Download to read offline

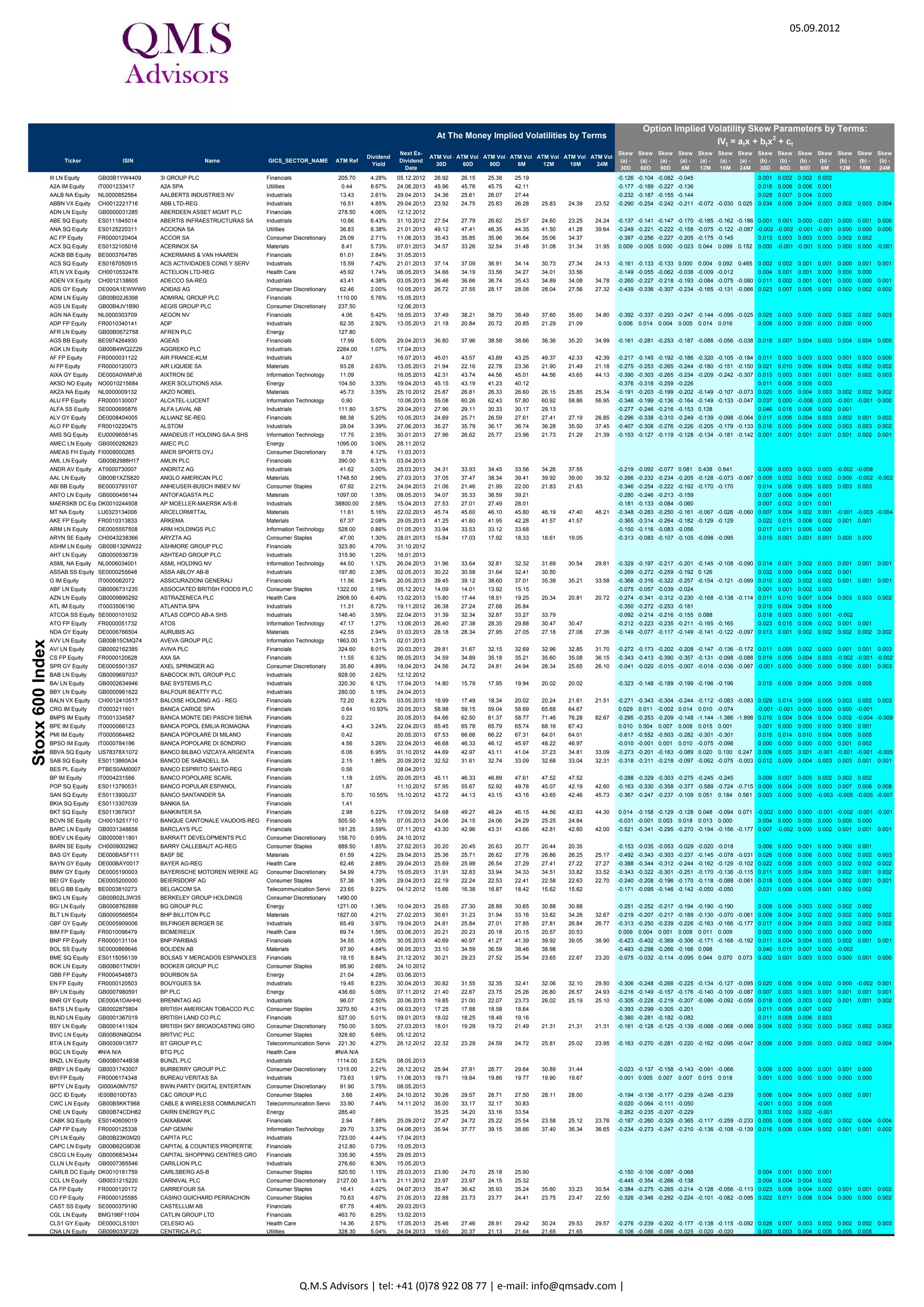

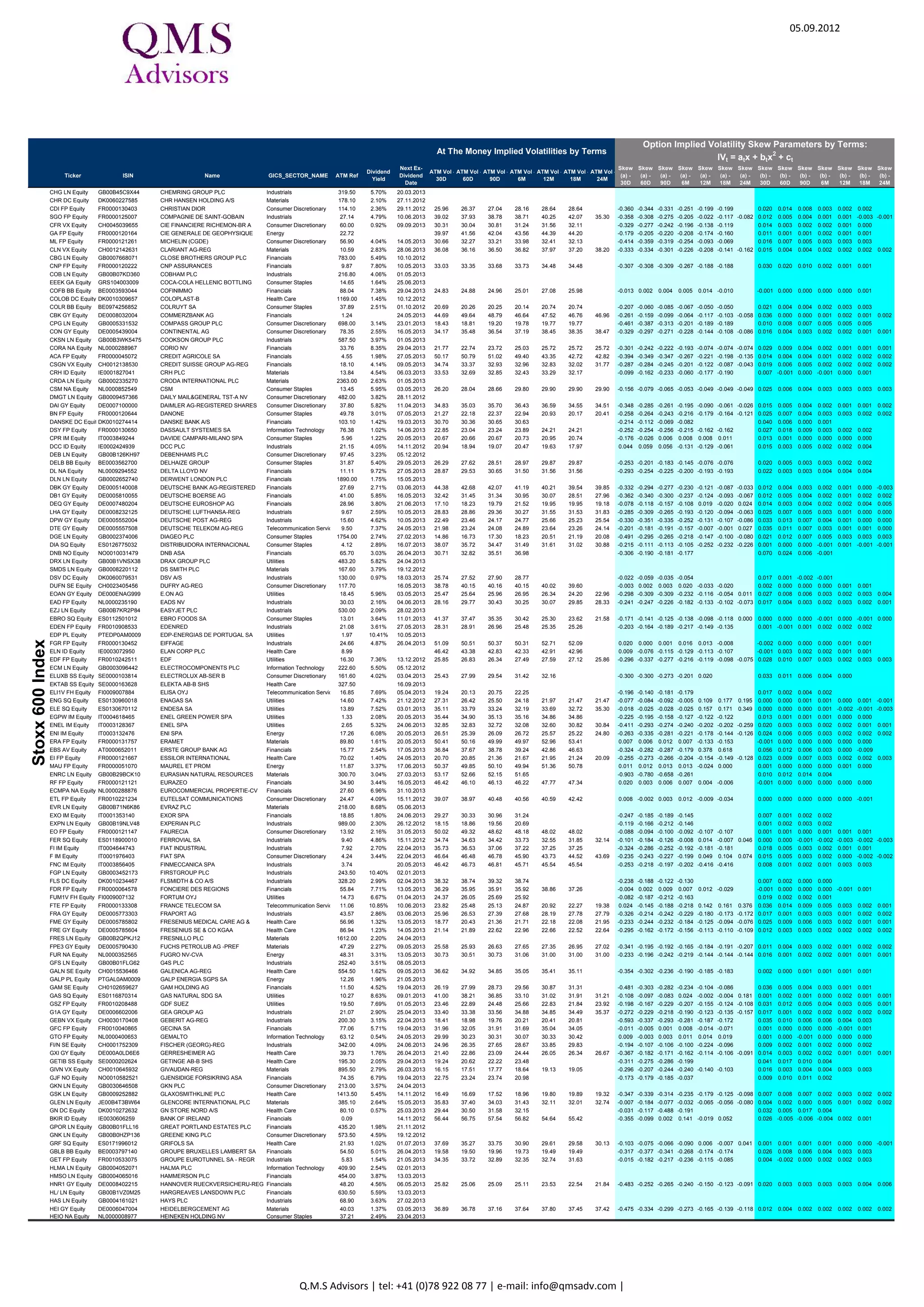

