Downloaded 20 times

![: www.accoca.com

: ankush@accoca.com ; doonacco@gmail.com

: 0135-2741999 ; 09412059974 ; 09410702848

Issuance of Form 16 & 16A TDS Certificate:

CIRCULAR NO. 01/2012 [F.No. 276/34/2011-IT(B)], DATED 9-4-

2012 Notofication 41/2010 dated 31 may 2010

Who and when has to issue Form 16?

Deductor/Employer. Form 16 under sec 192 to be issued

annually (for salaried person)

Who and when has to issue Form 16A?

Deductor. Form 16A to be issued quarterly (other than

salaried

How to get Form 16A after Notification dt 9th Apr 12?

The deductor, issuing TDS certificate in Form 16A by

downloading from the TRACES website

How Form 16A has to authenticate?

Shall be authenticated by DIGITAL or MANNUAL signature.](https://image.slidesharecdn.com/tds13-14highlights-140618032709-phpapp01/85/Tds-13-14-highlights-8-320.jpg)

![: www.accoca.com

: ankush@accoca.com ; doonacco@gmail.com

: 0135-2741999 ; 09412059974 ; 09410702848

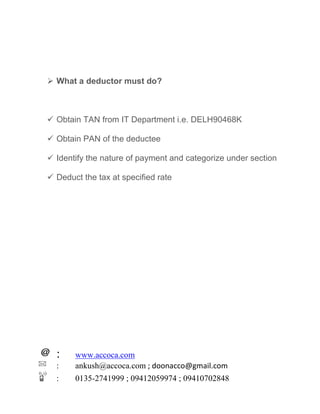

TDS Chart:

Important: Please note that the TDS Rates for FY 2013-14 remains same as of FY 2012-13,

only few changes were made which you can find after the table

SectionParticulars TDS Threshold Limit

192 Salary Normal

Rate

As per normal computation of income

193 Interest on Specified Securities 10% Rs. 5,000 [Rs. 2,500 upto 30-6-2012] in

case of Listed Debentures payable to

resident individual or a Hindu undivided

family, by a company in which public are

substantially interestedRs. 10,000 in

case of 8% Savings (Taxable) Bonds,

2003,

Rs. 10,000 in case of 6½ per cent Gold

Bonds, 1977, or 7 per cent Gold Bonds,

1980, where the Bonds are held by an

individual not being a non-resident, and

the holder thereof makes a declaration

in writing before the person responsible

for paying the interest that the total

nominal value of the 6½ per cent Gold

Bonds, 1977, or, as the case may be, the

7 per cent Gold Bonds, 1980

No TDS on certain specified securities –

see section 193

193 Interest other Securities 10%

194 Dividend (Deemed) 10% Rs. 2,500 where shareholder is an

individual

194 Dividend (Other) Nil

194A Interest other than interest on security 10% (a) Rs. 10,000/- where the payer is a

banking company

(b) Rs. 10,000/- where the payer is a co-](https://image.slidesharecdn.com/tds13-14highlights-140618032709-phpapp01/85/Tds-13-14-highlights-13-320.jpg)

![: www.accoca.com

: ankush@accoca.com ; doonacco@gmail.com

: 0135-2741999 ; 09412059974 ; 09410702848

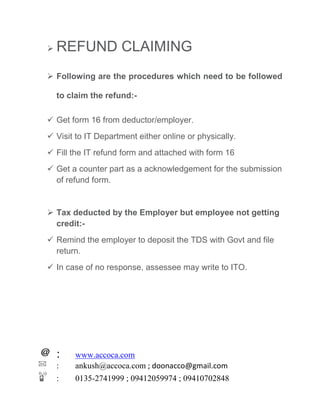

operative society engaged in carrying on

the business of banking;

(c) Rs. 10,000/- on any deposit with post

office under any scheme framed by the

Central Government and notified by it in

this behalf; and

(d) Rs. 5,000/- in any other case

194B Winning from Lotteries 30% Rs. 10,000

194BB Winning for horse race 30% Rs. 5,000

194C Payment to Individuals and HUF 1% Rs. 30,000 per single contract or Rs.

75,000 in aggregate during the Finance

Year

No TDS on GTA if PAN number of the

GTA is available

194C Payment to other contractors 2% Rs. 30,000 per single contract or Rs.

75,000 in aggregate during the Finance

Year

No TDS on GTA if PAN number of the

GTA is available

194D Insurance Commission 10% Rs. 20,000

194E Payment to a non-resident foreign

citizen sportsman or nonresident

sports association [upto 30.6.2012]

10% -

Payment to a non-resident foreign

citizen sportsman / entertainer or non

resident sports association [w.e.f.

1.7.2012]

20% -

194EE Payment for National Saving Scheme,

1987

20% Rs. 2500](https://image.slidesharecdn.com/tds13-14highlights-140618032709-phpapp01/85/Tds-13-14-highlights-14-320.jpg)

![: www.accoca.com

: ankush@accoca.com ; doonacco@gmail.com

: 0135-2741999 ; 09412059974 ; 09410702848

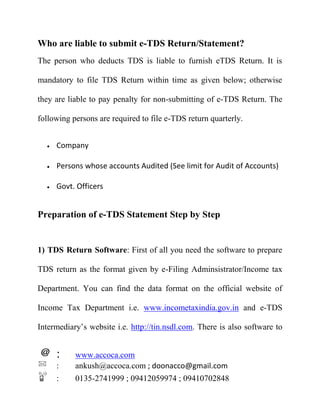

194F Payment for repurchase of units 20% -

194G Commission on sale of lottery ticket 10% Rs. 1,000

194H Commission or Brokerage 10% Rs. 5,000

194I Rent on land, building or furniture 10% Rs. 1,80,000

194IA TDS on transfer of immovable

property other than agriculture land

(w.e.f. 01.06.13)

1% Rs. 50,00,000

194I Rent on plant, machinery or

equipment

2% Rs. 1,80,000

194J Fees for Professional/Technical

services

10% Rs. 30,000

Remuneration to a director w.e.f.

1.7.2012

10%

194LA Compensation to a resident on

acquisition of certain immovable

property

10% Rs. 2,00,000

[Rs. 1,00,000 upto 30.6.2012]

Applicable TDS Rates are same as were in force for F.Y. 2013-13 except the changes

specified below.

I. Rates for deduction of income-tax at source during the financial year 2013-14 from

certain incomes other than “Salaries”.

The rates for deduction of income-tax at source during the financial year 2013-14 from certain

incomes other than “Salaries” have been specified in Part II of the First Schedule to the Bill. The

rates for all the categories of persons will remain the same as those specified in Part II of the

First Schedule to the Finance Act, 2012, for the purposes of deduction of income-tax at source

during the financial year 2012-13, except that in case of certain payments made to a non-resident

(other than a company) or a foreign company, in the nature of income by way of royalty or fees

for technical services, the rate shall be twenty-five percent of such income.](https://image.slidesharecdn.com/tds13-14highlights-140618032709-phpapp01/85/Tds-13-14-highlights-15-320.jpg)

This document provides information about tax deducted at source (TDS) in India, including procedures for deducting, depositing, filing returns, and claiming refunds. It discusses who is responsible for deducting TDS and key details like rates, thresholds, due dates, and forms used. The summary also outlines the steps for preparing an electronic (e-TDS) return, including using TDS return software, applicable filing deadlines, and documents required.

![Tds provisions [income tax act, 1961]](https://cdn.slidesharecdn.com/ss_thumbnails/tdsprovisionsincometaxact1961-140709044039-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)