TataKelola dan KamSiber Kecerdasan Buatan v022.pdf

Revenue and BEA additional of ecoconomy.pptx

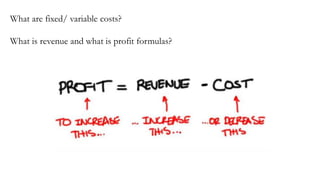

1. What are fixed/ variable costs?

What is revenue and what is profit formulas?

2. Concept of Revenue

• The money income which a producer gets from the sale of his product is

known as revenue of the firm.

• The amount of money that a producer receives in exchange for the sale

proceeds is known as revenue.

• The concept of revenue should not be confused with the concept of profit. Profit

of a firm is estimated as the difference between revenue and cost related to the

production of a commodity (Profit = Revenue –Cost).

Revenue has three aspects:

Total Revenue

Average Revenue

Marginal Revenue

3. Types of Revenue

Total Revenue (TR)

• Total Revenue refers to total receipts from the sale of a given quantity of a

commodity. It is the total income of a firm. Total revenue is obtained by

multiplying the quantity of the commodity.

• Total Revenue = Quantity x Price

Average Revenue (AR)

• Average revenue refers to revenue per unit of output sold. It is obtained by

dividing the total revenue by the number of units sold.

AR and Price are the Same

We knew, AR is equal to per unit sale receipts and price is always per unit. Since sellers receive

revenue according to price, price and AR are one and the same thing. This can be explained as

under: TR = Quantity x Price= So AR=P

4. • Marginal Revenue: is the additional revenue generated from the sale of an

additional unit of output. It is the change in TR from sale of one more unit of a

commodity.

• MR = ΔTR/ΔQ

• MR=TRn – TRn-1

(Here, MR = Marginal revenue, ΔTR= Change in total revenue, ΔQ= Change in

output, TRn= Total revenue from ‘n’ units of the output and TRn-1= Total

revenue from ‘n – 1’ units of the output.)

• Marginal revenue is the addition to total revenue on account of sale of one more

unit of output

• TR is summation of MR: Total Revenue can also be calculated as the sum of

marginal revenues of all the units sold.

• It means, TR = MR + MR+ MR+ ……………….MRn

5. Relationship Between Revenue Concepts

The relationship between different revenue concepts can be discussed under two situations:

• When Price remains Constant (It happens under Perfect competition). In this situation,

firm has to accept the same price as determined by the industry. It means, any quantity of a

commodity can be sold at that particular price.

• When Price Falls with rise in output (It happens under Imperfect Competition). In this

situation, firm follows its own pricing policy. However, it can increase sales only by

reducing the price.

6. Relationship between AR and MR (When Price remains Constant)

• When price remains same at all output levels (like in case of perfect competition), no firm is in

a position to influence the market price of the product. A firm can sell more quantity of

output at the same price.

• It means, the revenue from every additional unit (MR) is equal to AR As a result, both AR and

MR curves coincide in a horizontal straight line parallel to the X-axis as shown.

7. Relationship between TR and Price line

When price remains constant at all the levels of output, then

Price = AR = MR. Therefore, price line is the same as MR

curve. Also, TR = . So, the area under MR curve or price line

will be equal to TR. In Fig., TR at MR level of output = OP x

OQ =Area under price line.

8. Relationship between AR and MR (When Price Falls with rise in output)

When firms can increase their volume of sales only by decreasing the price, then AR falls with

increase in sale. It means, revenue from every additional unit (i.e. MR) will be less than AR. As a

result, both AR and MR curves slope downwards from left to right.

9. General Relationship Between AR and MR

The relationship between AR and MR depends on

whether the price remains same or falls with rise in

output. However, if nothing is mentioned about the

nature of price with rise in output, then the following

general relation exists between AR and MR:

• AR increases as long as MR is higher than AR

(or when MR > AR, AR increases).

• AR is maximum and constant when MR is

equal to AR (or when MR = AR, AR is

maximum).

• AR falls when MR is less than AR (or when

MR < AR>

It must be noted that specific relationship between

AR and MR depends upon the relation of price with

output, Le, whether price remains same or varies

inversely with output.

