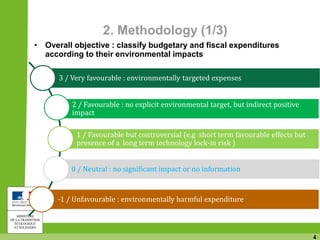

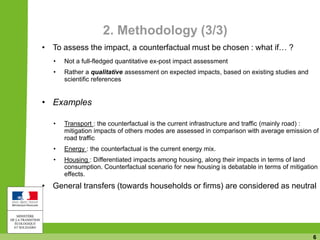

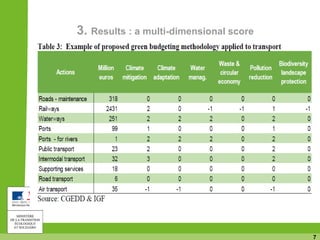

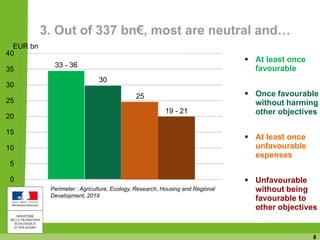

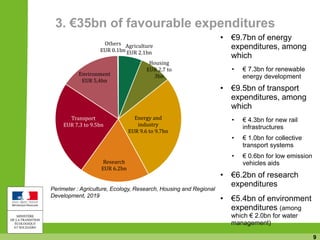

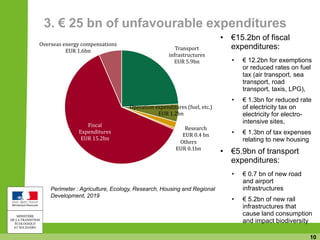

This document summarizes France's efforts in green budgeting. It describes France's commitment to assessing the environmental impacts of its public finances and budget. The methodology classifies budget expenditures on a scale from very favorable to unfavorable based on their impacts on climate change mitigation, adaptation, and other environmental objectives. Results show most expenditures are neutral, while around €35 billion are favorable and €25 billion are unfavorable. Favorable expenditures include investments in renewable energy, rail infrastructure, and research. Unfavorable expenditures include tax exemptions on fuels and some new transport infrastructure projects. Challenges ahead include improving impact assessments, evaluating efficiency of spending, and enabling international comparisons of fiscal expenditures.