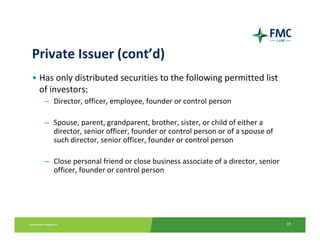

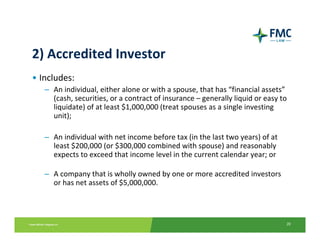

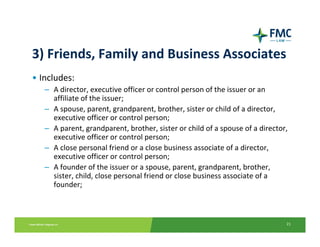

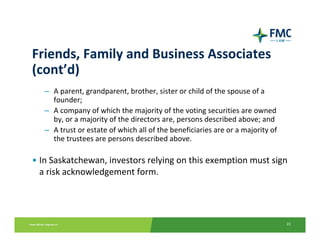

Downloaded 28 times

![Private Issuer

• Means an Issuer:

– That is not a reporting issuer or an investment fund,

– Whose securities (except non‐convertible debt):

• Are subject to transfer restriction contained in the issuers constating

documents or security holders’ agreement; and

• Are owned by not more that 50 people, exclusive of employees and

former employees, and

– Has only distributed designated securities to the permitted list of

investors [i.e. relatives, close friends, accredited investors – s. 2.4(2)].

10](https://image.slidesharecdn.com/securitiesforprivatecompanies-110613134307-phpapp01/85/Securities-for-Private-Companies-10-320.jpg)

The document provides an overview of securities related to private companies, including definitions of various terms such as 'security,' 'private issuer,' and 'accredited investor.' It also outlines private placement exemptions under national instrument 45-106, detailing the responsibilities and requirements for compliance, misrepresentation, and disclosure obligations for non-private issuers. Furthermore, it emphasizes the importance of understanding statutory obligations and preparing for potential transitions to public company practices.