10. TR and MR (When Price Falls with rise in output)

11. AR and MR Curves under Monopoly and Monopolistic Competition

Both, Monopoly and Monopolistic Competition fall under the category of Imperfect

Competition. Therefore, AR and MR curves slope downwards as more units can be sold only by

reducing the price. However, there is one major difference between AR and MR curves of

monopoly and monopolistic competition.

Under monopolistic competition, the AR and MR curves are more elastic as compared to those

of Monopoly. It happens because of the presence of close substitutes under monopolistic

competition and absence of close substitutes under monopoly. So, when price of a commodity is

increased in both the markets, then proportionate fail in demand under monopoly is less than

proportionate fall in demand under monopolistic competition.

12. Relationship Between TR MR and AR

The TR curve rises as long as MR is positive. It reaches its

highest point (point A) when MR is zero (point B) and it

starts declining when MR becomes negative. The

relationship can be summed up as under:

• As long as MR is positive, TR increases (or when TR

rises, MR is positive).

• When MR is zero, TR is at its maximum point (or when

TR is maximum, MR is zero).

• When MR becomes negative, TR starts falling (or when

TR falls, MR is negative).

13.

14.

15. Reach a point in a business venture when the

profits are equal to the costs.

16. To gain an understanding of calculating break-even we will use the

example of a young entrepreneur wishing to start up a business

delivering packages of fruit and veg.

He knows that the last local shop in his area closed last year.

Sensibly, he has carried out market research which indicates that

there will be a good level of demand, but before he begins he needs

to know how profitable the business might be. He has also fully

researched the costs of starting up as a deliveryman and the costs of

purchasing supplies.

17. The costs he has researched are as follows:

• cost of delivery van purchase £6000;

• insurance and road tax £100 per month;

• petrol £10.00 per day;

• average cost of fruit and veg box £5.00;

• Salaries - £1150 per month;

• loan repayment £500 per month for twelve months.

18. His market research indicates that the fruit and veg boxes will

have an average sales price of £9.00.

The question then is how many boxes will he need to sell to

cover all his costs, i.e. to break even?

He decides to calculate break-even on a monthly basis.

19. Fixed costs

Loan - £500 per month

Petrol costs - £250 per month

Insurance/road tax - £100 per month

Salaries - £1150 per month

Total fixed costs - £2000 per month

Variable costs

£5.00 per box

Sales revenue

£9.00 per box

20. Calculating break-even point using the contribution method.

Once we have calculated costs, the next step in calculating

break-even output or sales is finding out how much

contribution each item sold produces for the business.

21. Every product made has a variable cost and a selling price

(which must obviously be higher).

The difference between the selling price per unit and the

variable cost per unit is known as the CONTRIBUTION towards

covering the business’s fixed costs.

22. There is a simple formula for calculating break-even output.

Break-even output = Fixed costs

Contribution per unit.

Contribution per unit = Selling price – Variable costs (per

unit)

23. Break-even output = Fixed costs

Contribution per unit.

Contribution per unit = Selling price – Variable costs (per unit)

Break even in units = £2,000

£9 - £5

Break even in units = £2,000 / 4

Break even in units = 500 boxes

24. We can now see that to break even our deliveryman must

sell 500 fruit and veg boxes per month.

• If he sells more than 500 boxes he will make a profit.

• If he sells less than 500 boxes he will make a loss.

At break-even point the

total contribution equals

the total fixed costs.

25. Break-even analysis also allows us to calculate the profit or

loss a business will make at different levels of output.

This will always be important – after all our grocery seller may

wish to go into business only if his profits are likely to be at a

certain level.

First of all calculate the

break-even output, in the

above case we know it is

500 boxes per month.

26. As a result of his market research he believes that he can sell 650

boxes a month.

He now wants to know what his profit will be at that level of

sales. To find out how much profit will be made, we again use the

idea of contribution.

27. In this case predicted sales are 650. Break-even sales are 500.

Profit per sales = Predicted sales – Break even sales x

Contribution per unit

Profit per sales = 650 – 500 x £4

Profit per sales = 150 x £4

Profit per sales = £600

His profits per month on sales of 650 boxes will be £600.