Small Business Lending Index August 2015

•

2 likes•336 views

Big banks decreased 22.3% of small business loan requests in August 2015, down from 22.4% in July, marking the tenth consecutive month, small banks have denied more than half of their loan requests.

Recommended

More Related Content

What's hot

What's hot (20)

Viewers also liked

Viewers also liked (20)

Similar to Small Business Lending Index August 2015

Similar to Small Business Lending Index August 2015 (20)

More from Biz2Credit

More from Biz2Credit (20)

Small Business Lending Index August 2015

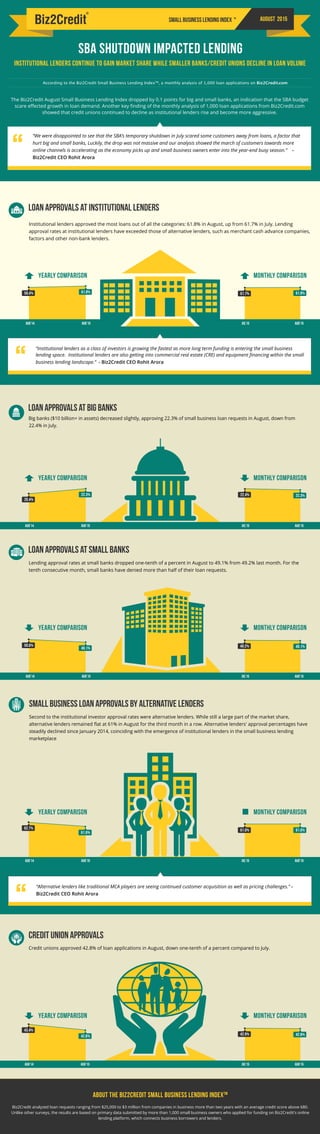

- 1. 61.8%61.7% SBA Shutdown Impacted Lending Institutional Lenders Continue to Gain Market Share While Smaller Banks/Credit Unions Decline in Loan Volume August 2015Small Business Lending Index According to the Biz2Credit Small Business Lending IndexTM , a monthly analysis of 1,000 loan applications on Biz2Credit.com The Biz2Credit August Small Business Lending Index dropped by 0.1 points for big and small banks, an indication that the SBA budget scare effected growth in loan demand. Another key finding of the monthly analysis of 1,000 loan applications from Biz2Credit.com showed that credit unions continued to decline as institutional lenders rise and become more aggressive. About the Biz2Credit Small Business Lending IndexTM Biz2Credit analyzed loan requests ranging from $25,000 to $3 million from companies in business more than two years with an average credit score above 680. Unlike other surveys, the results are based on primary data submitted by more than 1,000 small business owners who applied for funding on Biz2Credit's online lending platform, which connects business borrowers and lenders. TM “We were disappointed to see that the SBA’s temporary shutdown in July scared some customers away from loans, a factor that hurt big and small banks, Luckily, the drop was not massive and our analysis showed the march of customers towards more online channels is accelerating as the economy picks up and small business owners enter into the year-end busy season.” - Biz2Credit CEO Rohit Arora “ Small business loan approvals by Alternative lenders Second to the institutional investor approval rates were alternative lenders. While still a large part of the market share, alternative lenders remained flat at 61% in August for the third month in a row. Alternative lenders' approval percentages have steadily declined since January 2014, coinciding with the emergence of institutional lenders in the small business lending marketplace Credit union approvals Credit unions approved 42.8% of loan applications in August, down one-tenth of a percent compared to July. Loan Approvals at Small banks Lending approval rates at small banks dropped one-tenth of a percent in August to 49.1% from 49.2% last month. For the tenth consecutive month, small banks have denied more than half of their loan requests. “Institutional lenders as a class of investors is growing the fastest as more long term funding is entering the small business lending space. Institutional lenders are also getting into commercial real estate (CRE) and equipment financing within the small business lending landscape.” - Biz2Credit CEO Rohit Arora“ Loan Approvals at Institutional Lenders Institutional lenders approved the most loans out of all the categories: 61.8% in August, up from 61.7% in July. Lending approval rates at institutional lenders have exceeded those of alternative lenders, such as merchant cash advance companies, factors and other non-bank lenders. Loan Approvals at Big banks Big banks ($10 billion+ in assets) decreased slightly, approving 22.3% of small business loan requests in August, down from 22.4% in July. yearly comparison 22.3% 20.4% MONTHLY comparison JUL’15 AUG’15 22.3%22.4% yearly comparison 49.1% 50.6% MONTHLY comparison JUL’15 AUG’15 49.1%49.2% yearly comparison 42.8% 43.4% MONTHLY comparison AUG’14 AUG’15 JUL’15 AUG’15 42.8%42.9% yearly comparison 61.0% 62.7% MONTHLY comparison JUL’15 AUG’15 61.0%61.0% yearly comparison 61.8%59.4% MONTHLY comparison “Alternative lenders like traditional MCA players are seeing continued customer acquisition as well as pricing challenges.” - Biz2Credit CEO Rohit Arora “ AUG’15JUl’15 AUG’14 AUG’15 AUG’14 AUG’15 AUG’14 AUG’15 AUG’14 AUG’15