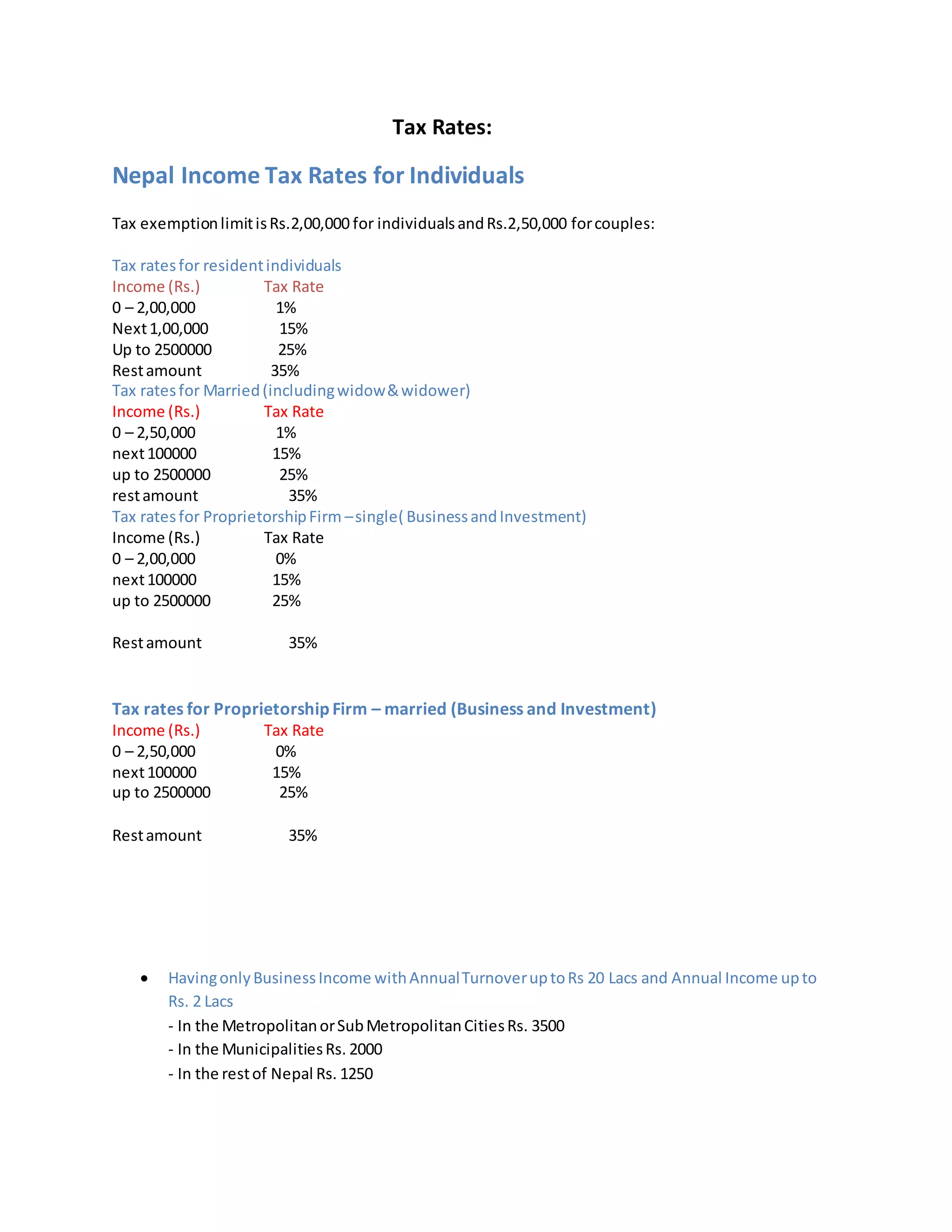

This document outlines income tax rates and deductions for individuals and corporations in Nepal. For individuals, tax rates range from 1% to 35% depending on income level. Married couples and disabled individuals receive higher exemption limits. Tax deductions are provided for life insurance premiums, foreign employment allowances, and remote area benefits. Corporate tax rates range from 20-30% for most entities and industries, with tax holidays and rebates provided for industries establishing in special economic zones or creating many jobs.

![from industries established in special economic zone: 50% of applicable rate

- Industries established in remote areas: 0% for 10 years

- Information Technology based industries established at prescribed Information Technology

park: 75% of Normal Rate

- Licensed Industries engaged in production and distribution of electricity, if the production and

distribution is completed by the end of Chaitra 2075: 100% exemption for first 7 years, 50% for

next 3 years.

Tax ConcessionandRebates

- 10 Years Tax Holidayfromdate of operationand50% Tax Rebate thereaftertoindustriesestablishedin

Special EconomicZone (SEZ) of HimalayanDistrictsandotherprescribedHillyDistrict.

- 5 YearsTax Holidayfromdate of operationand50% Tax Rebate thereaftertoindustriesestablished in

otherSpecial EconomicZone (SEZ).

- 100% Rebate forfirst5 Yearsfrom date of operationandthen50% Rebate fornext3 Yearson dividend

distributedbyindustriesestablishedinSpecial EconomicZone (SEZ).

- 50% Rebate on Income Tax on income fromForeignTechnologyorManagementConsultancyor

Royaltyearnedbyforeigninvestorsof industryestablishedinSEZ.

- 10 Years Tax Holidayfromdate of operationtoindustriesestablishedinremote areas.

- 25% Tax Rebate to IT IndustriesestablishedinprescribedInformationTechnologyPark.

- Entitieshavinglicense forElectricitygeneration,transmission&distribution,if commencesgeneration

/ generation&transmission/generation&distribution/generation,transmission&distributionof

Hydro-electricitycommercial mannerbyChaitraend,2075; suchentitiesshall have Tax Holidayfora

periodof first7 Years and 50% Tax Rebate thereafterfor3 Years,from date of such commencementof

generation,transmission&distribution.Suchfacilitiesshall alsobe applicableforElectricitygenerated

fromSolar/Wind/OrganicMaterials.

However,entitiesalreadyhavingstartedcommercial productionof electricitybefore Shrawan01,2066

shall be eligible forfacilityasprevalentatthe time of obtaininglicense

- 50%, 30% & 25% Rebate onIncome Tax for10 Yearsincludingthe yearof operationtoSpecial

IndustriesoperatinginHighlyUndeveloped,Undeveloped&Under-developedareasrespectively.

- 10 % Rebate onIncome Tax to Special IndustriesandITIndustrieswhichprovide directemploymentto

300 Nepalesenationalsthroughoutthe year.[Earlier,itwas500 Nepalese].

- 20 % Rebate onIncome Tax to Special Industrieswhichprovide directemploymentto1200 Nepalese

nationalsthroughoutthe year.

- 20 % Rebate onIncome Tax to Special Industrieswhichprovide directemploymentto100 Nepalese

nationalsincluding33percentwomen,dalits(the downtrodden) orthe handicapped,throughoutthe

year](https://image.slidesharecdn.com/taxationinnepalbook-161212081148/85/Taxation-in-nepal-book-5-320.jpg)

![Tax guide-2012[1]](https://cdn.slidesharecdn.com/ss_thumbnails/tax-guide-20121-130314215142-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)