Download as PDF, PPTX

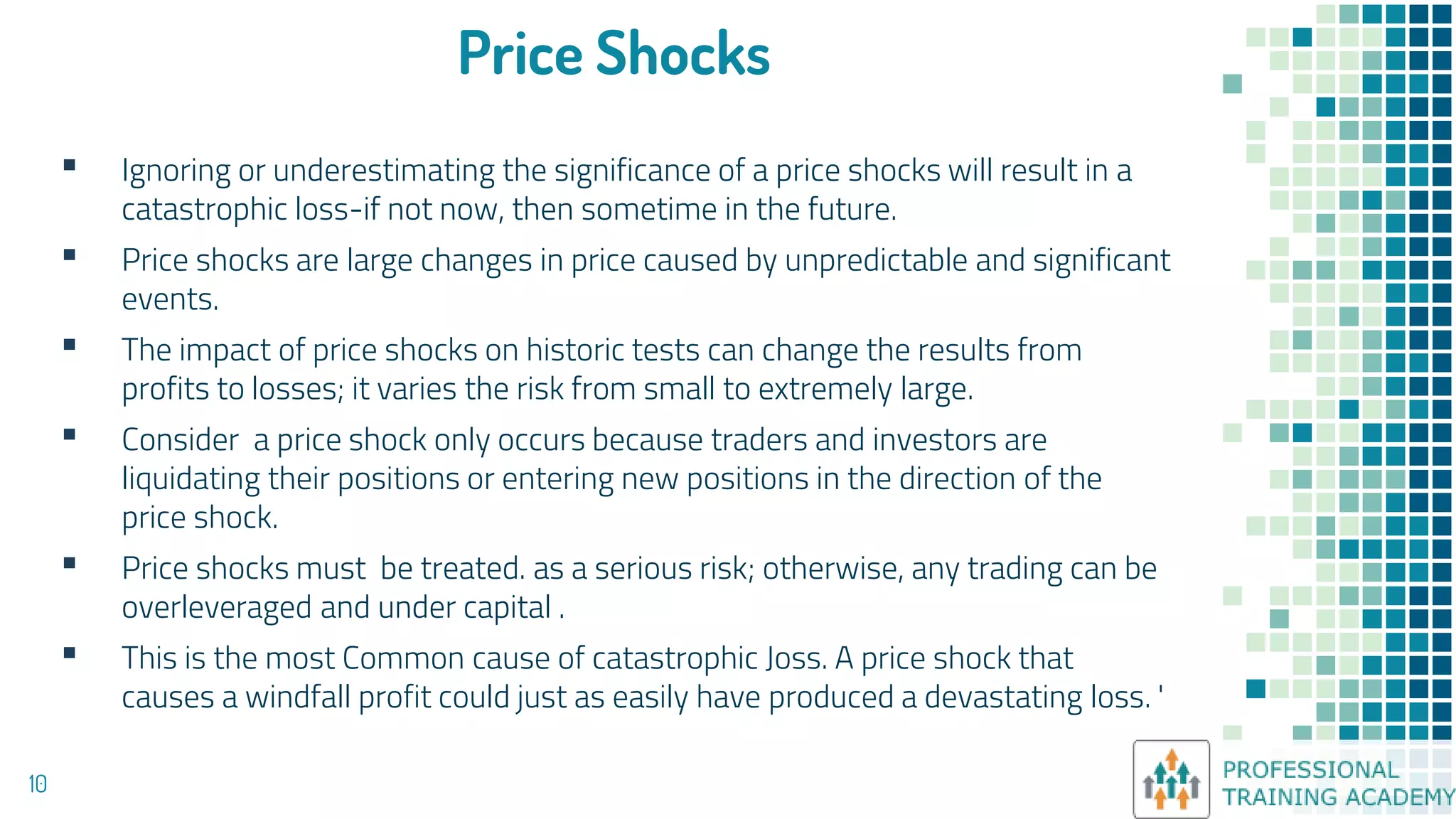

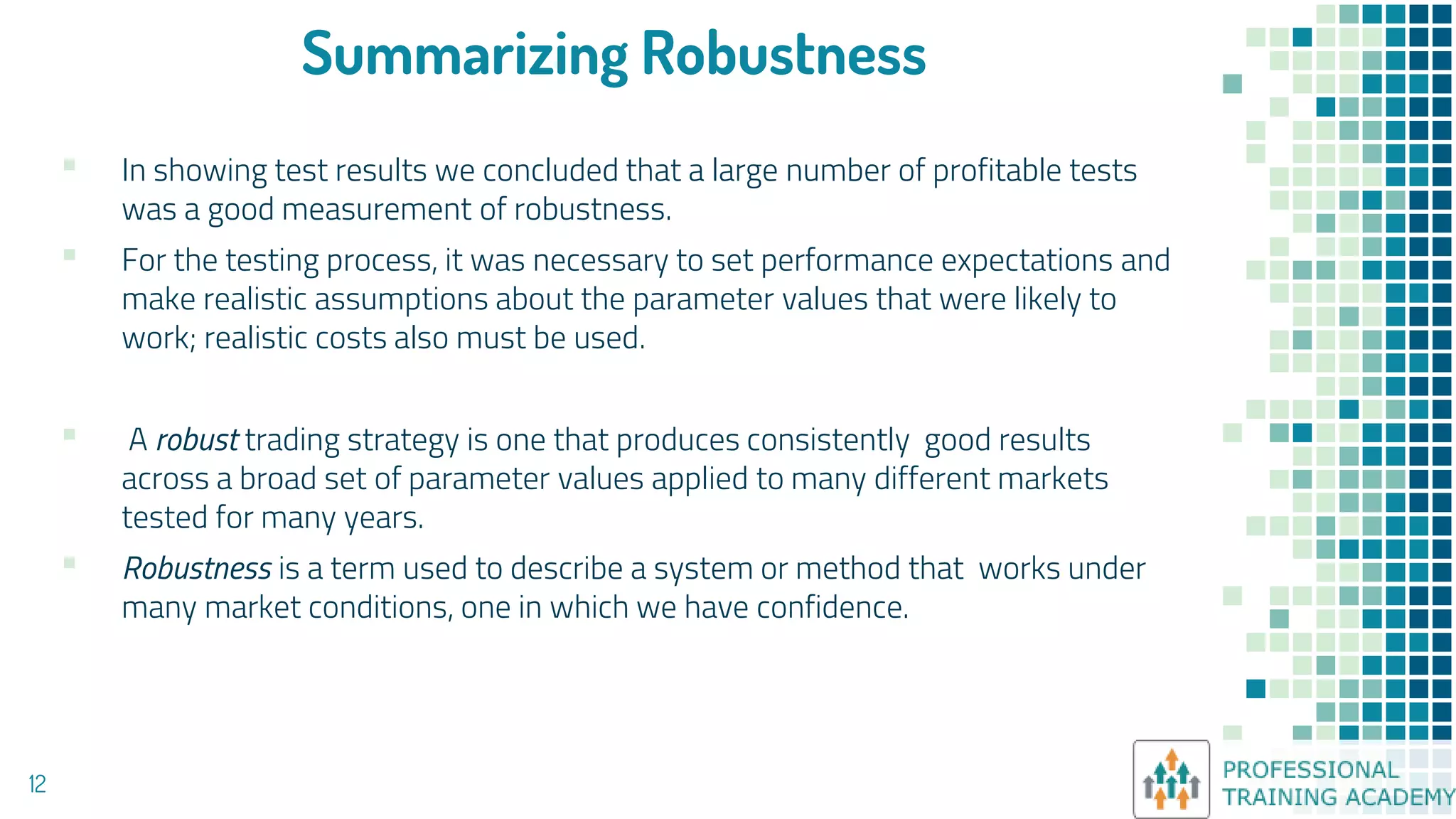

