Download to read offline

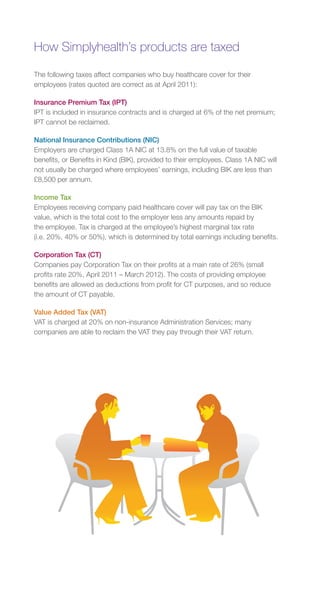

This document discusses the various taxation implications of company-paid healthcare in the UK, including: - Insurance Premium Tax of 6% is included in insurance premiums and cannot be reclaimed. - Employers pay Class 1A National Insurance Contributions of 13.8% on the cost of employees' healthcare benefits. - Employees pay income tax on the value of their benefits at their marginal tax rate of 20%, 40%, or 50%. - Companies can deduct the costs of providing employee benefits from profits for corporation tax purposes. It provides examples of the tax treatment for private medical insurance and health cash plans.

![Ab 09 Paye Update May 11[1]](https://cdn.slidesharecdn.com/ss_thumbnails/ab09payeupdatemay111-13201259563118-phpapp01-111101004053-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)

![[ARCHIVE] Aviva Working Lives report](https://cdn.slidesharecdn.com/ss_thumbnails/workinglives-120502024926-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)

![[ARCHIVE] Infographic - Aviva Times of Our Lives Report - Mind the insurance gap](https://cdn.slidesharecdn.com/ss_thumbnails/infographictimesofourlives-121025055726-phpapp02-thumbnail.jpg?width=640&height=640&fit=bounds)

![How To Survive And Thrive In The Era Of Health Reform[1]](https://cdn.slidesharecdn.com/ss_thumbnails/howtosurviveandthriveintheeraofhealthreform1-1344556089601-phpapp01-120809184958-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)