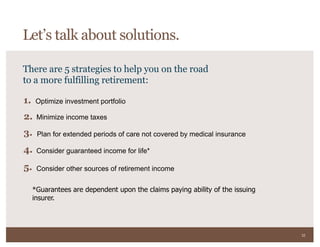

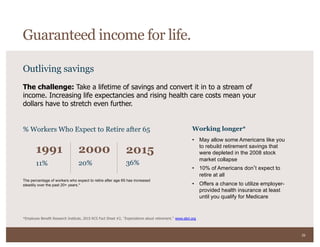

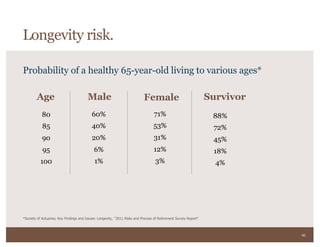

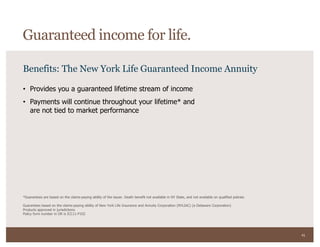

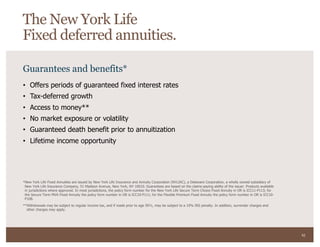

This document discusses strategies for navigating retirement challenges and outlines 5 strategies to help achieve a more fulfilling retirement: 1) Optimize investment portfolio, 2) Minimize income taxes, 3) Plan for extended health care costs, 4) Consider guaranteed income products for life, and 5) Consider other sources of retirement income. It addresses common retirement challenges such as inflation, outliving savings, taxes, expenses, and managing expectations.

![Slirp 4 9 09 Final[1]](https://cdn.slidesharecdn.com/ss_thumbnails/slirp4909final1-12667828759198-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)