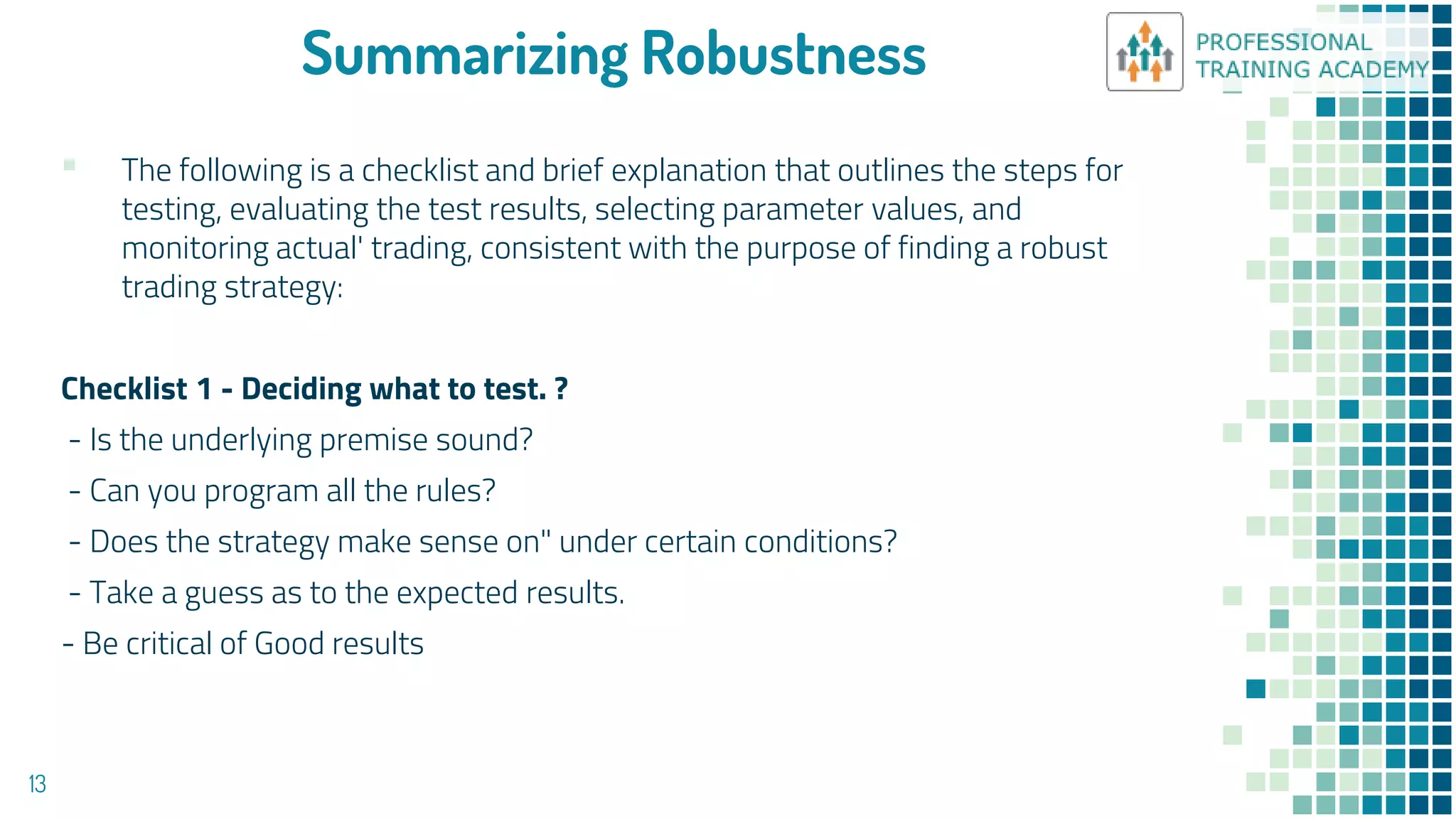

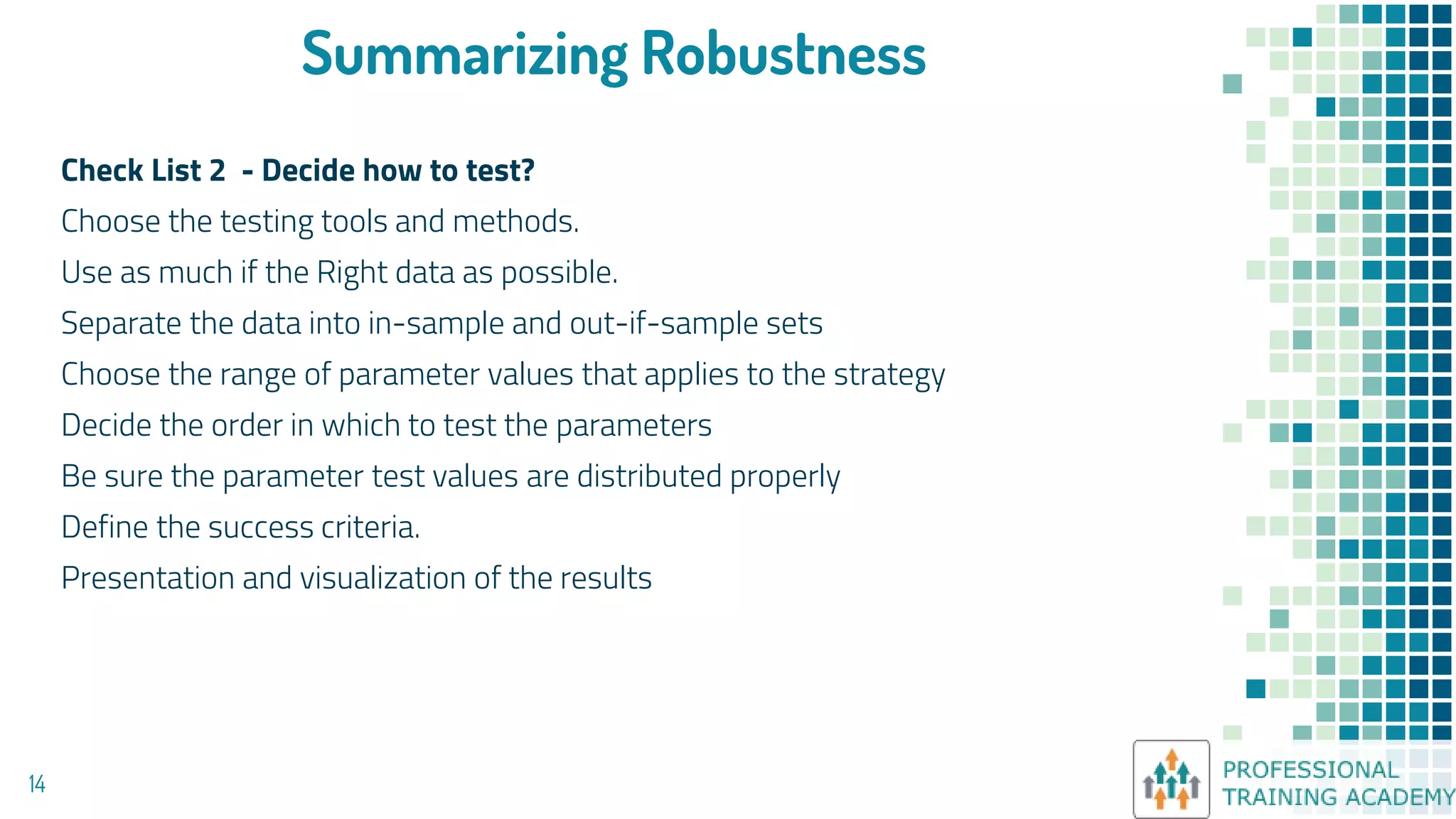

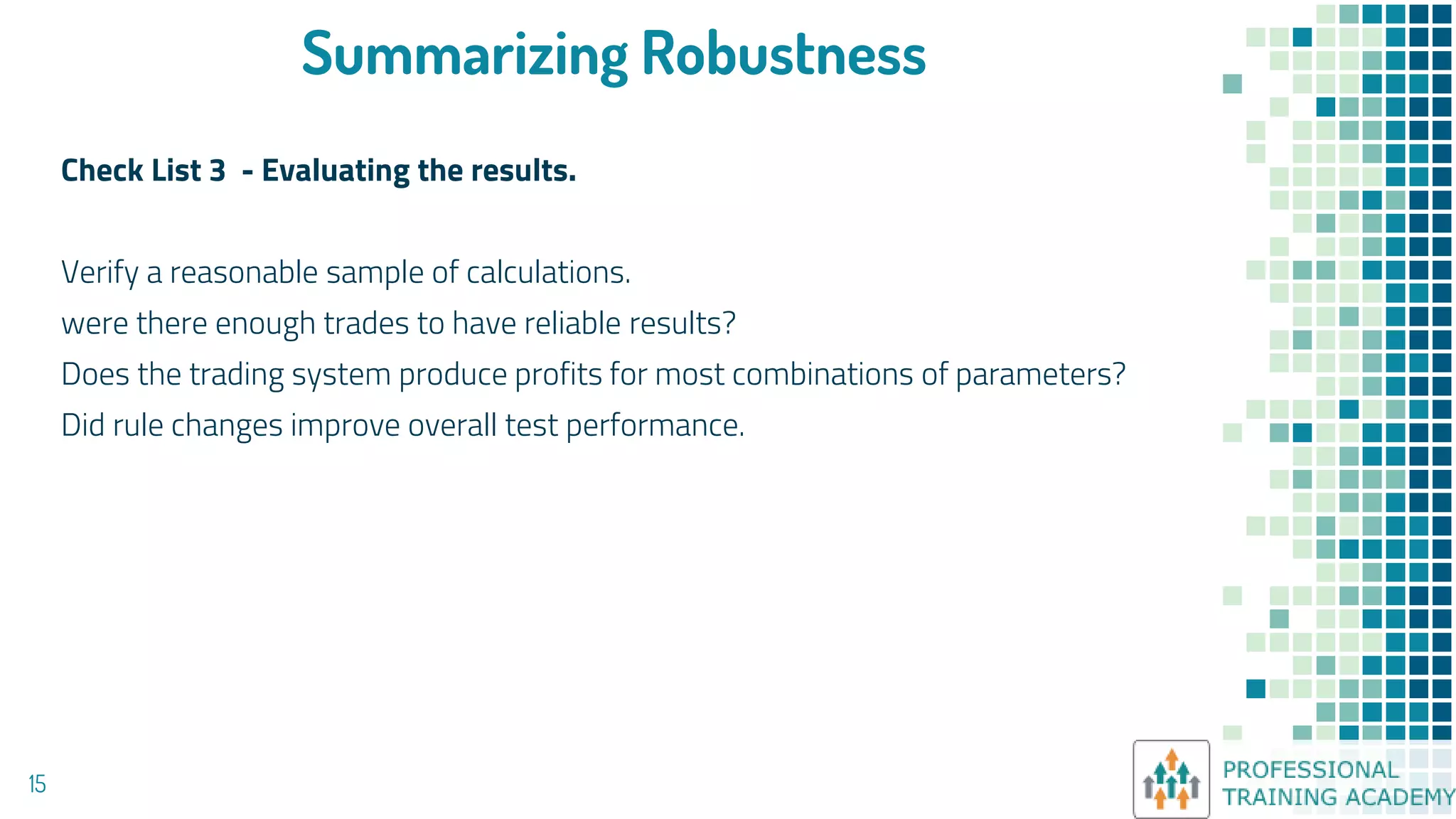

