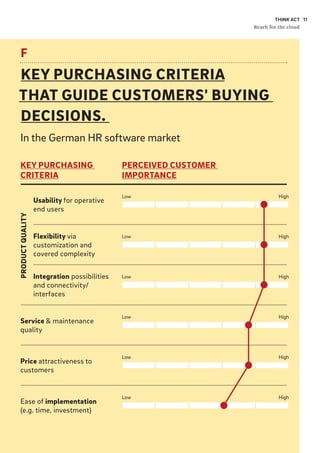

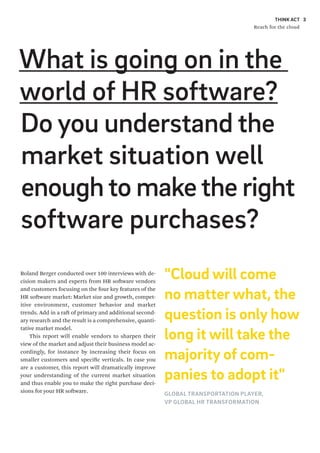

The German HR software market reached about EUR 1.3 billion in 2015 and is expected to grow to EUR 1.7 billion by 2020, driven by trends like the transition to cloud-based solutions. The market consists of seven segments, with administrative segments like employee data administration currently larger but growing slower than strategic segments like recruiting and talent management. A major trend is the strong expected growth of cloud-based solutions, from a 13% market share in 2015 to an estimated 86% by 2020. Growth is also supported by increasing demand from small and medium-sized enterprises.

![THINK ACT

Reach for the cloud

6

ABOVE AVERAGE GROWTH RATE TO BE

EXPECTED

German HCM software market 2014-20 [EUR bn]

A MAJOR GROWTH DRIVER IS CLOUD BASED

HR SOFTWARE

German HCM software market by deployment type,

2014-20 [EUR bn]

SEVEN SEGMENTS MAKE UP THE HR MARKET

German HCM software market by product segment,

2015 [%]

DEMAND FOR NEW SOFTWARE IS ESPECIALLY

STRONG IN THE GERMAN "MITTELSTAND"

German HCM software market by customer segment,

2014-20 [EUR bn]

A

C

B

D

2014

2014

1.2

1.2

0.3

0.3

0.6

0.9 1.0

1.1

2015

2015

1.3

1.3

2020

2020

24%

Employee data

administration

23%

Workforce

management

17%

Recruiting

13%

Learning &

development

11%

Performance &

talent management

4%

Employee collaboration

& engagement

9%

Payroll, compensation

& benefits

1.7

1.7

CAGR

+5%

+11%

+86%

Source: Roland BergerHCM = Human Capital Management

Administrative segments Strategic segments

Cloud On-premise

2014

1.2

0.4

0.4

0.7

0.8

0.9

1.0

2015

1.3

2020

1.7

+16%

+55%

SME Large](https://image.slidesharecdn.com/653b514e-3e9f-4362-bb33-a6ed0ff8670f-160709140458/85/TAB_HR_Software_Market_final-6-320.jpg)