1) The document summarizes a presentation about how "Black Swan Trigger Events" influence the development of profitable high growth small firms.

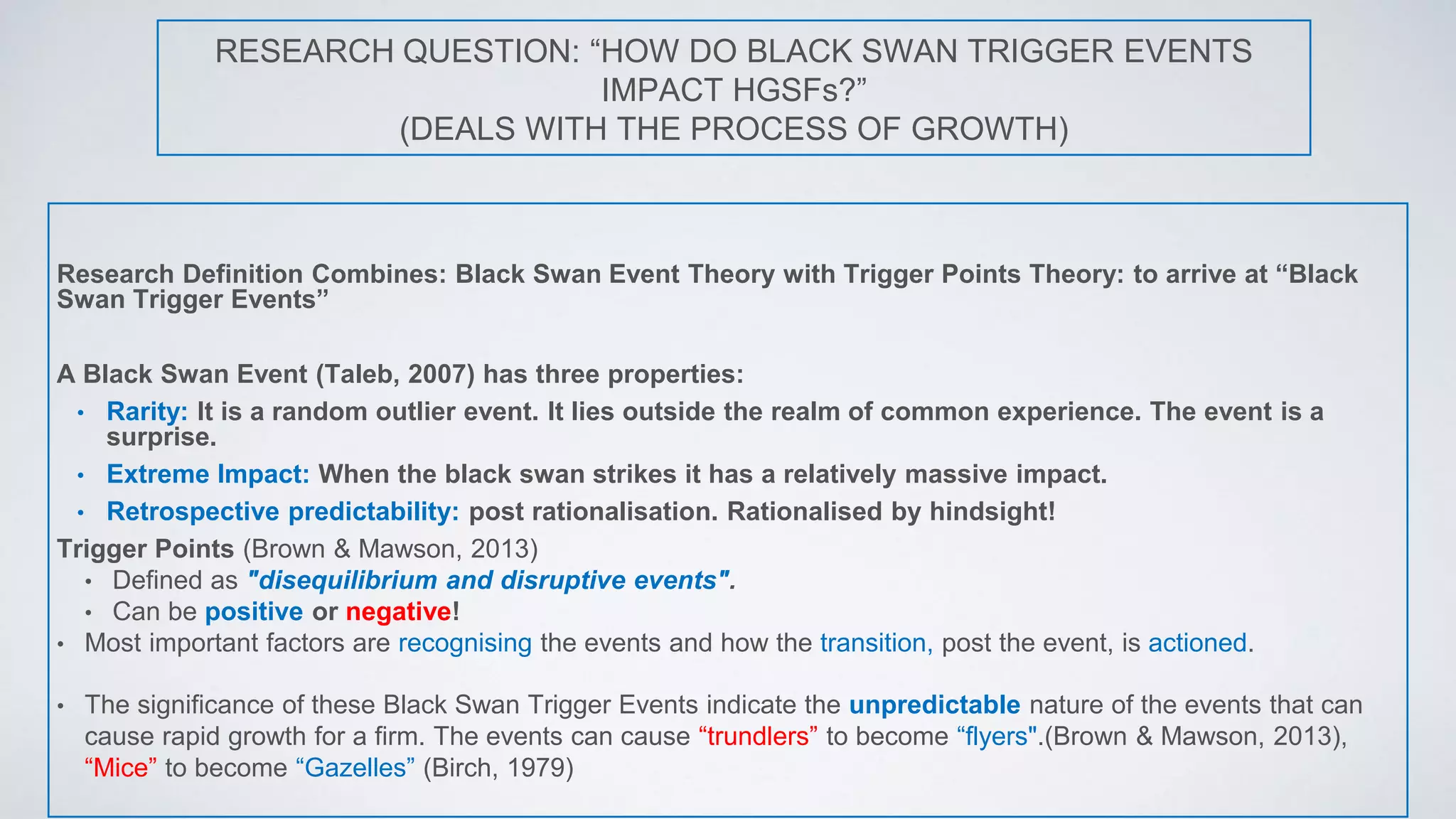

2) It discusses key topics like what a Black Swan Trigger Event and high growth small firm are, examples of large trigger events, and myths about high growth small firms.

