Download as PDF, PPTX

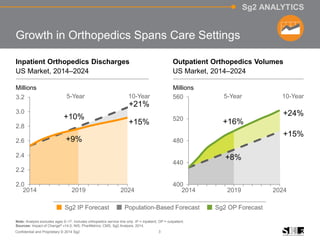

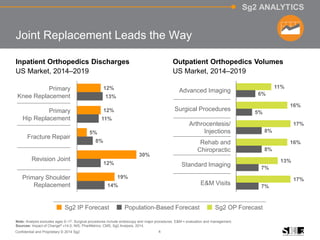

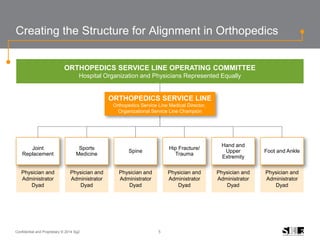

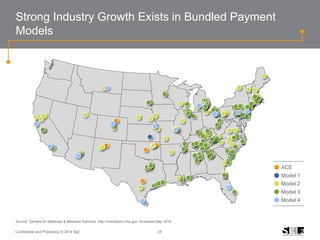

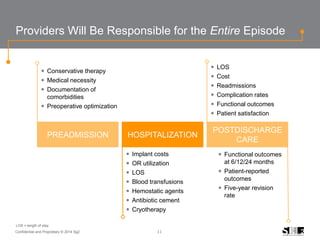

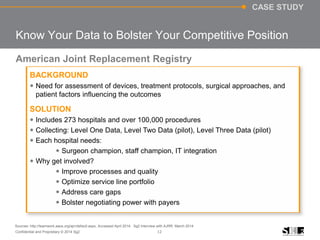

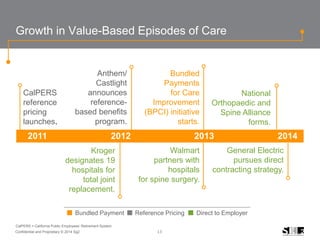

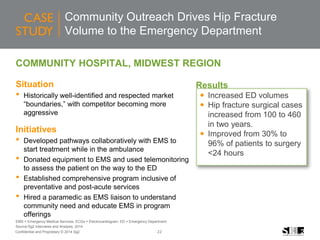

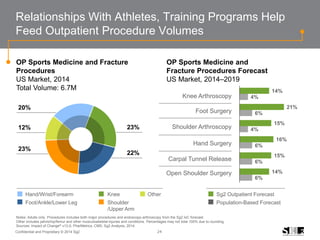

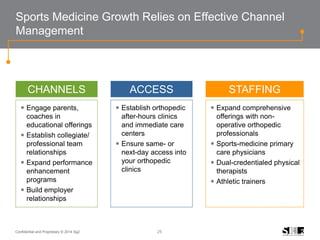

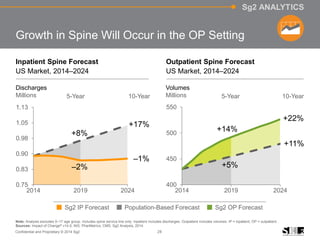

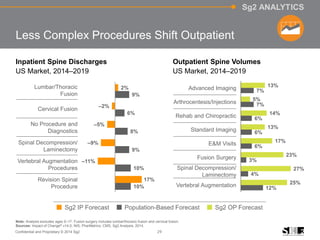

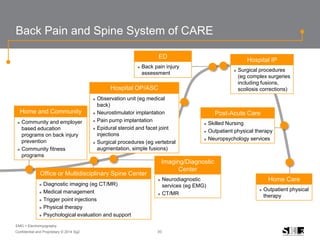

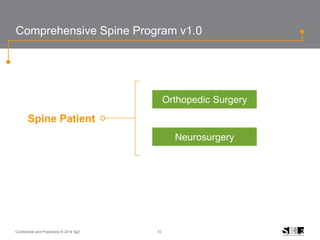

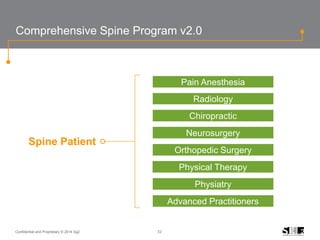

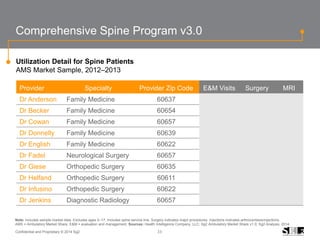

The document outlines trends in orthopedics over the next decade, highlighting significant growth in total joint replacement and outpatient procedures, forecasted to expand by 21% and 24% respectively by 2024. It emphasizes the importance of effective program structures and alignment among healthcare providers to enhance patient care, reduce costs, and improve operational efficiencies. Additionally, it discusses strategies like bundled payment models and robust data management to bolster quality outcomes and competitive positioning in the orthopedics market.

![Hypothalamus short notes on location, function and disorders by Dr. Neha [PT]...](https://cdn.slidesharecdn.com/ss_thumbnails/hypothalamusbydr-260124142231-2b48143d-thumbnail.jpg?width=640&height=640&fit=bounds)

![Cells and Organs of immune system [Autosaved].pptx](https://cdn.slidesharecdn.com/ss_thumbnails/cellsandorgansofimmunesystemautosaved-260123152717-ea0cb261-thumbnail.jpg?width=640&height=640&fit=bounds)