Download as PDF, PPTX

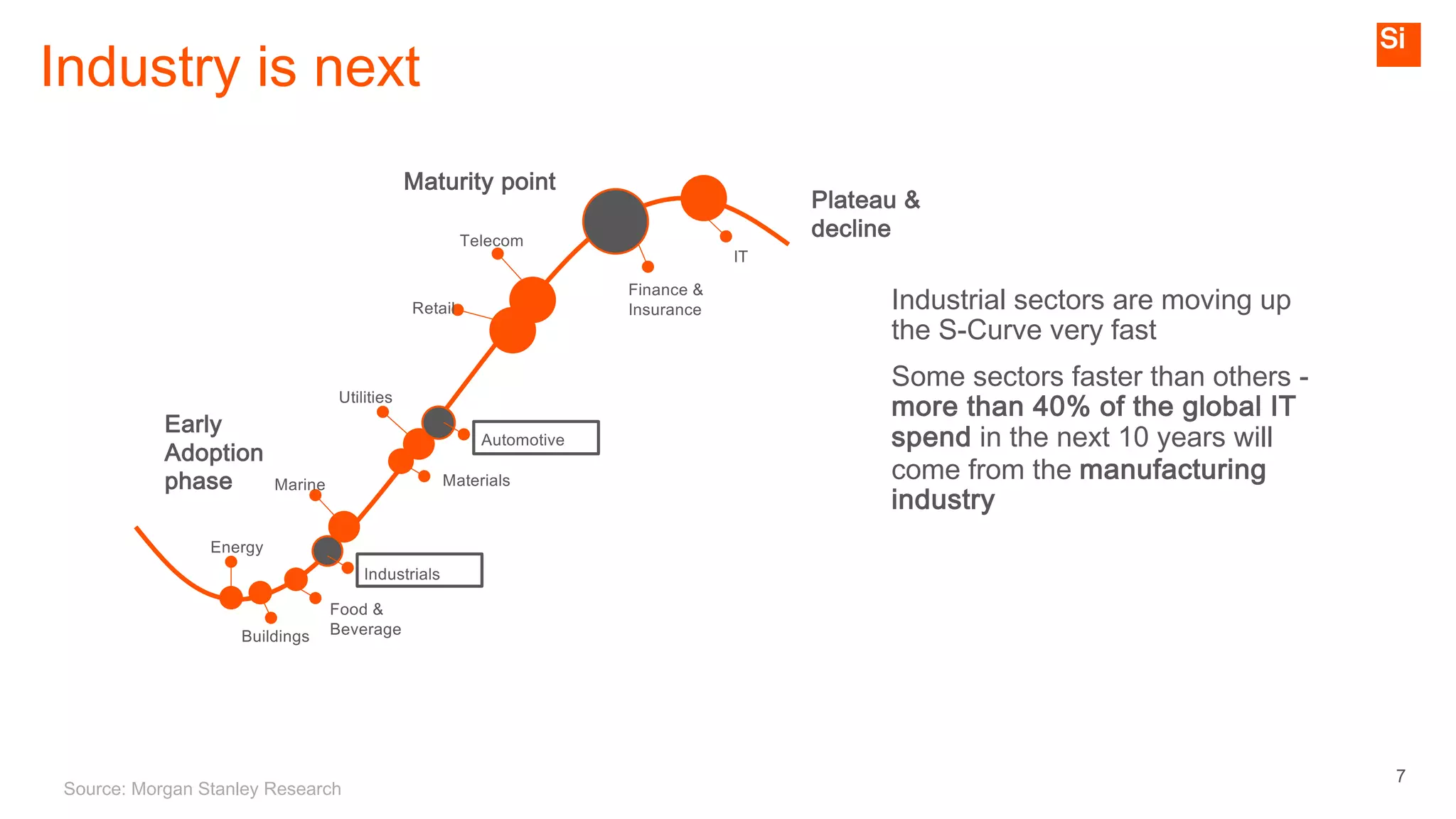

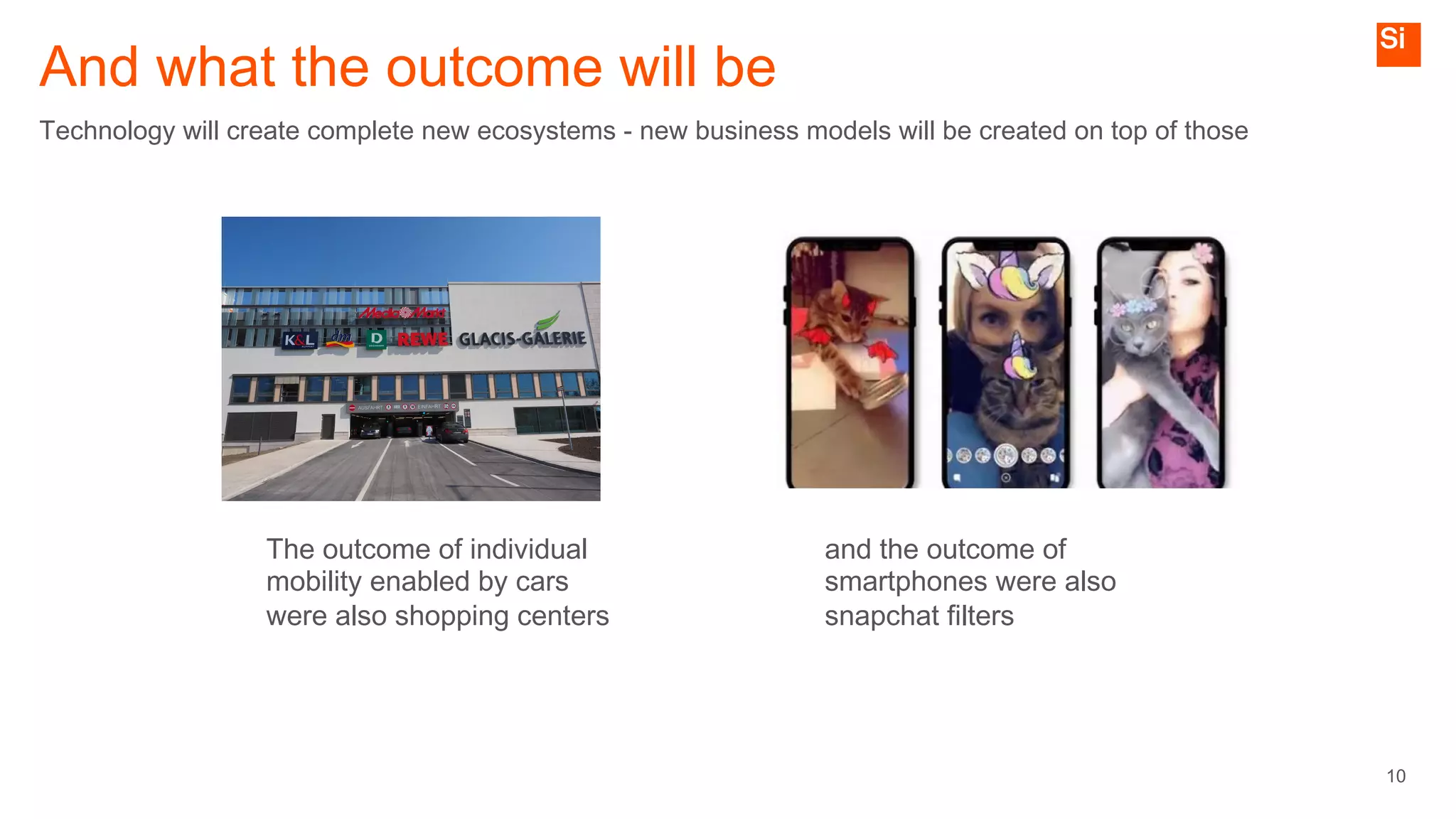

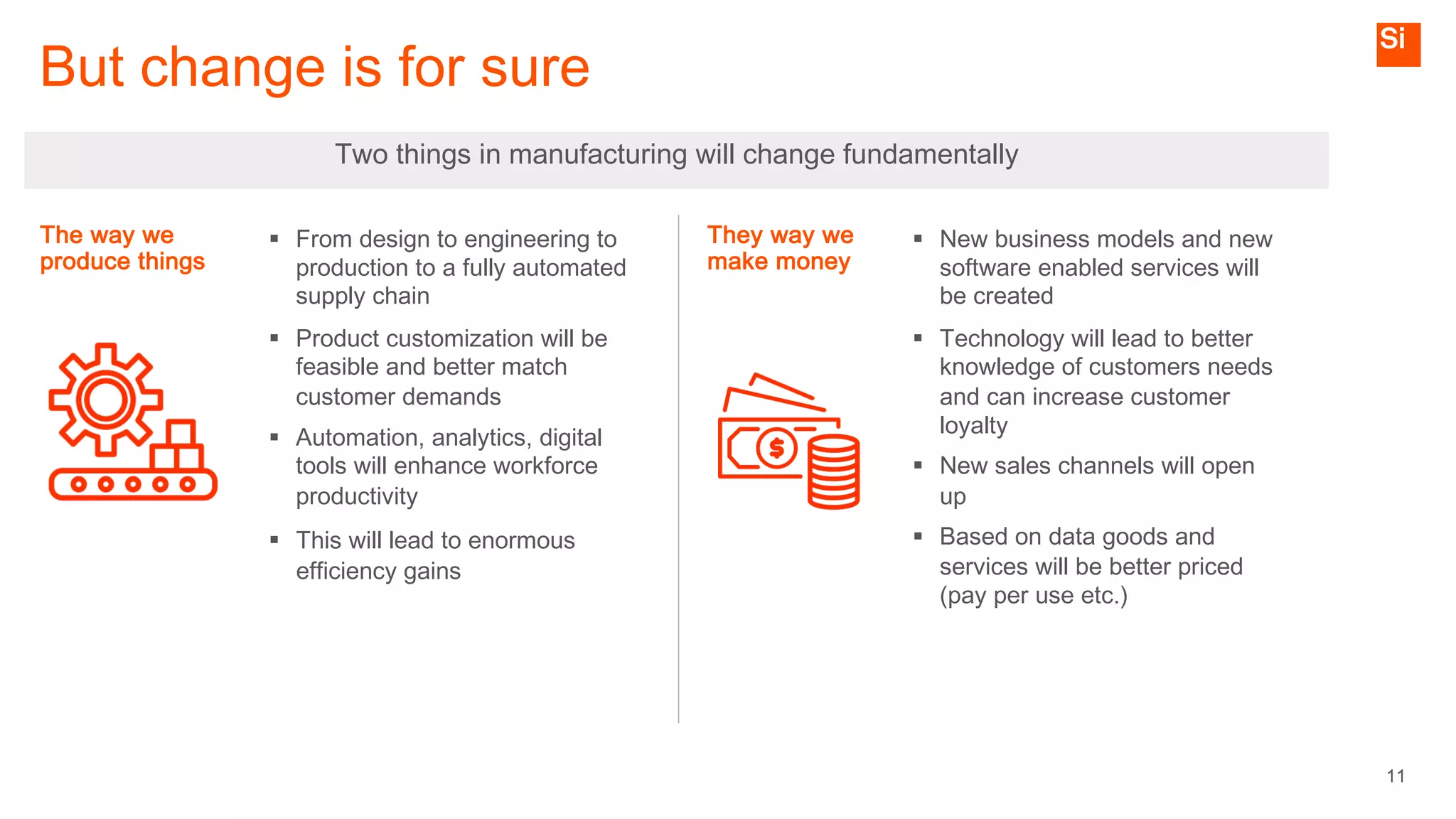

