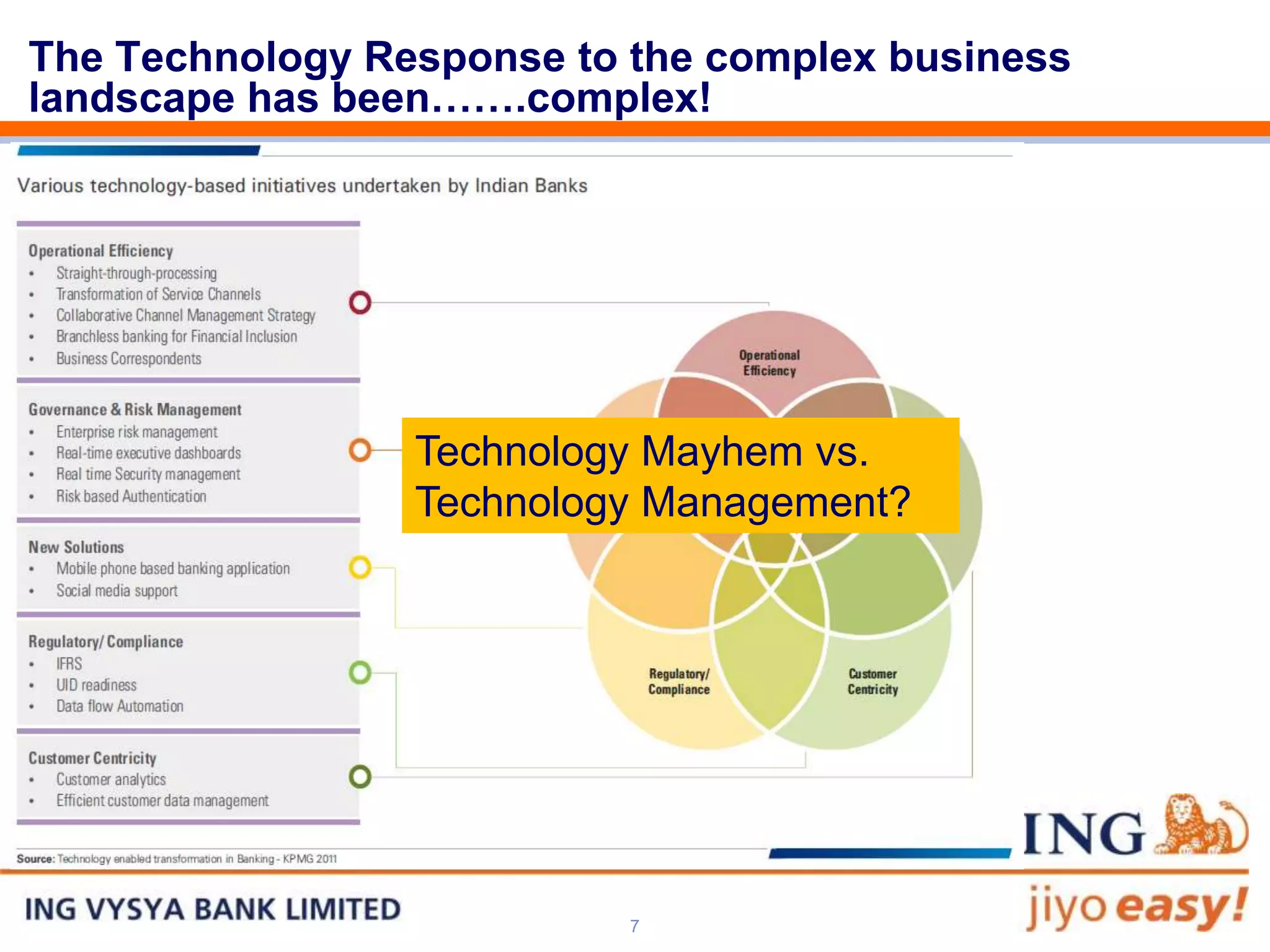

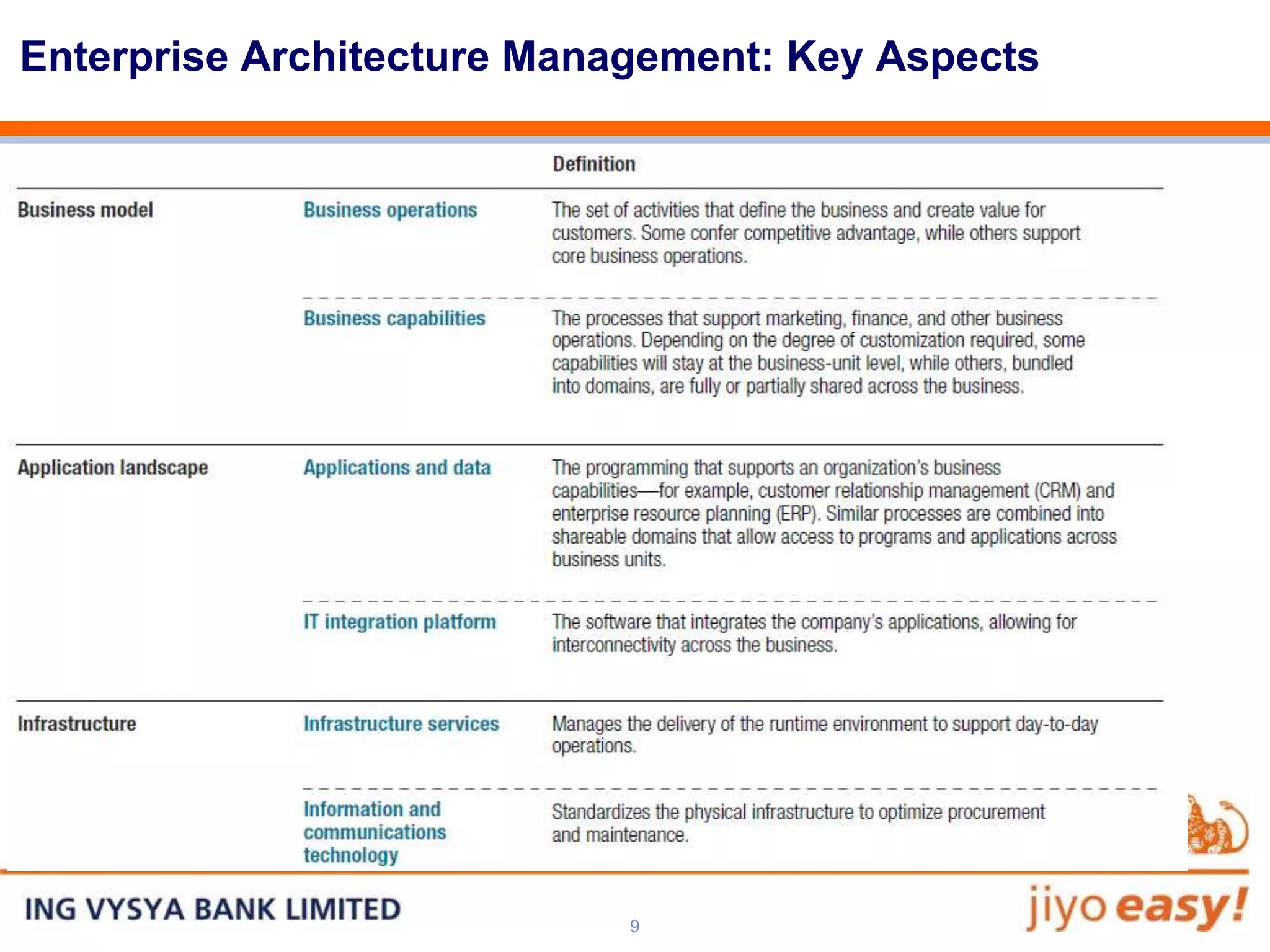

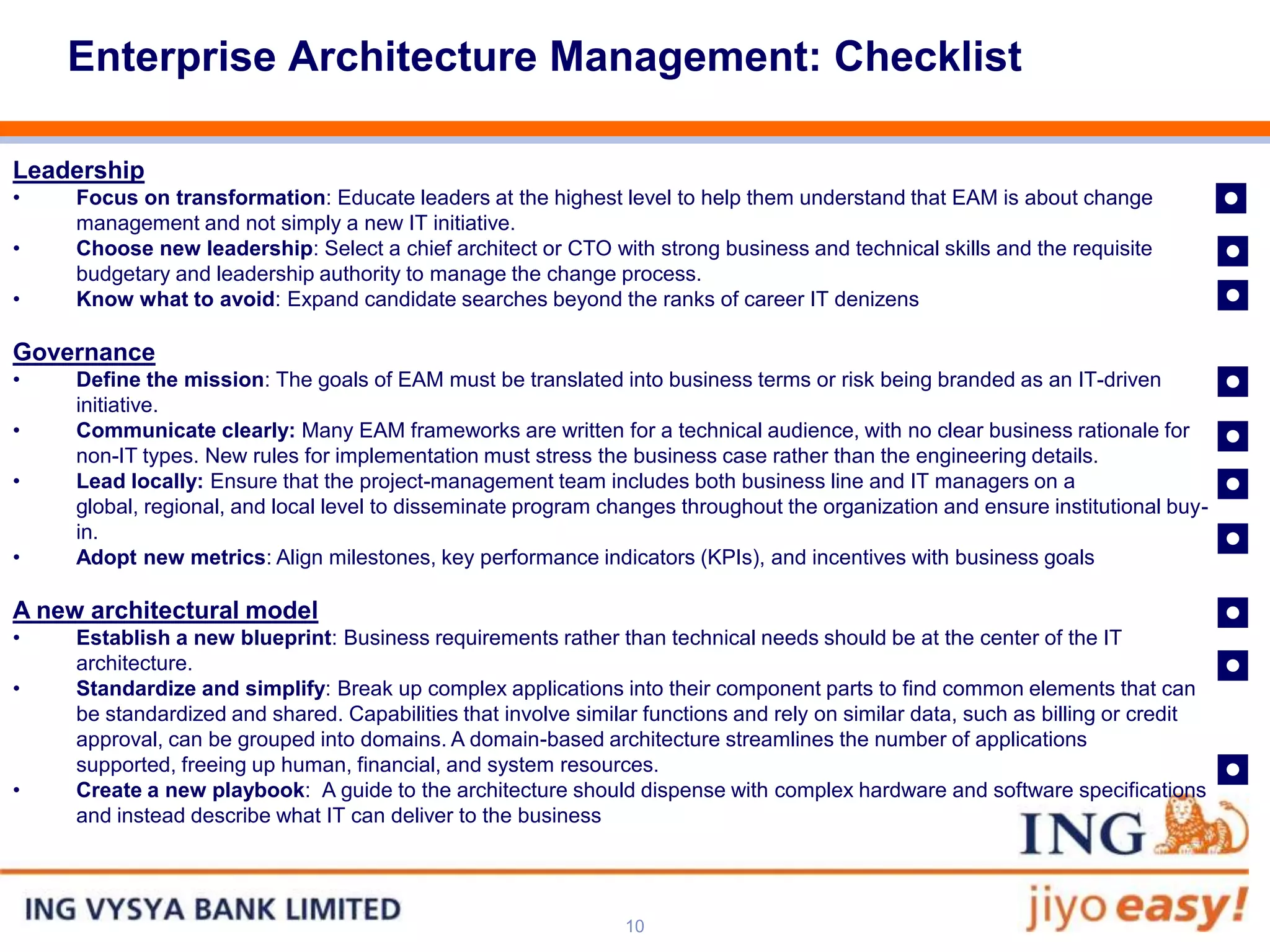