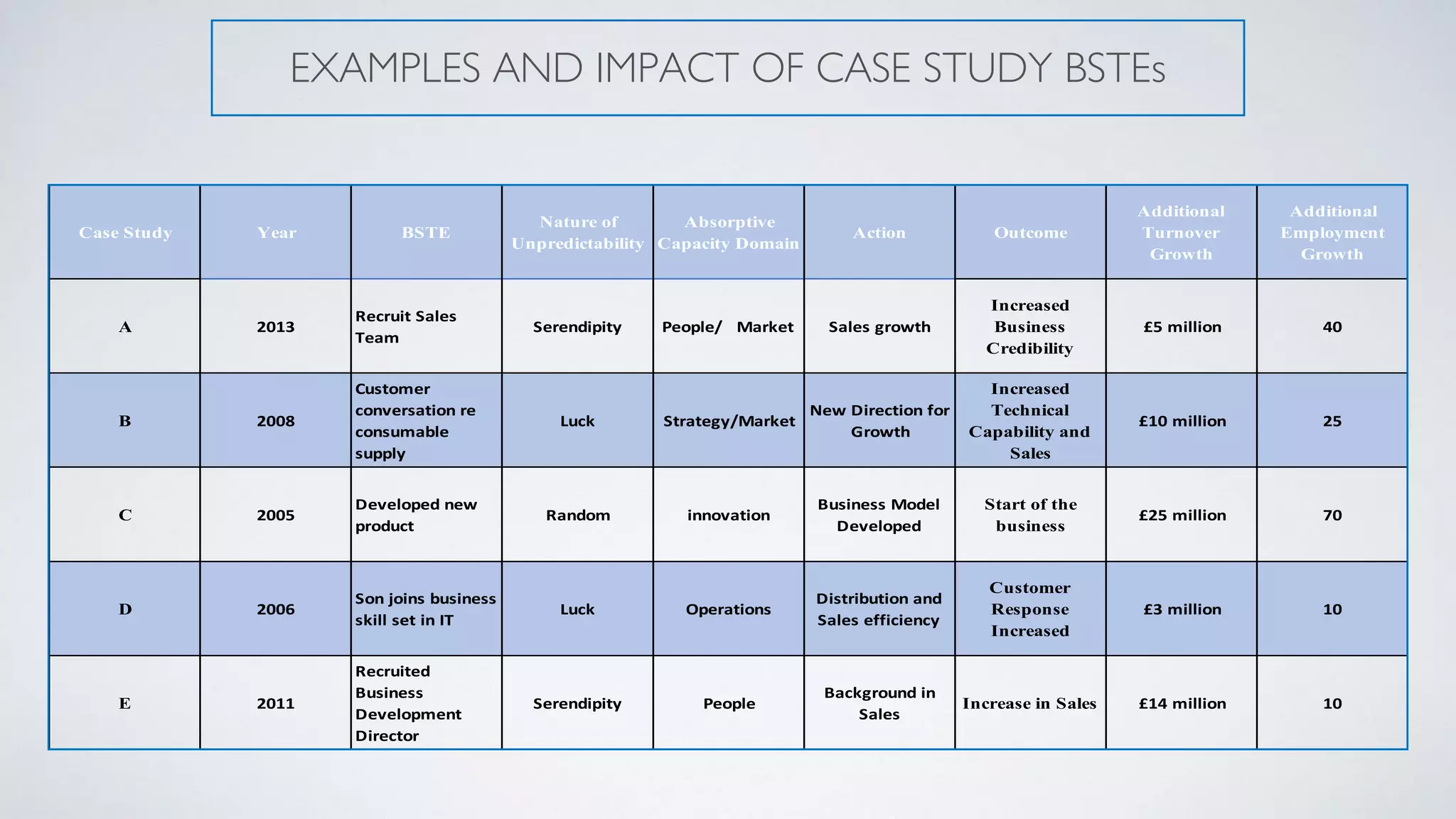

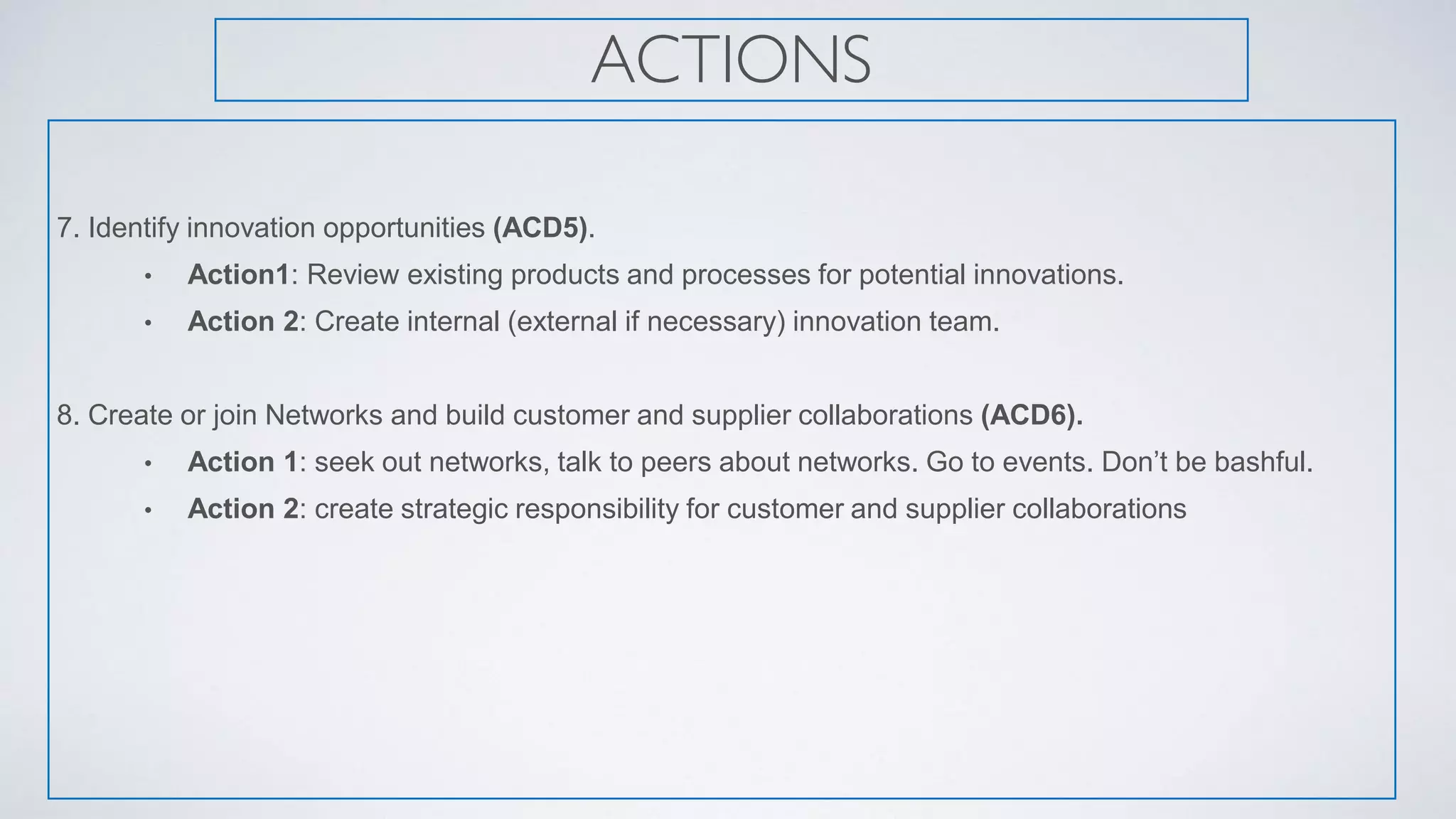

3) The presentation describes the researcher's methodology which involved case studies of 5 North East firms to analyze how they responded to Black Swan Trigger Events through developing absorptive capacity domains.

![Mi ba day_1_session_a_[compatibility_mode]](https://cdn.slidesharecdn.com/ss_thumbnails/mibaday1sessionacompatibilitymode-120311204928-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)