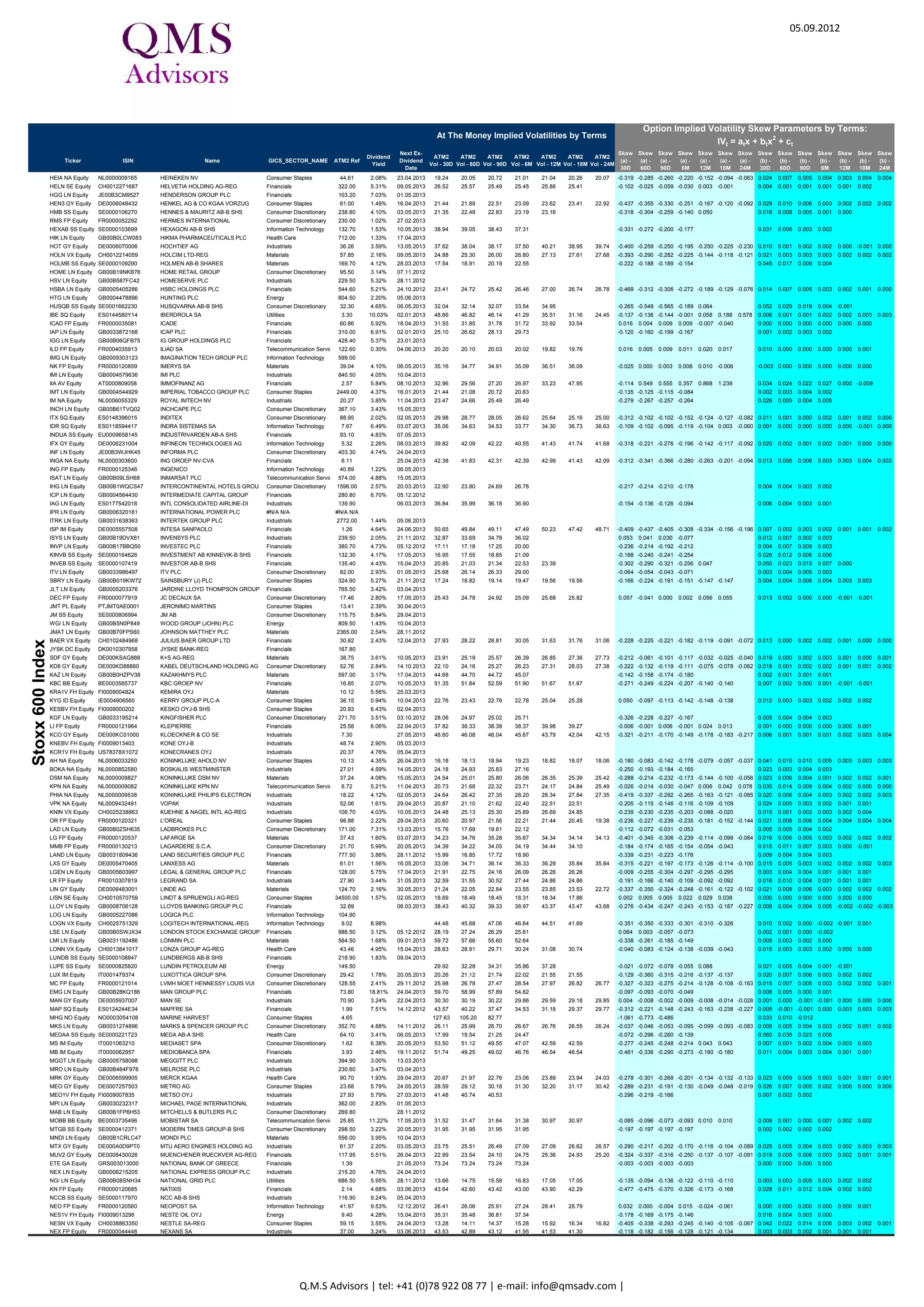

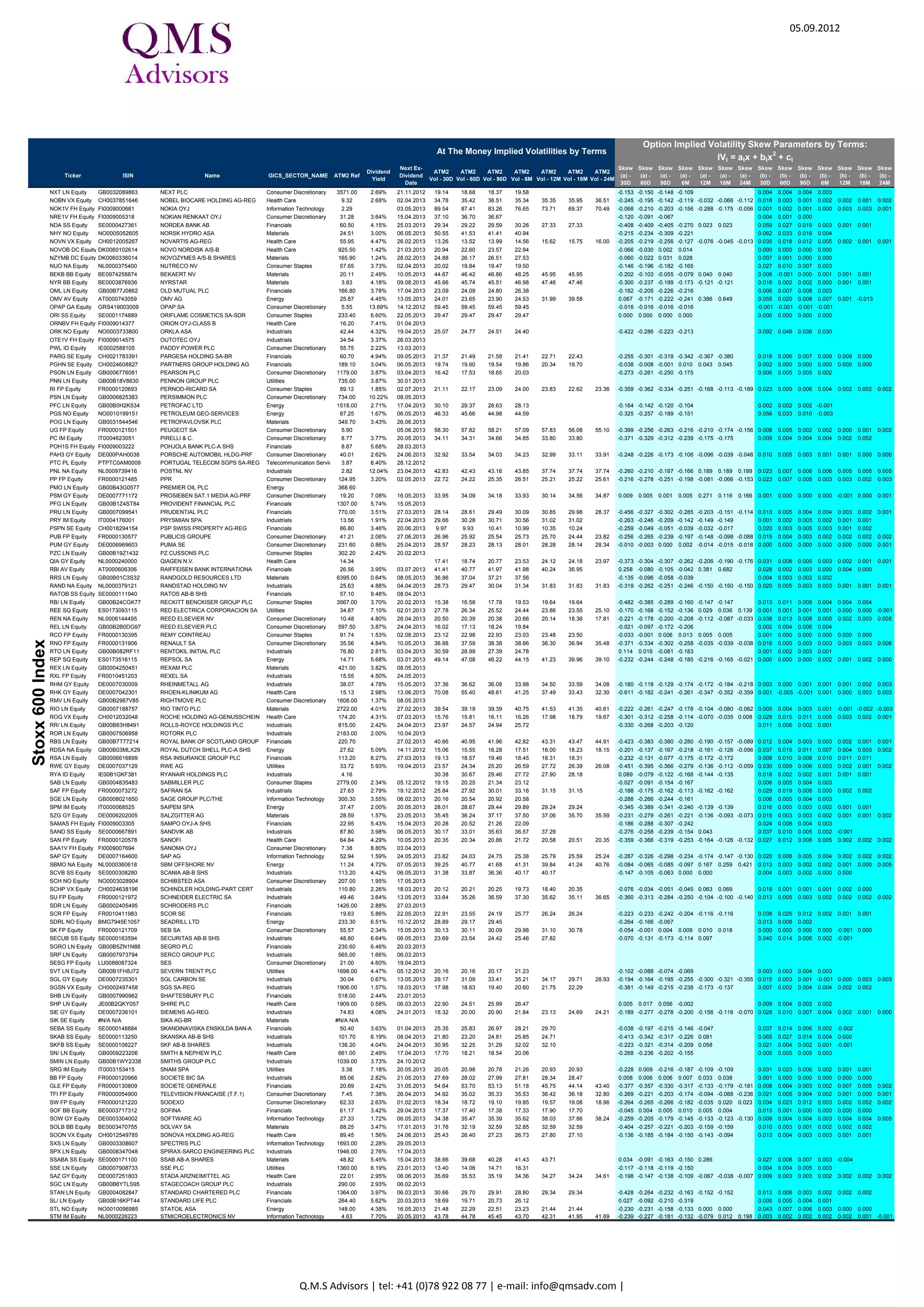

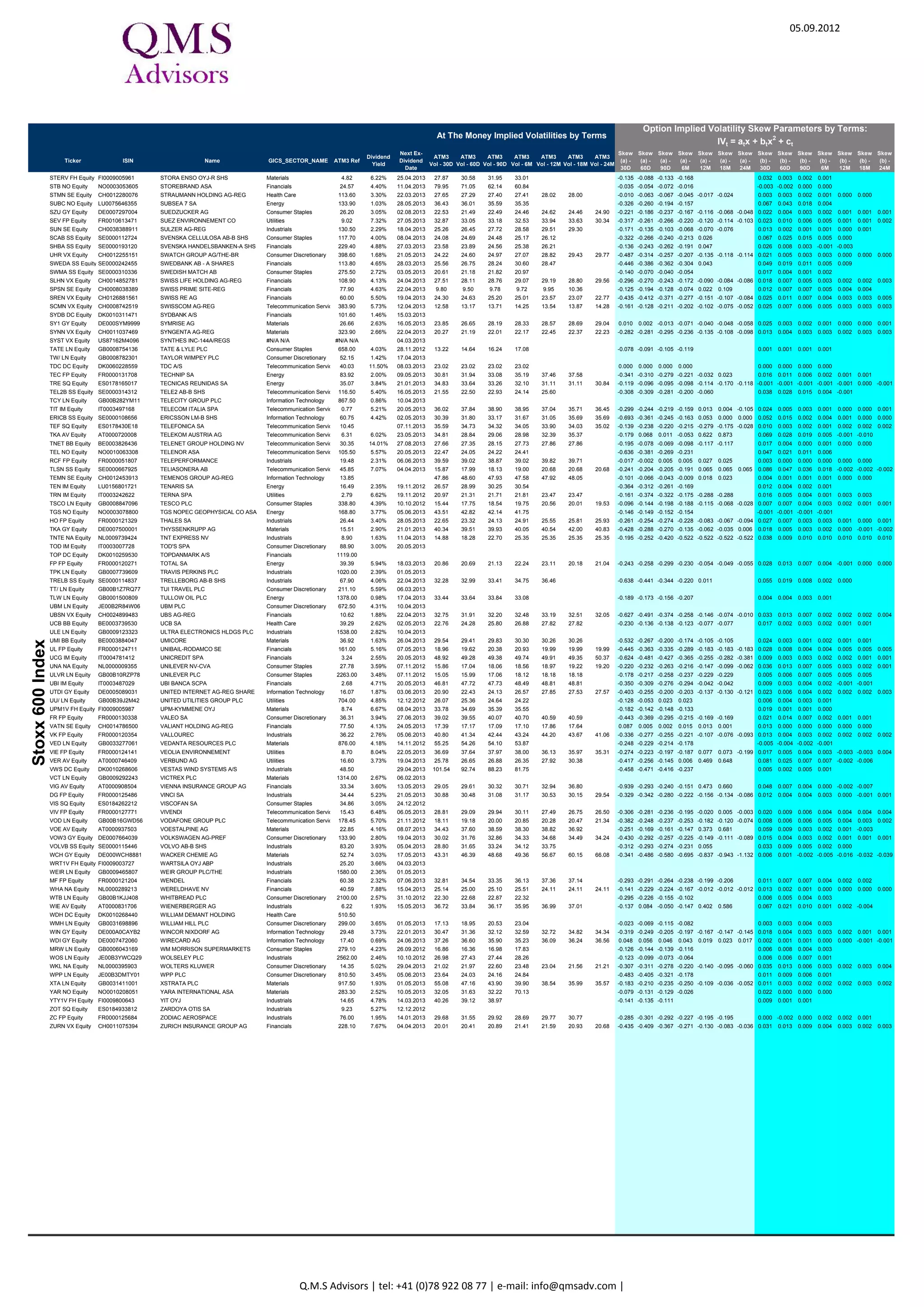

The document contains implied volatility skew parameters for the options of 19 stocks across various terms from 30 days to 24 months. For each stock, it lists the at-the-money implied volatilities, skew coefficients that model the implied volatility smile, and ex-dividend dates. The stocks span sectors like consumer staples, healthcare, energy, and financials.