Download to read offline

![3

Add to the list flooding, tornados, and other effects of climate change, not to mention

political unrest. Any one of these events can send major sources of supply and

demand into turmoil. Consider the price and supply volatility of raw materials, fuel,

and commodities in the wake of a major natural disaster, and how much any one

element affects the others. Howells elaborates: “Natural disasters and extreme weather

have always been a part of life. However, in today’s global economy, the impact is

exaggerated by the interdependence of our global society. If one link in the supply chain

is broken, it can have a huge ripple effect.”

In short, the more we’re connected, the more disruption in any area broadcasts

its effects throughout the world economy. Take into account multiplying levels of

complexity, and it’s clear that companies destined to survive and thrive are those

that can react quickly and flexibly across the board. Whether facing economic,

environmental, supply, or demand changes, businesses are looking for solutions that

enable responsive planning, support collaboration, and mitigate risk across supply

chain networks.

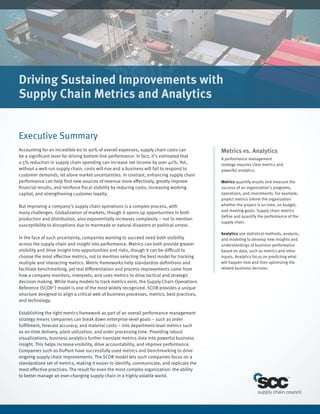

Using Metrics to Drive Performance

To respond rapidly to disruptions, supply chain managers need both flexibility and

comprehensive visibility into supply chain performance. According to Rich Sherman, a

member of the founding team for Supply Chain Council (SCC) and Director at the Council

of Supply Chain Management Professionals (CSCMP), “Whether the economy is trending

up and growth and expansions are the norm – or down and cutbacks are needed –

organizations must be able to adapt the supply chain to support their objectives.”

Continues Sherman, “For organizations desiring this level of insight and flexibility,

supply chain analytics are critical.” One valuable analytical model is the Supply Chain

Operations Reference (SCOR) from SCC, an independent, nonprofit global corporation

working to advance the state of the art in supply chain management systems

and practices.

The SCOR Model

The SCOR model provides a unique framework that links business processes, metrics,

best practices, and technology into a unified structure designed to improve the

effectiveness of supply chain management. This includes collaborating with partners to

identify and implement supply chain improvements.

SCOR helps manage common problems through a standardized set of language, metrics,

and business practices that accelerate change and improve performance. Applying SCOR

streamlines communication while dramatically improving the overall effectiveness of

daily management and targeted improvement initiatives; gains are measured using the

organization’s SCORindex. “We’ve seen drastic improvements in companies that use

SCOR; [they] are consistent top performers in their industries,” says Sherman.](https://image.slidesharecdn.com/3dbebcb3-399b-404c-bd19-eaf5980a6597-151124011140-lva1-app6892/85/Sustained-Performance-3-320.jpg)

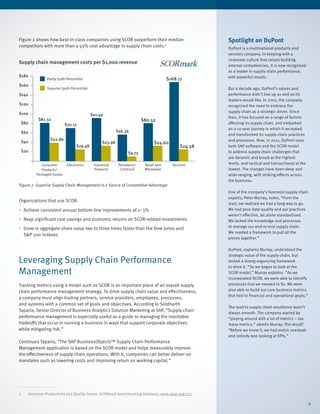

This document discusses the importance of supply chain metrics and analytics for managing supply chain complexity and risks. It summarizes that effective metrics and analytics can provide visibility across the supply chain and insights to drive performance improvements. The Supply Chain Operations Reference (SCOR) model is highlighted as an effective framework for standardizing metrics and enabling benchmarking. The document also provides an example of how DuPont has successfully used metrics and benchmarking based on the SCOR model to transform its supply chain and drive ongoing improvements.