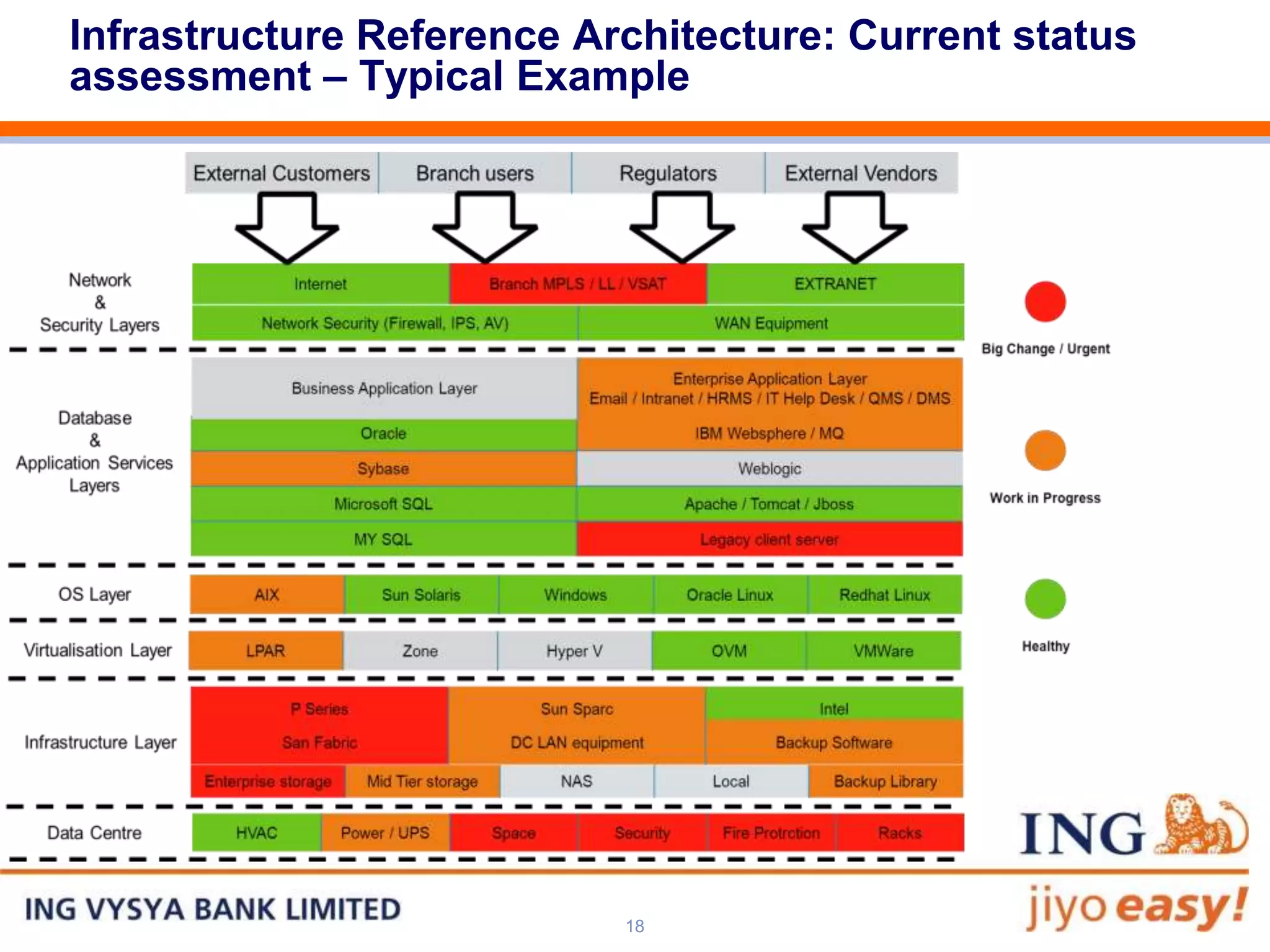

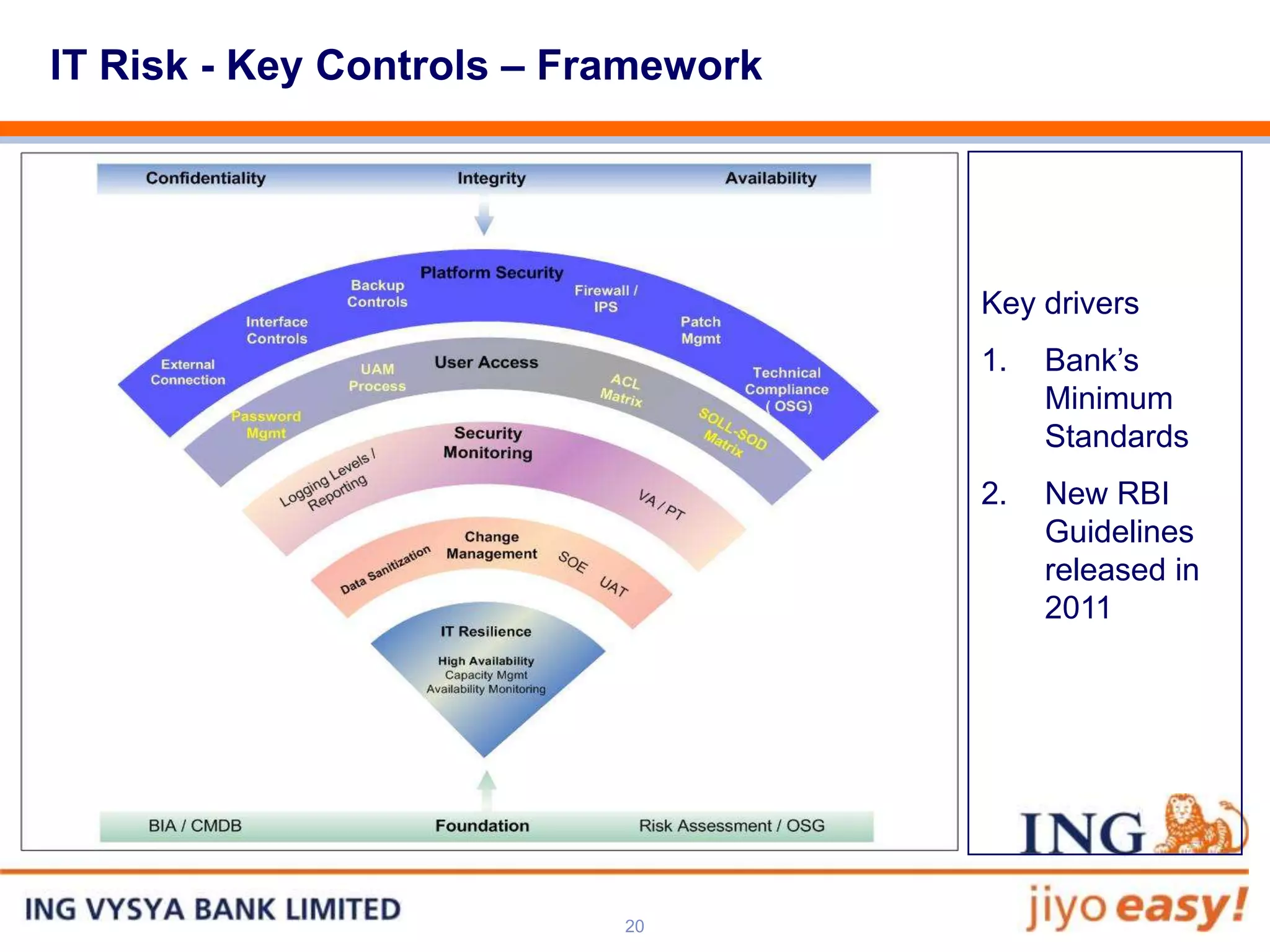

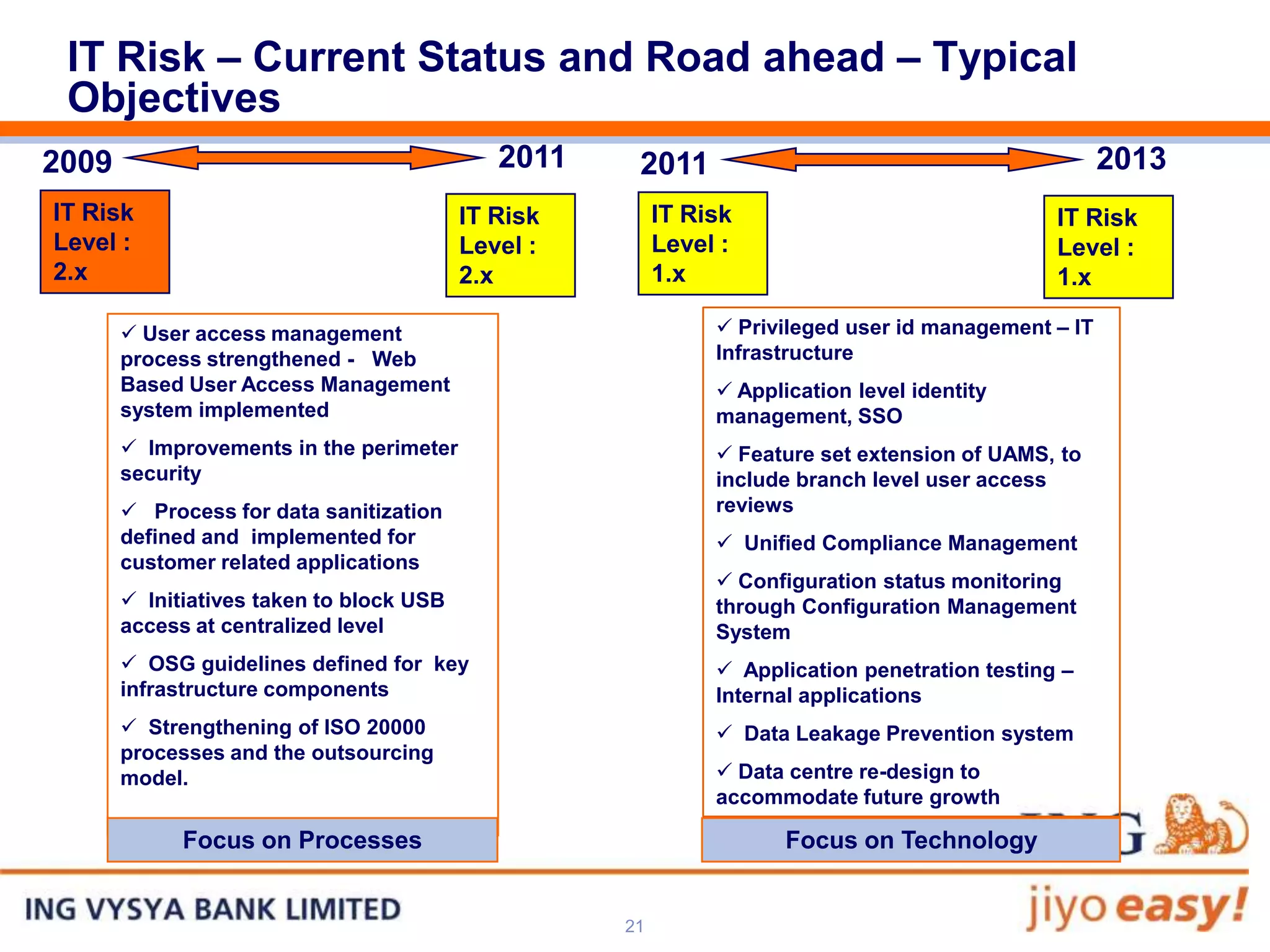