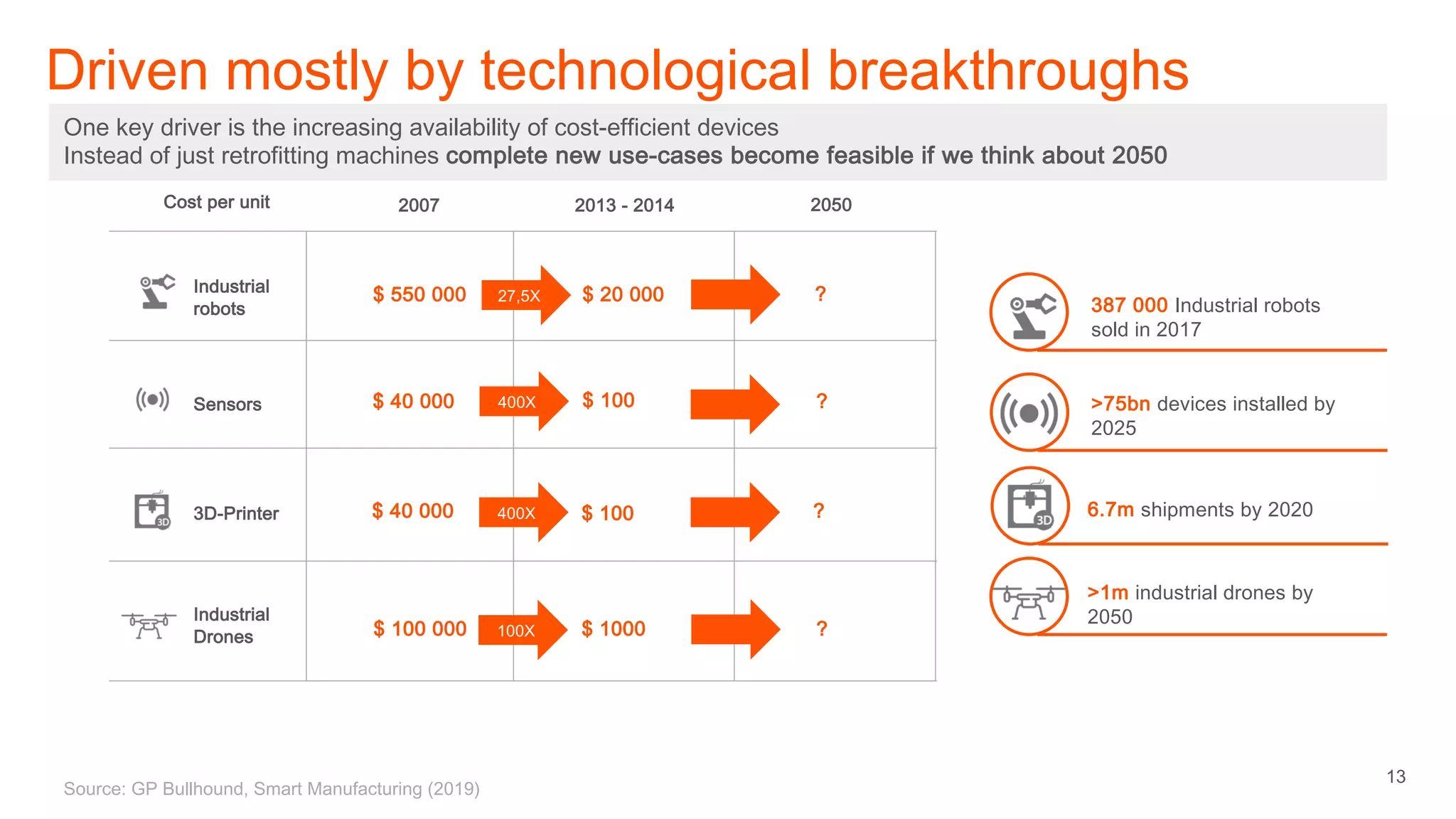

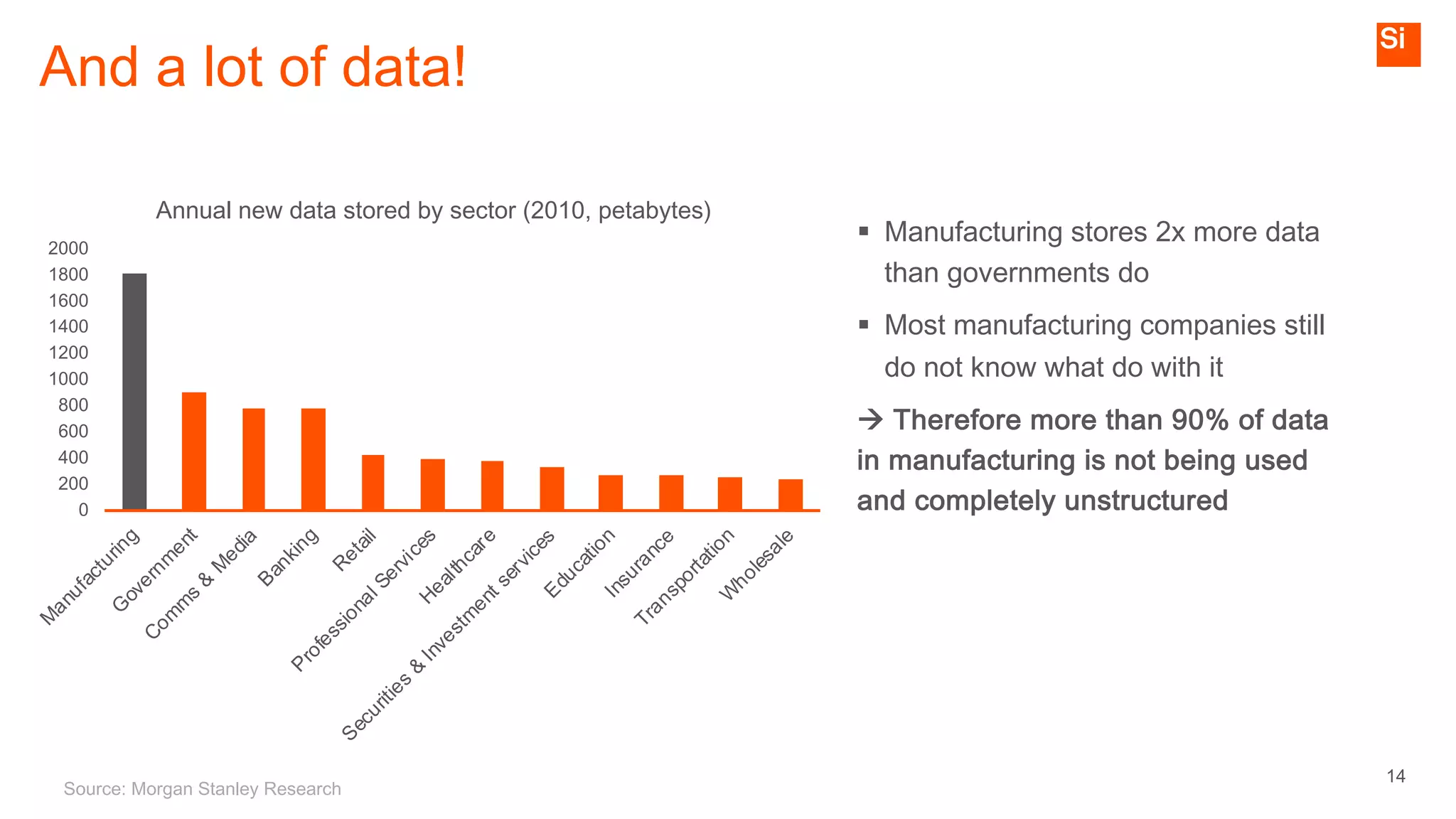

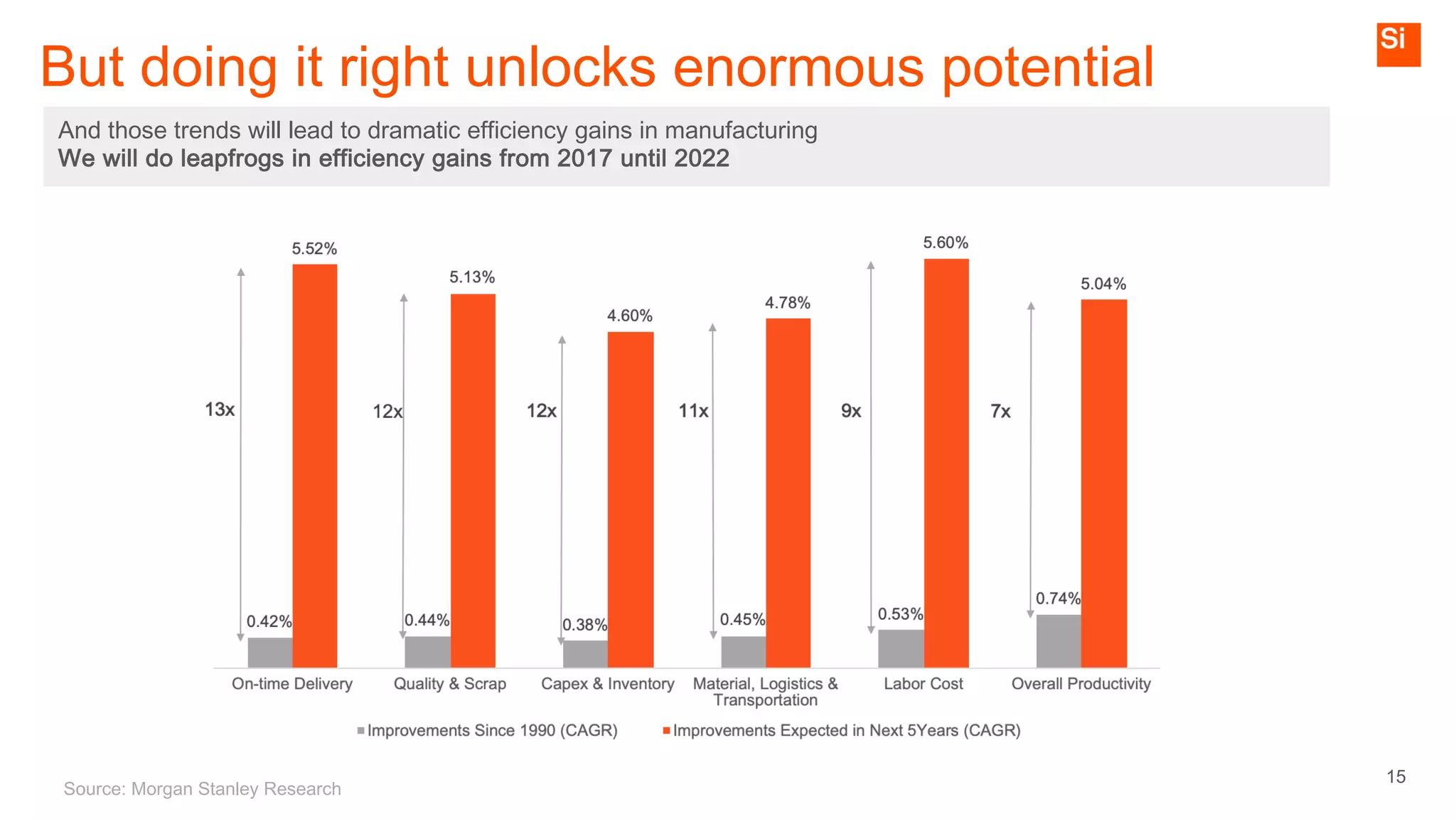

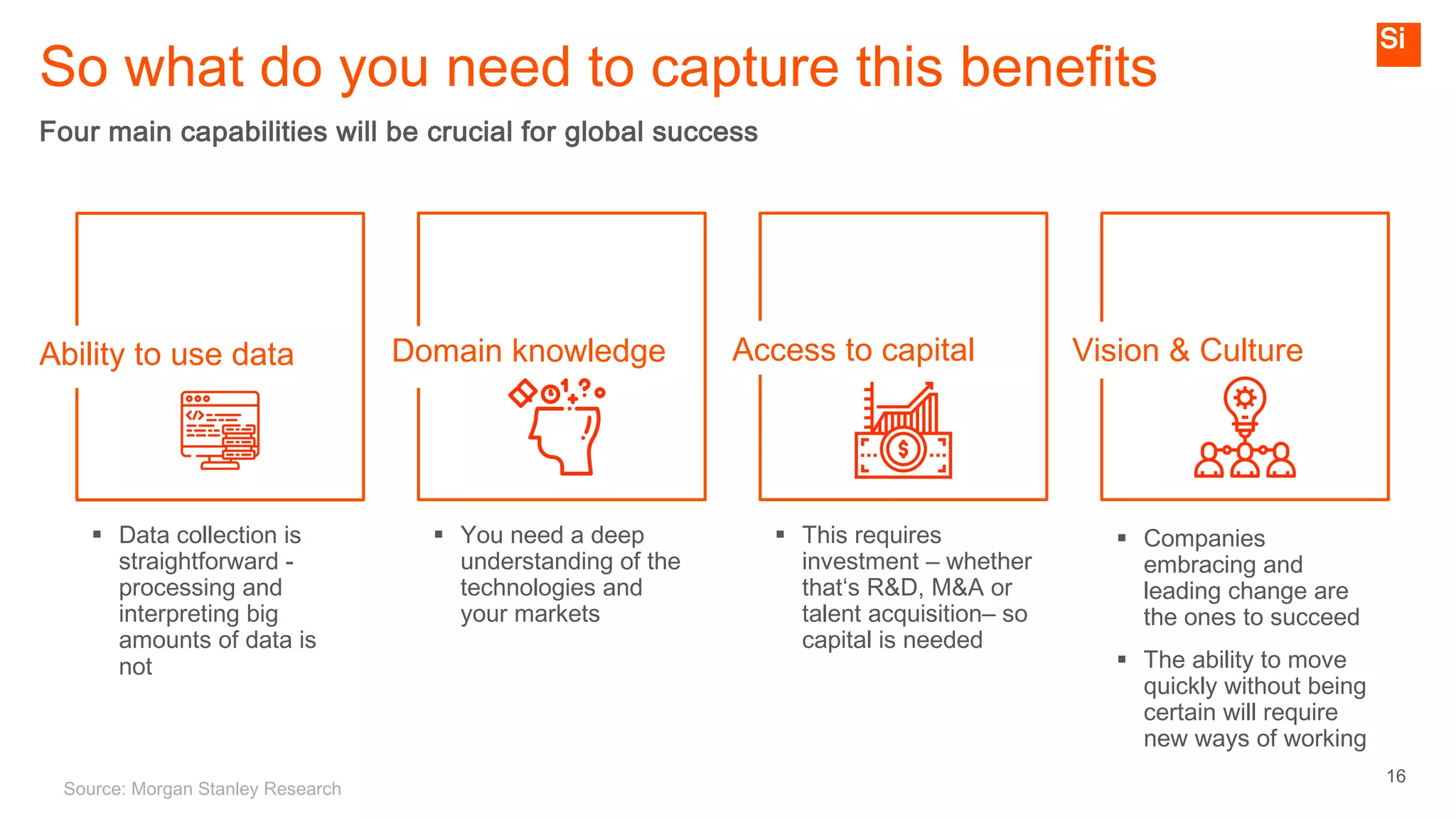

The document discusses the transformation in manufacturing due to technological advancements, emphasizing the shift towards autonomous and self-organizing factories and the integration of data-driven processes. It highlights the importance of rapid innovation and adaptability for companies to succeed and gain economic advantages in a competitive landscape. As manufacturing sectors evolve, new business models and enhanced productivity through automation and data usage will emerge, fundamentally changing the way products are created and services are delivered.

![Computer Networks 01[1 using all terms].pptx](https://cdn.slidesharecdn.com/ss_thumbnails/computernetworks011-251214040533-327dd9f8-thumbnail.jpg?width=640&height=640&fit=bounds)