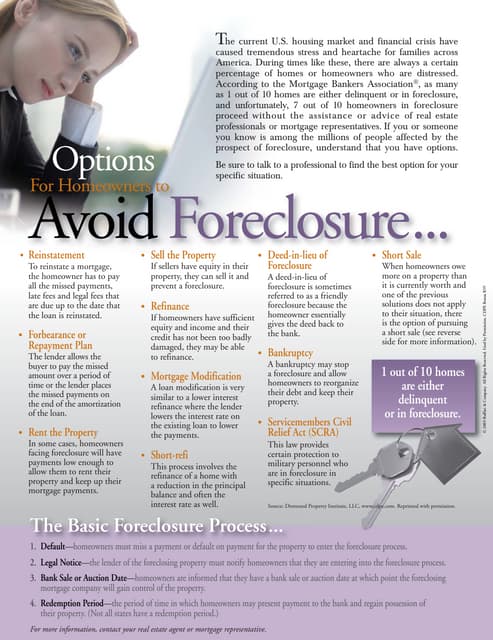

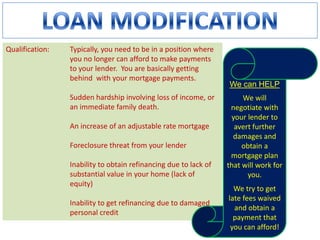

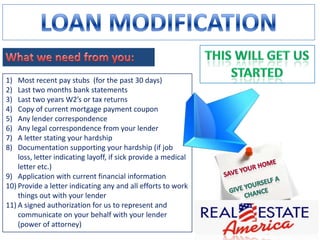

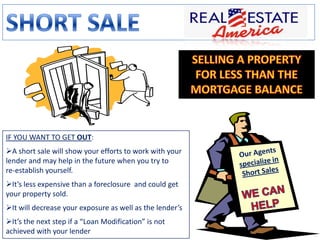

The document outlines the qualifications and documentation needed for individuals facing mortgage payment difficulties, including hardship due to income loss or family death. It provides steps for negotiating with lenders, exploring options like loan modifications and short sales, and emphasizes the importance of demonstrating efforts to resolve the situation to protect future credit. Additionally, it specifies required documents for assistance and the potential benefits of short sales over foreclosures.