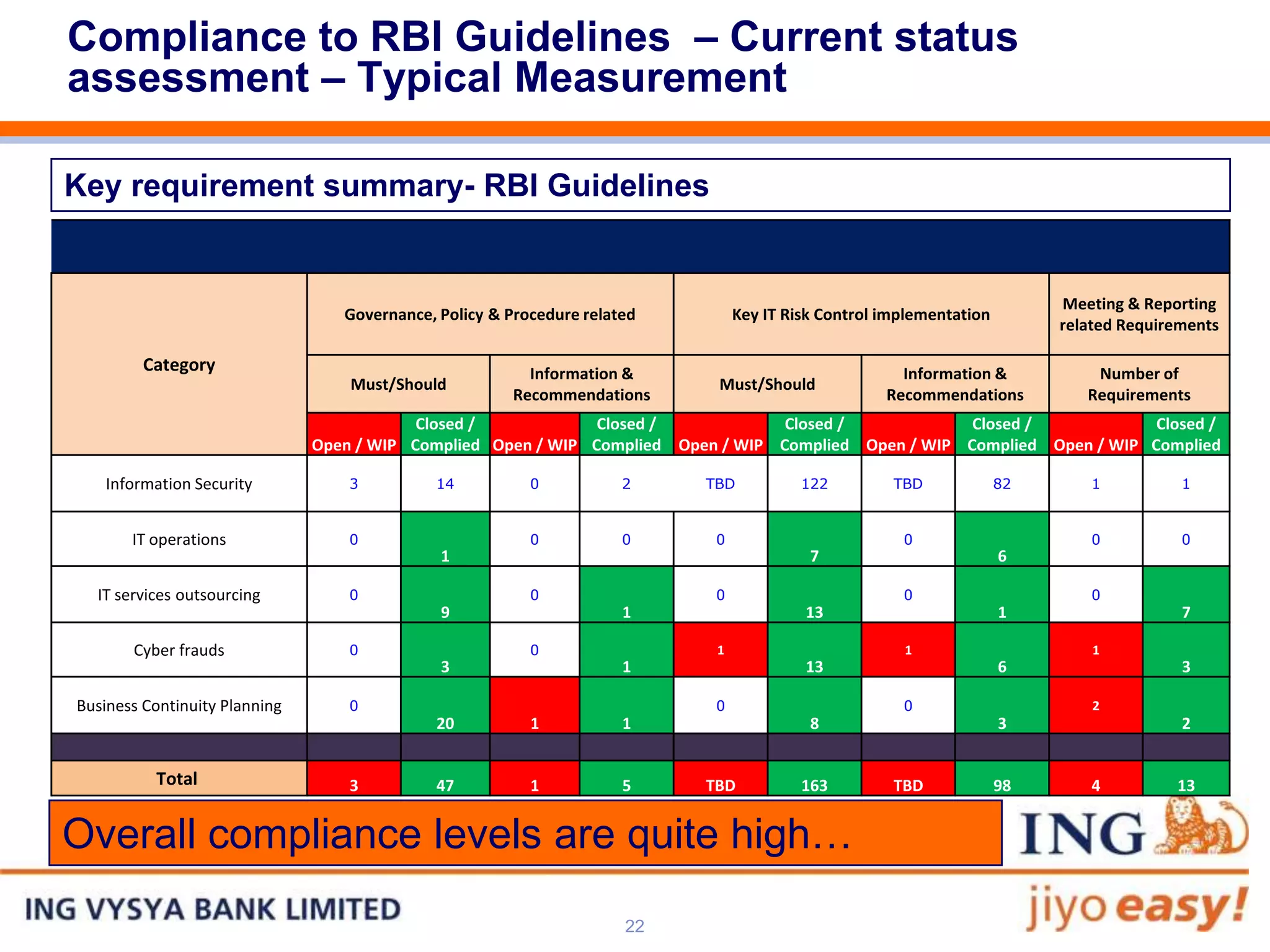

This document outlines a presentation given to the Reserve Bank of India on technology management in banks. The presentation covers the history of banking in India, the current technology landscape, and enterprise architecture management. It then discusses typical IT structures in banks including mission, governance, and processes. The presentation is divided into sections on changing business needs, running current infrastructure, and securing the bank. Specific topics covered include business architecture, channels, processors, data infrastructure, infrastructure reference architecture, IT risk controls, and compliance with RBI guidelines.