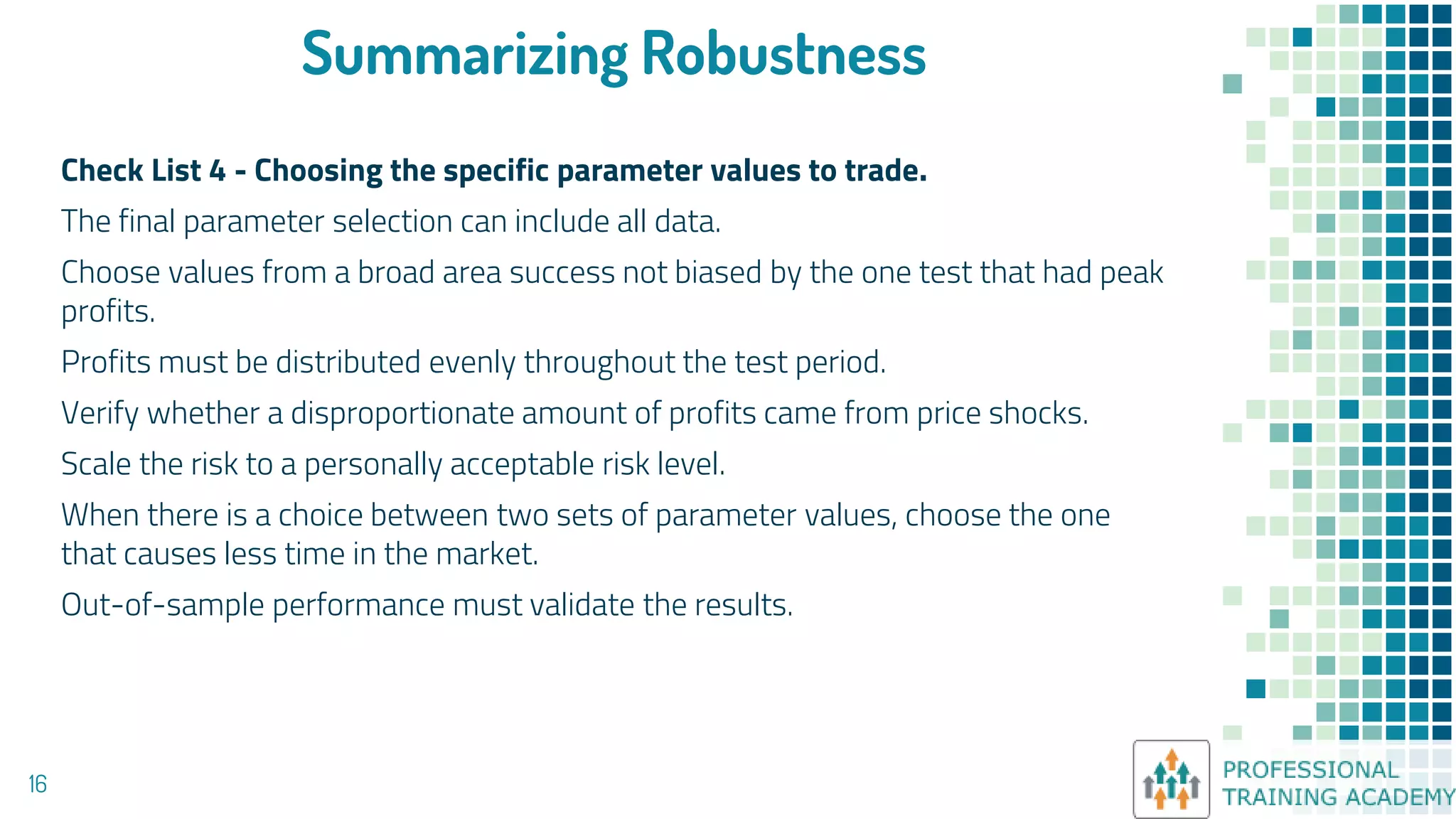

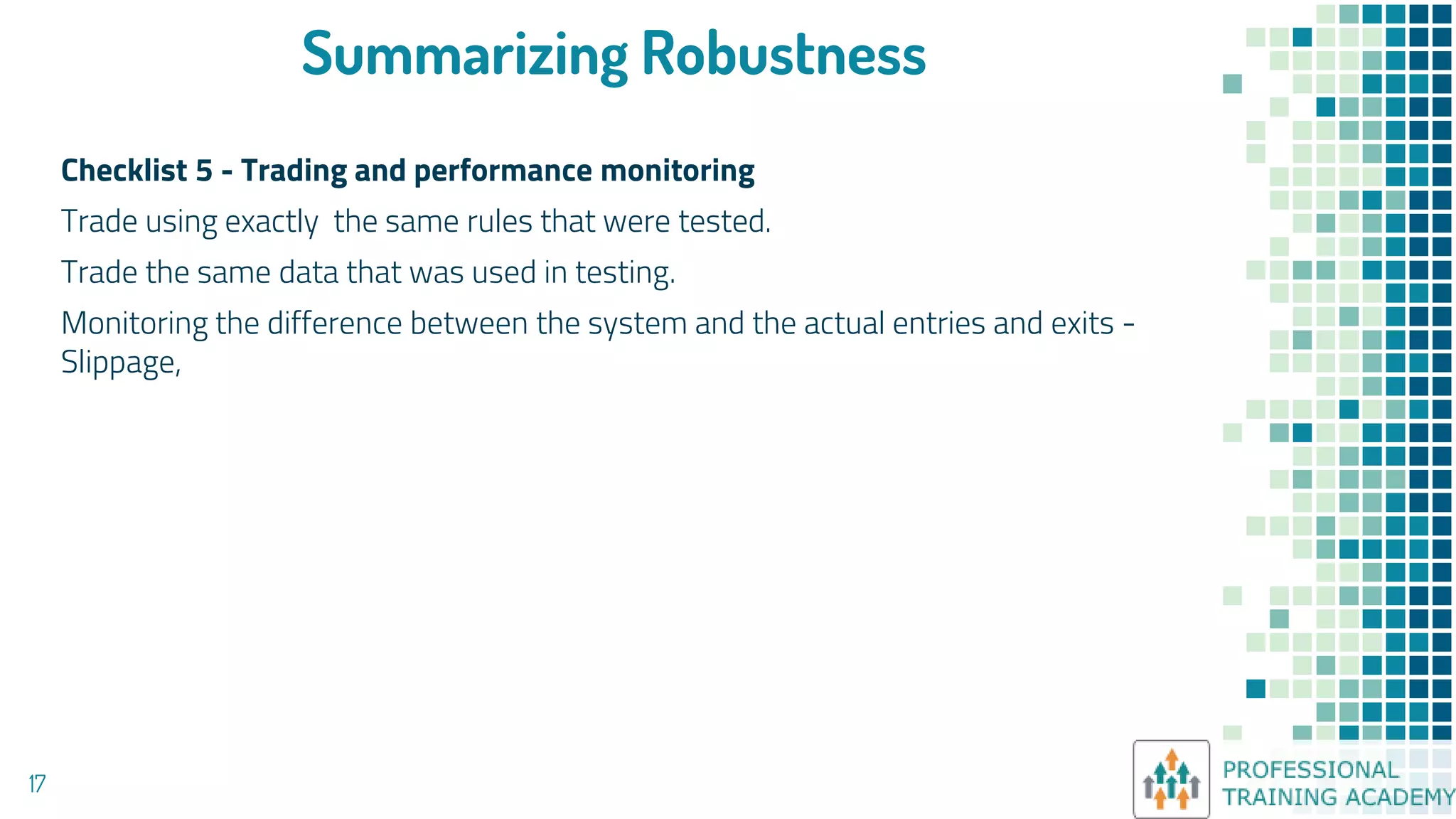

The document outlines a comprehensive approach to system evaluation and testing in risk management, detailing factors such as test parameters, data selection, and the significance of price shocks. It emphasizes the need for robustness in trading strategies, highlighting methodologies for testing, evaluating results, and choosing appropriate parameter values. Additionally, it discusses the importance of monitoring actual trading performance relative to test results for credible outcomes.