A wide gamut of people including common people with not an idea of portfolio management are lured in to moneymaking with ease.

They want to enjoy capital appreciation apart from hedge against inflation. Investors have an infinite range of securities to choose from.

Apart from the dilemma of risk and return they also face the difficult question of how much to invest and in which share.

Sharpes optimization model pulls the investors out of this dilemma. The model is easier to understand and also requires less calculation on the part of the investor

![William F. Sharpe was born on June 16, 1934 in Boston,

Massachusetts. A friend introduced William F. Sharpe to Harry

Markowitz, thus he proceeded to work closely with him on the

topic Portfolio Analysis Based on a Simplified Model of the

Relationships Among Securities. Harry guided his dissertation,

after which he received the PhD degree in 1961. He was

invited to take a position at the Stanford University Graduate

School of Business, in 1970. He completed a book, Portfolio

Theory and Capital Markets, and Asset Allocation Tools.

William F. Sharpe has also received awards from diverse

constituencies. He is the proud recipient of the American

Assembly of Collegiate Schools of Business award for the field

of business education in 1980 and the Financial Analysts'

Federation Nicholas Molodovsky Award for outstanding

contributions to the [finance] profession in 1989. He received

the Nobel Prize in Economic Sciences with Harry Markowitz

and Merton Miller in 1990.

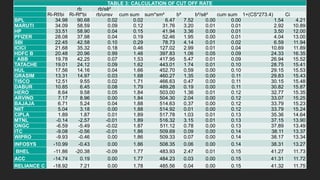

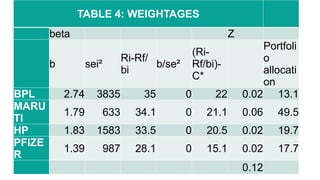

the Single Index Model of portfolio return and risk can

be computed easily.3n+1 calculations, thus only 151

calculations for a portfolio of 50 shares.

.

William Sharpe](https://image.slidesharecdn.com/dr-250627085034-009de3d6/85/REVISITING-SHARPES-SINGLE-INDEX-AND-OPTIMAL-PORTFOLIO-3-320.jpg)