Download to read offline

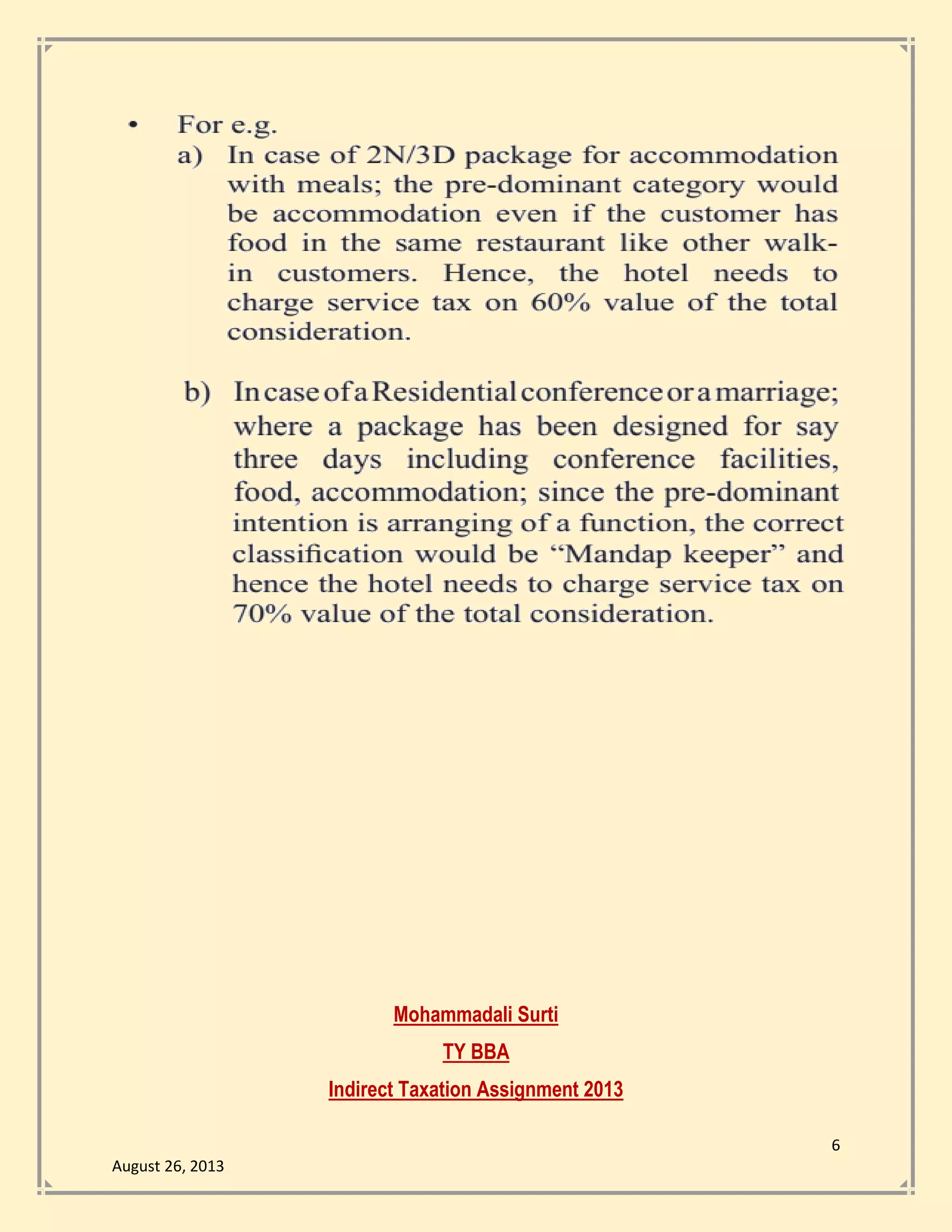

Sumo Hotels sought financial advice from Mr. Kumar regarding service tax obligations and compliance procedures since their business began in August 2013. Mr. Kumar explained that a 60% abatement applies to food sold, requiring service tax to be paid on the remaining 40%, and detailed the registration and payment processes as well as penalties for non-compliance. The hotel must file returns semi-annually, and failure to do so incurs penalties based on arrears.